mikkelwilliam

We previously covered Upstart Holdings (NASDAQ:UPST) in August 2023, discussing the stock’s massive volatility attributed to the FQ2’23 miss and the eye-watering short interest.

While the management had continued to show tight control over operating costs while improving its loan automation process, its Net Interest Income [NII] and Net Interest Margins [NIM] remained underwhelmingly negative at a time of elevated interest rate environment.

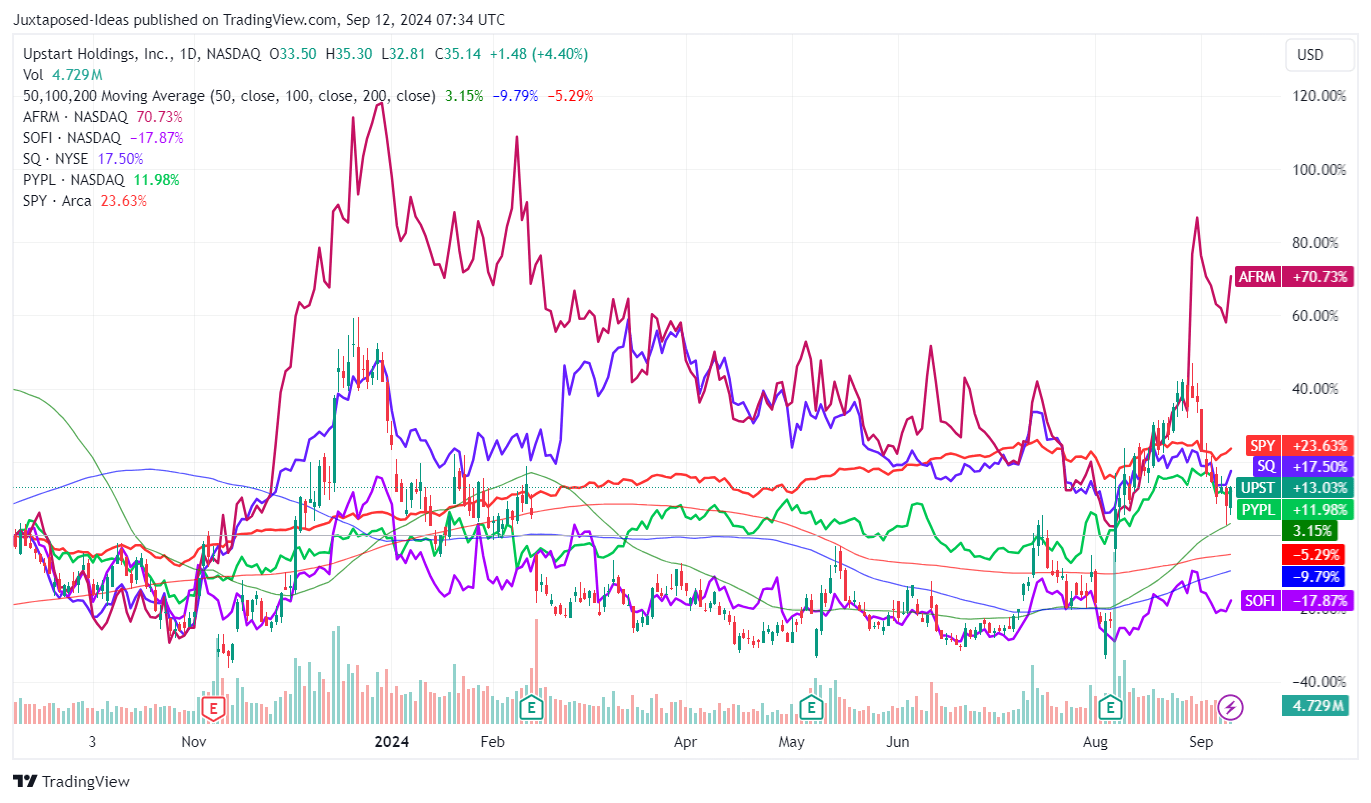

UPST 1Y Stock Price

Trading View

Since that Hold rating, UPST has recovered by +16.8% compared to the wider market at +25.4%, partly attributed to the market’s growing optimism surrounding the Fed’s upcoming rate cut in the September 2024 FOMC meeting.

The same recovery has also been observed in other fintech/ lending peers to various degrees, thanks to the intermediate-term lowered borrowing costs and the accretive impact on their bottom-lines.

Even so, we are uncertain if UPST’s rally is well deserved, since it has not been able to achieve positive profit margins despite the supposed rich spreads from the elevated interest rate environment.

While the fintech operates as a cloud-based AI lending platform with the aim of improving access to credit for all, it appears the remaking of the lending process to more accurately quantify the true risk of its loan continues to deliver mixed results.

