Summary

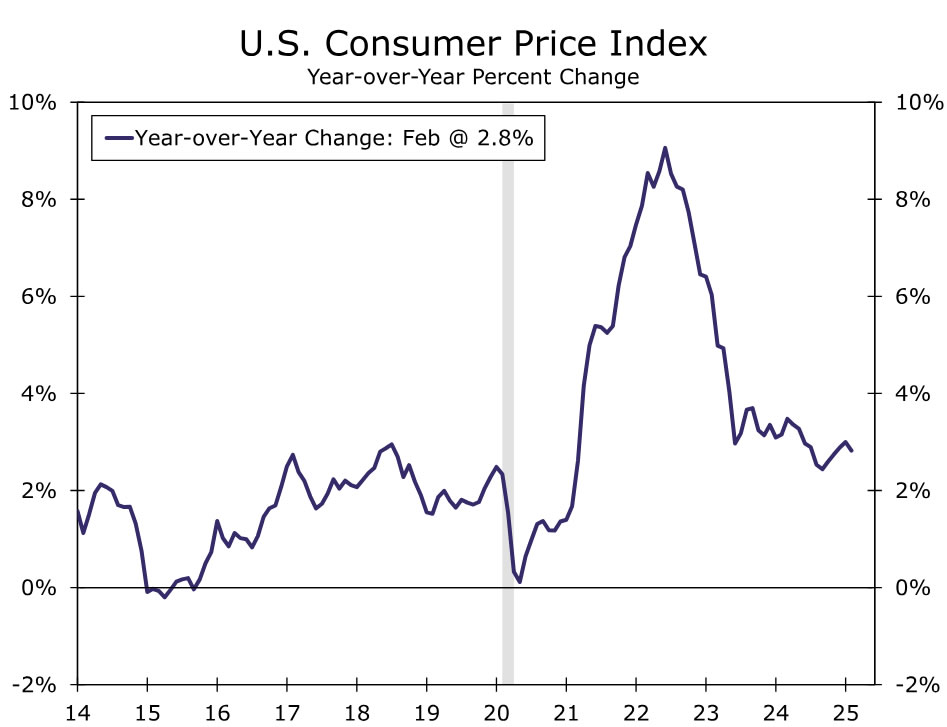

The Consumer Price Index came in slightly softer than expected, with both the headline and core indices advancing 0.2% in February. Slower growth in food and energy costs, as well as an easing in core goods and services inflation, helped overall price growth cool. The outturn is a welcome development after January’s unexpectedly strong print.

Stepping back from the month-to-month noise, inflation has essentially moved sideways since early 2024. New and potential tariffs are poised to stoke goods inflation in the coming months, which is unlikely to be offset by further slowing in shelter and other services inflation.

With today’s data in hand, we expect the core PCE deflator to increase around 0.35% in February, which would keep the Fed’s preferred inflation measure running closer to 3% than its 2% goal. This presents a challenging situation for the FOMC, but we expect the Committee to respond with a gradual pace of monetary policy easing later this year amid slower growth and a somewhat softer labor market.

Good, but not Eggcellent

After a hot half-a-percentage-point increase in January, the Consumer Price Index rose 0.2% in February, a touch softer than consensus expectations. The more temperate gain pushed down the annual rate of inflation two tenths to 2.8%. Despite the slight reprieve, the CPI has essentially moved sideways since early 2024 (chart).

