Richard Drury

TriplePoint Venture Growth (NYSE:TPVG) chopped its dividend by 25% this month due to insufficient net investment income and performance challenges in the debt portfolio. The dividend cut was widely expected, as the BDC’s shares traded at a dividend yield of up 19% prior to the announcement. I believe TriplePoint Venture Growth cut its dividend down to a more manageable level and the new distribution of $0.30/share is more sustainable.

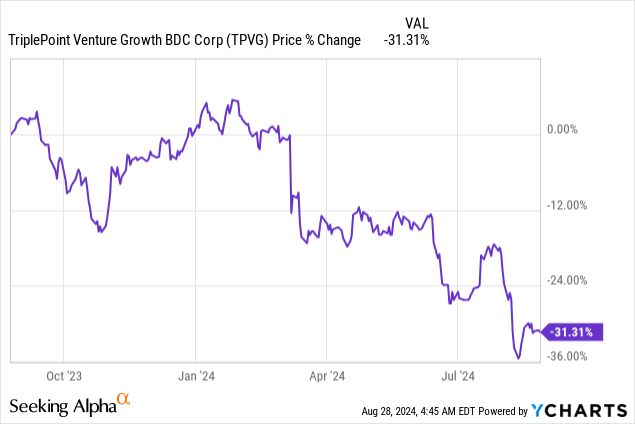

A rise in the non-accrual percentage, persistent investment losses and a steep drop-off in interest income/total investment income created significant selling pressure for TPVG, whose shares are now trading at a 15% discount to net asset value. In my opinion, the best option for income investors post-dividend cut is to stay the course, as the BDC’s distribution coverage profile should improve going forward.

Previous rating

In my June work Get Ready For A Dividend Cut, I argued that a dividend reset was highly likely and that investors should be prepared for an announcement in the next 1-2 quarters. The reason for this was that TriplePoint Venture Growth was suffering from a high ratio of non-performing loans in its portfolio and high investment losses. This in turn led to a weak distribution coverage profile and made a dividend cut that much more likely. Now that the dividend has been reset, I believe the distribution coverage profile is set to improve, and I therefore upgrade TPVG to hold.

Weak performance results lead to dividend cut

The second-quarter was not a great one for TriplePoint Venture Growth: the BDC suffered continual performance issues in its debt portfolio, which led to a surging non-accrual percentage as well as a good amount of investment losses. As a result, TriplePoint Venture Growth reported steep declines in net investment income and was forced to reset its dividend at a lower rate.