This is because UPST delivered a relatively rich FQ2’24 NII of $41.41M (+2.3% QoQ/ +39.7% YoY), which unfortunately have been drastically moderated by the increasingly elevated Fair value and other adjustments of -$44.31M (+12.6% QoQ/ -18% YoY).

With its unrealized loss on loans, loan charge-offs, and other fair value adjustments consistently growing to -$31.94M (-7.9% QoQ/ -32.2% YoY), it appears that the credit quality of its loan portfolio has been less than optimal, since “the fair value of the loans on our balance sheet has declined and may continue to decline.”

At the same time, UPST continues to report a relatively high Annual Percentage Rate of 38%, compared to the US average credit card interest rate of 21.48% for consumers with “really good credit” as of September 10, 2024, as best explained by the CEO during the recent earnings call:

All else being equal, a higher APR will select for a riskier borrower, a notion known as adverse selection. Conversely, a lower APR will select for a less risky borrower. (Seeking Alpha)

Combined with the elevated operating expenses of $183.11M (-6.2% QoQ/ +8.2% YoY), it is unsurprising that the fintech has been unable to report GAAP break even bottom-lines despite the relatively rich NII generation.

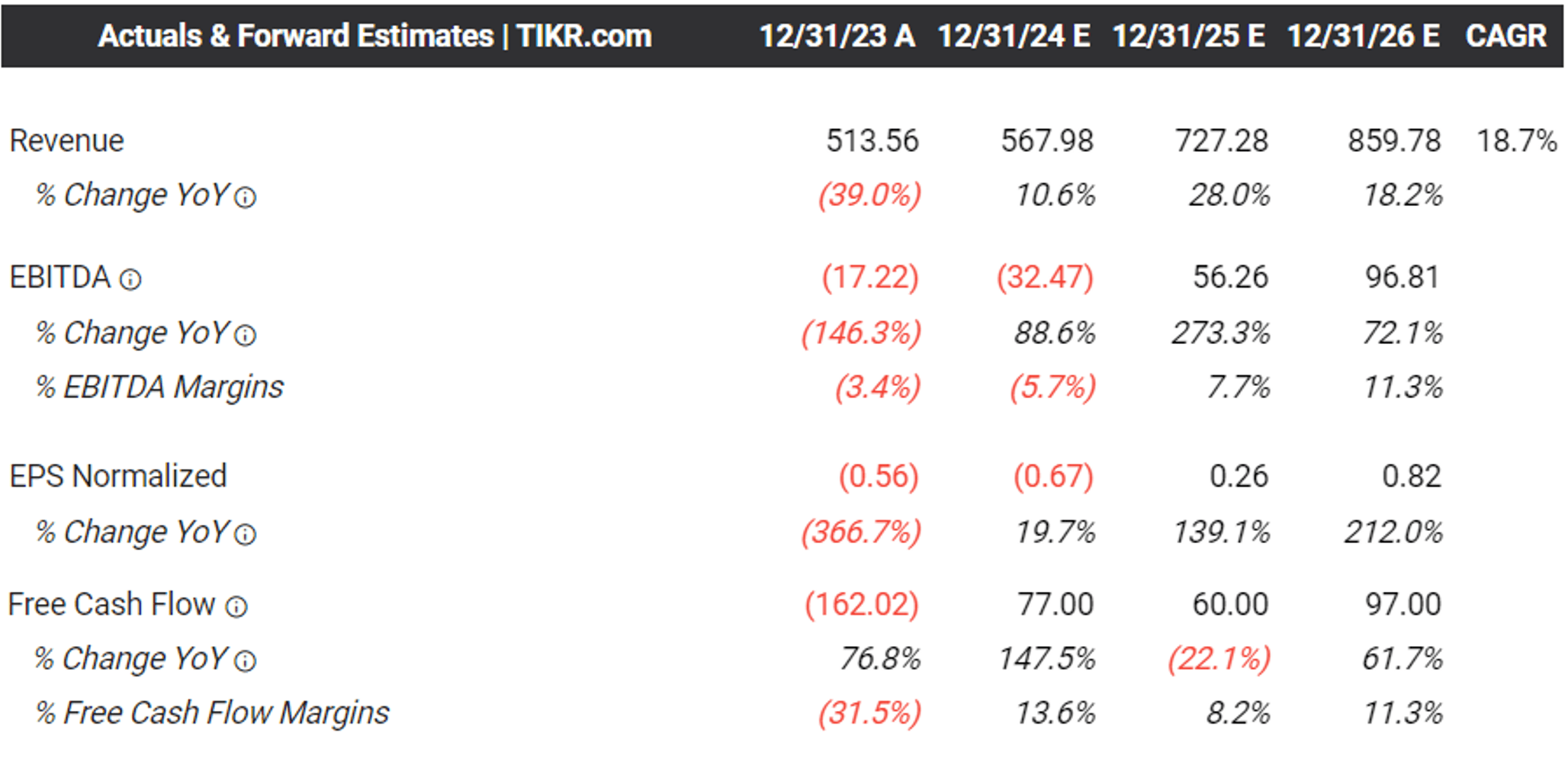

The Consensus Forward Estimates

Tikr Terminal

On the one hand, UPST has already offered a rather promising FQ3’24 guidance with revenues of $150M (+17.5% QoQ/ +11.1% YoY), contribution margin of 57% (-1 points QoQ/ -7 YoY), and adj EBITDA of -$5M (+46.2% QoQ/ -317.3% YoY).

Perhaps this is why the consensus has moderately raised their forward estimates, with the fintech expected to generate an improved top/ bottom-line growth through FY2026.

The top-line numbers do not appear to be overly aggressive, since an increasing amount of UPST’s loans have been fully automated at 91% in the latest quarter, up from 73% two years ago, with it undeniable that the fintech is likely to enjoy a more than decent top-line growth in the intermediate term.

This is especially since the fintech continues to expand the availability of its Home Equity Line of Credit [HELOC] to 30 states (+11 QoQ), with the “magic mortgage rate” of 5% potentially triggering a housing market boom and with it, a new growth opportunity.

These developments are significantly aided by UPST’s growing funding partnerships and the significant reduction in the use of its balance sheet, with H2’24 to bring forth improved funding mix.

On the other hand, while the market may already be pricing in UPST’s higher loan originations upon the normalization in borrowing costs, up from the $1.1B reported in the latest quarter (inline QoQ/ -8.3% YoY), we are not certain if volume growth alone is sufficient to boost its bottom-line performance.

This is barring any drastic improvements in its portfolio quality and operating efficiency, in our opinion, given that the fintech “tripled the number of Upstarters (employees) on our servicing product and engineering teams” – one that has been a bottom-line drag thus far.

As a result, investors whom continue to be bullish about UPST’s prospects may want to temper their near-term expectations indeed.

So, Is UPST Stock A Buy, Sell, or Hold?