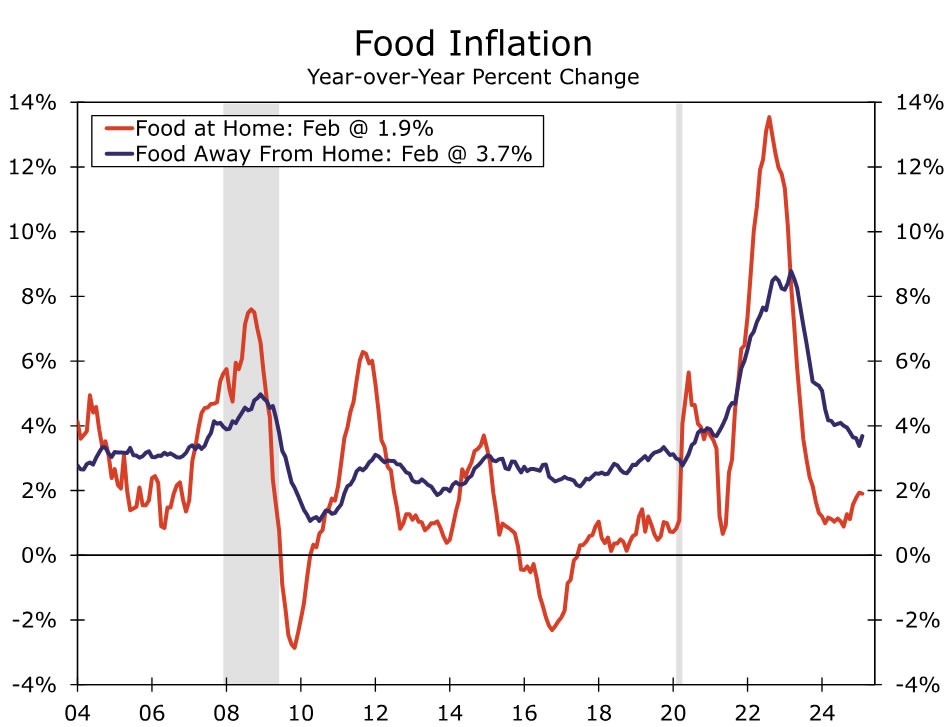

A slowing in energy and food inflation helped the headline CPI’s monthly moderation. Overall energy prices rose 0.2%, as a 1.4% increase in energy services was largely offset by a 1.0% drop in gasoline prices. Grocery store prices were flat over the month despite the 10.4% monthly rise in egg prices, as prices for fruits & vegetables, dairy products and “other” food products fell. Relief at the grocery store, however, was partially offset by prices for food away from home picking up with a 0.4% gain.