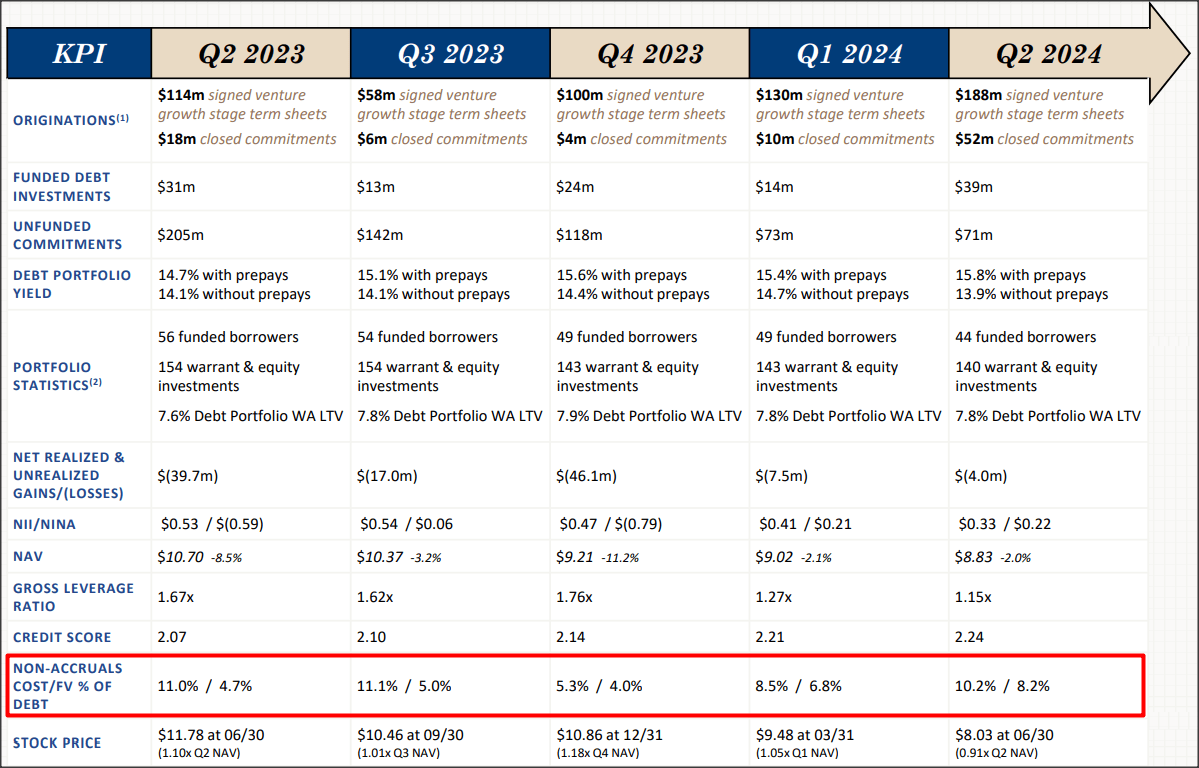

TriplePoint Venture Growth’s main issue is its weak balance sheet quality. Past loan originations have turned sour and the BDC was forced to put more loans on non-performing status. As a result, TriplePoint Venture Growth now sees one of the highest non-accrual percentages in the industry: at the end of the second-quarter, TriplePoint Venture Growth’s non-accruals surged to 8.2% (based off of fair value), showing an increase of 1.4 PP quarter-over-quarter. With the exception of Q4’23, the non-accrual trend has gotten progressively worse throughout the last year.

TPVG

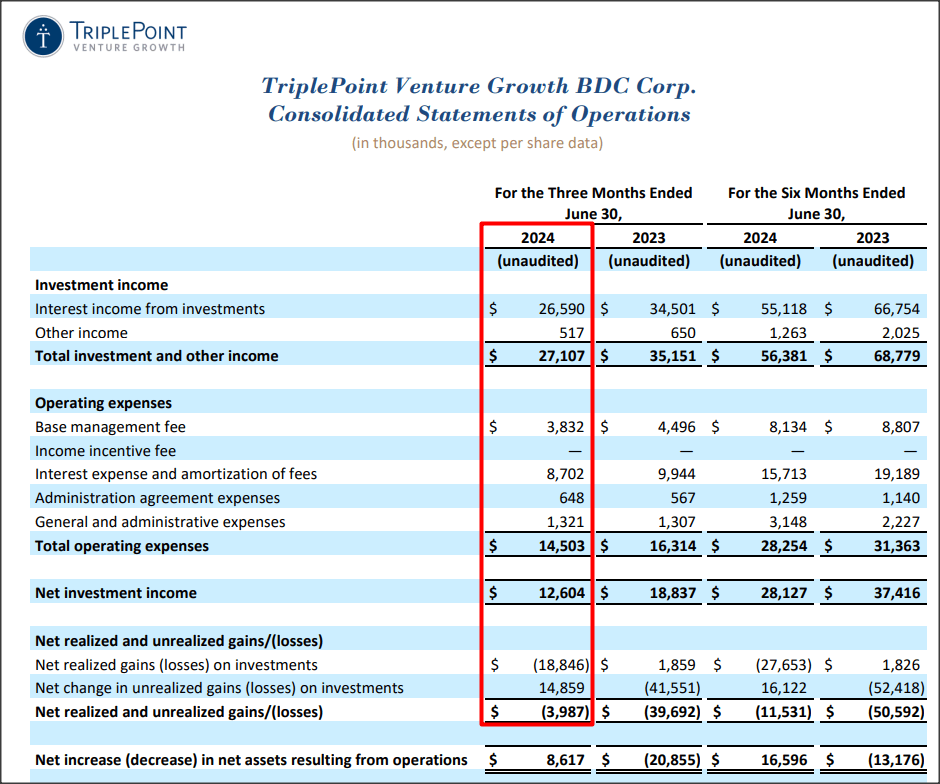

Because of TriplePoint Venture Growth’s credit problems, the BDC suffered a steep drop-off in its income in the second-quarter: the BDC reported a massive 23% year-over-year decline in interest income as well as in total investment income. Additionally, TriplePoint Venture Growth realized losses on debt investments totaling $18.8M in the second quarter, which resulted in a 2% Q/Q decline in net asset value.