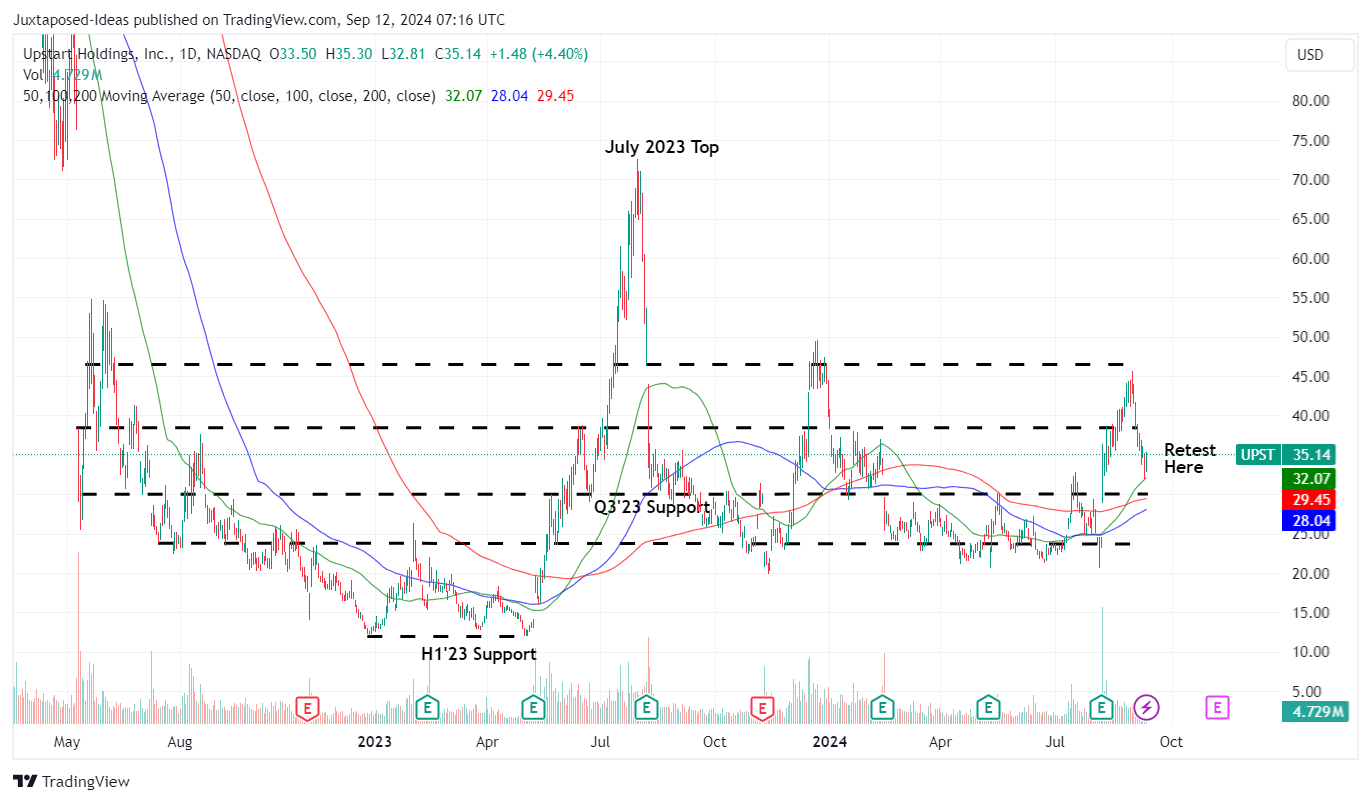

UPST 2Y Stock Price

Trading View

For now, UPST has already returned most of its recent gains, while appearing to be well-supported at the recent support levels of $33s.

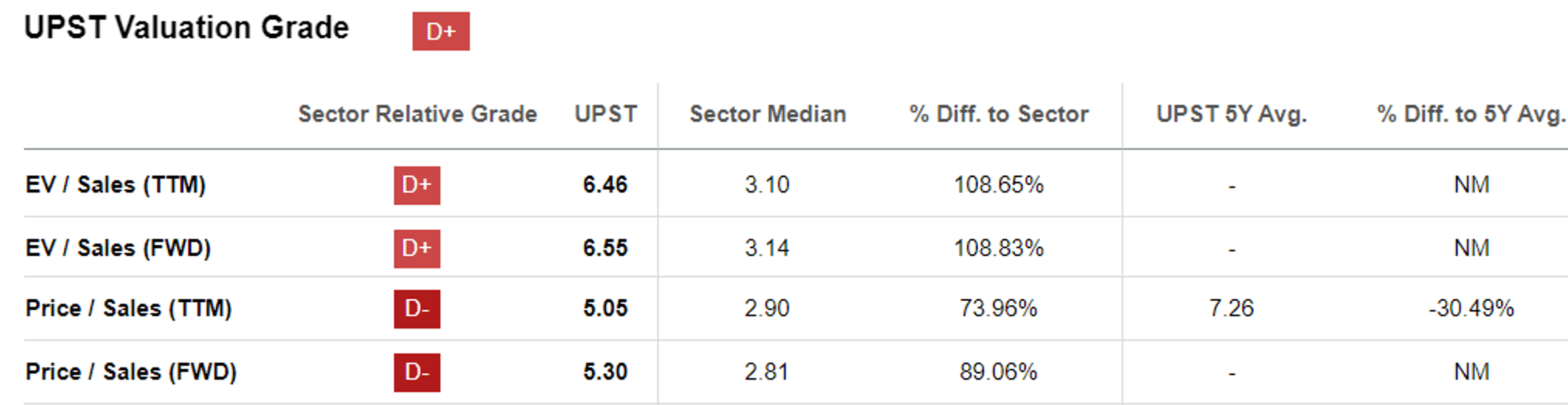

UPST Valuations

Seeking Alpha

Even so, it is undeniable that UPST is expensive at FWD Price/ Sales valuations of 5.30x, compared to its 1Y mean of 4.08x and the sector median of 2.81x.

When compared to its fintech/ lending peers, such as Affirm (AFRM) at 3.86x, SoFi (SOFI) at 3.05x, and Block (SQ) at 1.53x, we believe that there is a minimal margin of safety here.

This is especially since UPST is expected to generate a lower top-line growth at a CAGR of +18.7% through FY2026, compared to AFRM at +23.6% and SOFI at +18.5%, aside from SQ at +11.6%.

Readers must also note that UPST remains highly shorted at 26.71% at the time of writing, with insiders continuing to sell over the last twelve months.

Furthermore, while its stock-based compensation has moderated to an absolute number of $138M over the LTM (-22% sequentially), the ratio against total revenues has risen dramatically to 24.5% (+8.1 points sequentially).

This also meant that UPST’s shares outstanding has been growing at an accelerated rate of +6.3% sequentially or by +514.1% since FY2019 – with the erosion in shareholders’ equity occurring at a faster rate than the top-line growth.

Combined with the management’s laser focus on expanding “access to bank quality credit rather than to generate enormous profits,” i.e: lumpy monetization and the minimal margin of safety, we prefer to prudently reiterate our Hold rating here.