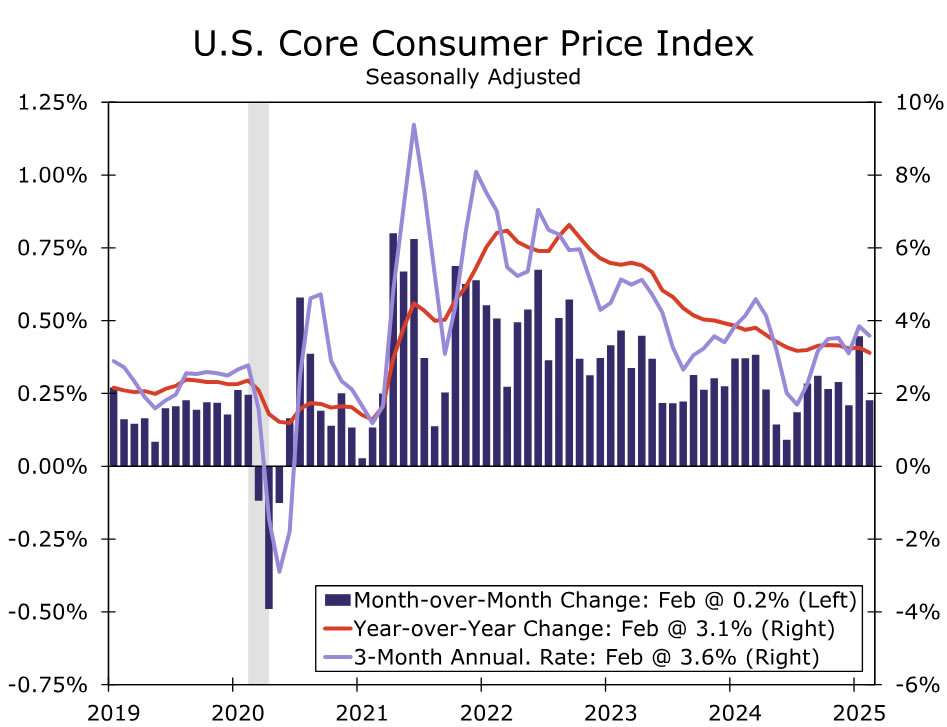

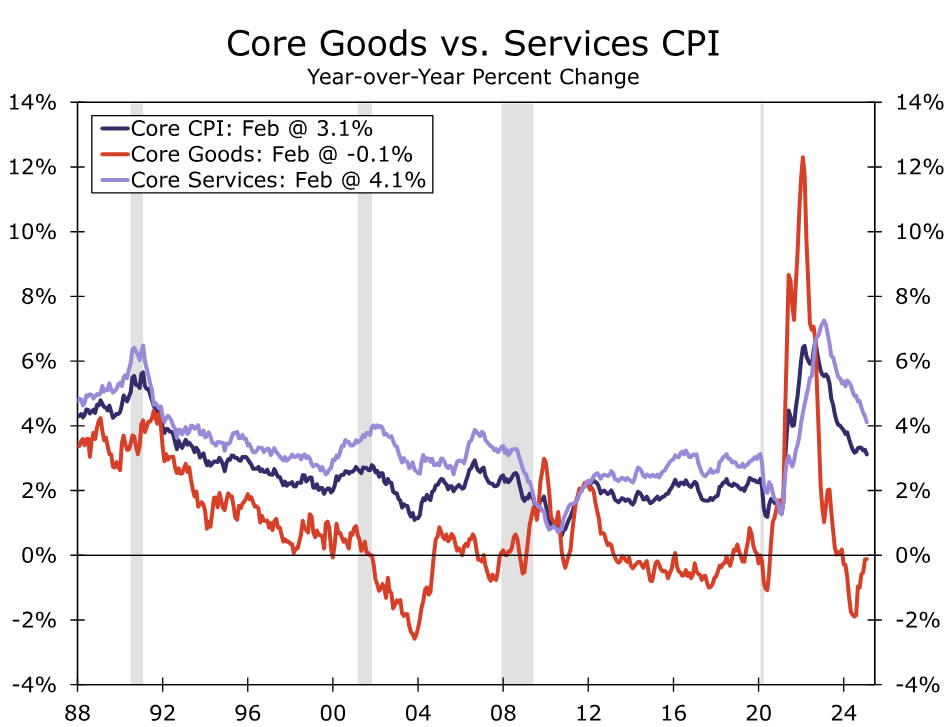

Excluding food and energy, the core CPI also came in a bit softer than expected. The 0.2% monthly increase (0.23% on an unrounded basis) was about half of January’s 0.45% increase. Both goods and services contributed to the moderation. Core goods inflation slowed to 0.2% month-over-month after a 0.3% increase in January. Overall vehicle inflation (+0.3%) ebbed from the prior month, with new vehicle prices slipping (-0.1%) and used car and truck prices (+0.9%) easing back below its average increase of 1.1% over the past six months. Elsewhere, recreational goods prices fell 0.7% and prescription drug prices were flat after a jump in January.

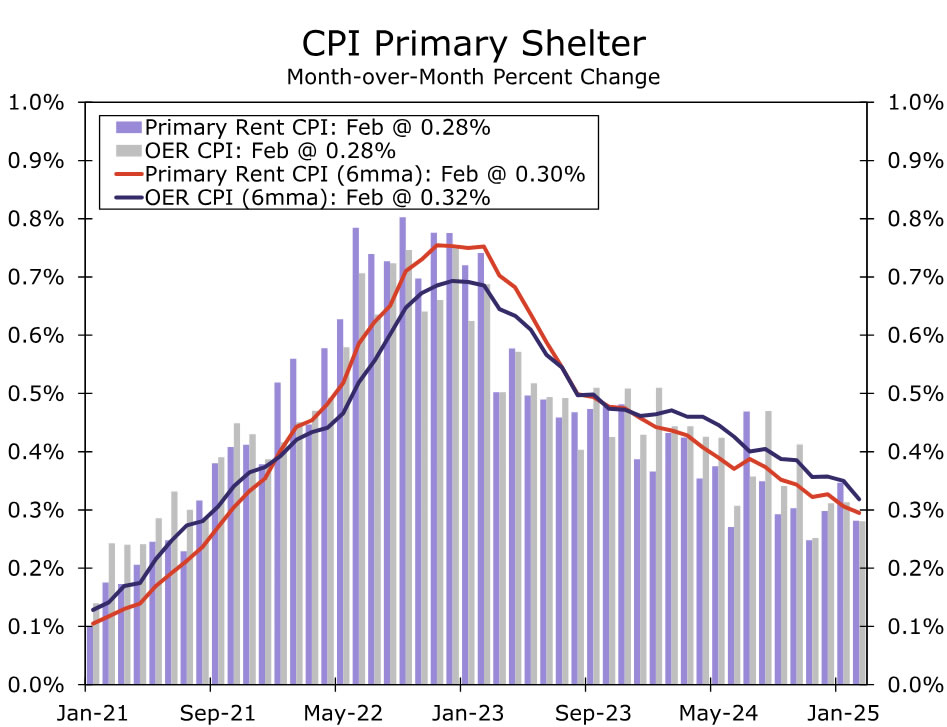

On the services side, the slowdown in primary shelter continued, with both rent of primary residences and owners’ equivalent advancing 0.28% last month (chart). Transportation services decreased 0.8% amid a price declines for airline fares and vehicle rentals, as well as a smaller rise in motor vehicle insurance (0.3%) after a 2% jump in January.

Taking a step back, progress has continued on the inflation front through the month-to-month noise. The ongoing downtrend in services remains enough to offset the firmer trend in goods inflation. The core CPI slowed to a three-and-a-half year low of 3.1% in February, indicating inflation continues to gradually recede. But with upward pressure on goods prices intensifying with tariffs, a further reduction in inflation this year is likely to be hard to come by.

The FOMC likely will welcome a CPI report that came in a bit softer than expected and shows disinflation proceeding. Yet, the year-ago pace of core CPI inflation is still ~75 bps above its February 2020 level, and the three-month annualized change in the core CPI is still an uncomfortably high 3.6%. Moreover, the details of the report suggest that the core PCE deflator may come in slightly higher than what we were anticipating heading into today’s report. Based on the February CPI data, the core PCE looks set to pickup with a 0.35% monthly gain, but we will know more after tomorrow’s PPI data. Higher tariffs threaten to raise spot inflation and inflation expectations in the months ahead, but they also threaten a labor market that has shown some small signs of weakness. This presents a challenging situation for the FOMC, and we expect the Committee to respond with a gradual pace of monetary policy easing later this year.