Consequently, TriplePoint Venture Growth’s earnings scorecard revealed a much weaker distribution coverage profile in the second-quarter. The BDC generated a distribution coverage ratio, based off of net investment income, of only 0.825X in Q2’24 compared to 1.025X in Q1’24. Given the clear unsustainability of the dividend, TriplePoint Venture Growth lowered its future payout from $0.40/share to $0.30/share, showing a 25% decline.

Now that TriplePoint Venture Growth reset its dividend at a lower rate, the BDC’s distribution coverage profile is set to improve in the next quarter. However, there is still the risk that other investments will be moved to non-performing status. Therefore, I believe that TriplePoint Venture Growth still has a considerable amount of net investment income and dividend risks going forward.

TPVG

TPVG’s valuation

The dividend cut had an expected negative impact on the BDC’s valuation: shares of TriplePoint Venture Growth have sold at a small discount to net asset value ahead of the dividend cut, but are now trading at a much larger discount of 15% to net asset value.

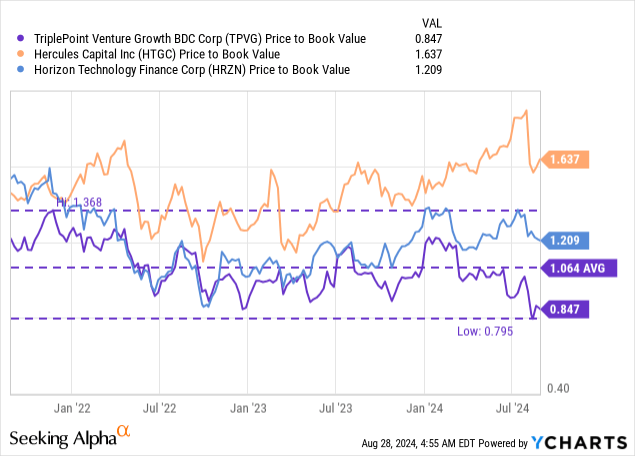

Horizon Technology Finance (HRZN) and Hercules Capital (HTGC) are rival BDCs in TriplePoint Venture Growth’s niche, as all companies focus on investments in the venture-backed growth sector. Hercules Capital is trading by far at the highest P/NAV ratio of 1.64X, largely because the BDC has been able to deliver steady and consistent net investment income results for the benefit of shareholders in the last several years. Hercules Capital’s strong second-quarter earnings sheet was the reason why I upgraded shares to buy just days ago.

TriplePoint Venture Growth is currently trading well below its longer-term average P/NAV ratio of 1.06X as well, and this discount is the direct result of the BDC’s credit problems and dividend cut. I believe it will be all but impossible for TPVG to return to P/NAV ratio of 1.0X in the short term as the BDC still has a high non-accrual percentage which points to lower future net investment income and which puts income investors off. Therefore, I would not be comfortable buying into TriplePoint Venture Growth at this point, but I would instead wait until the BDC’s credit issues have been resolved.

For investors that owned the BDC before the dividend got chopped, I believe the most sensible approach here is to wait and see how the credit situation develops. My longer-term price target for TriplePoint Venture Growth is the company’s net asset value ($8.83/share at the end of June), but I don’t see a short-term catalyst that could drive shares up to my fair value target in the near term. My fair value estimate would likely only get reached if the BDC succeeds in defending its new dividend and avoids incremental asset quality issues.

Risks with TPVG

The main risk for TriplePoint Venture Growth is a potential deterioration in the distribution coverage profile even after the BDC reset its dividend. Were this to happen, TriplePoint Venture Growth would likely create new negative sentiment overhang for its shares. If TriplePoint Venture Growth were to fail to cover its dividend with net investment income in the next 1-2 quarters, I would likely change my recommendation to sell.

Final thoughts

Income investors hate nothing more than a dividend cut and this is what TriplePoint Venture Growth unfortunately presented to shareholders this month: the new $0.30/share quarterly dividend reflects a sizable 25% reduction in dividend income for investors which, in my opinion, will weigh on the BDC’s valuation for a longer period of time.

I downgraded TriplePoint Venture Growth to sell in expectation of a dividend cut, which turned out to be correct, but I am not yet ready to upgrade shares to buy. The reason is the outsized non-accrual percentage in TriplePoint Venture Growth’s investment portfolio. The distribution coverage profile is set to improve after the dividend got chopped, however, but it is better, in my opinion, to play it safe here. Investors may want to stay on the sidelines and see how things develop with regard to TriplePoint Venture Growth’s non-accrual and net investment income trends before buying the BDC’s shares.