Canadian Highlights

- Trump made good on his 25% tariffs threat against Canada and Mexico this week. In the end it only lasted 72 hours, but the rollercoaster gave markets a fright.

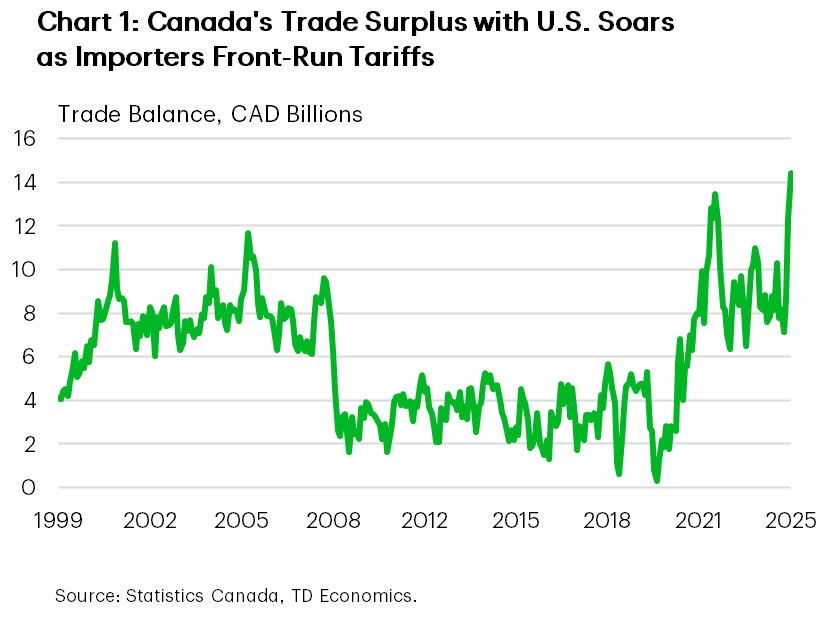

- Canada’s goods trade balance with the U.S. widened substantially in January, highlighting American companies are stockpiling supplies ahead of tariffs.

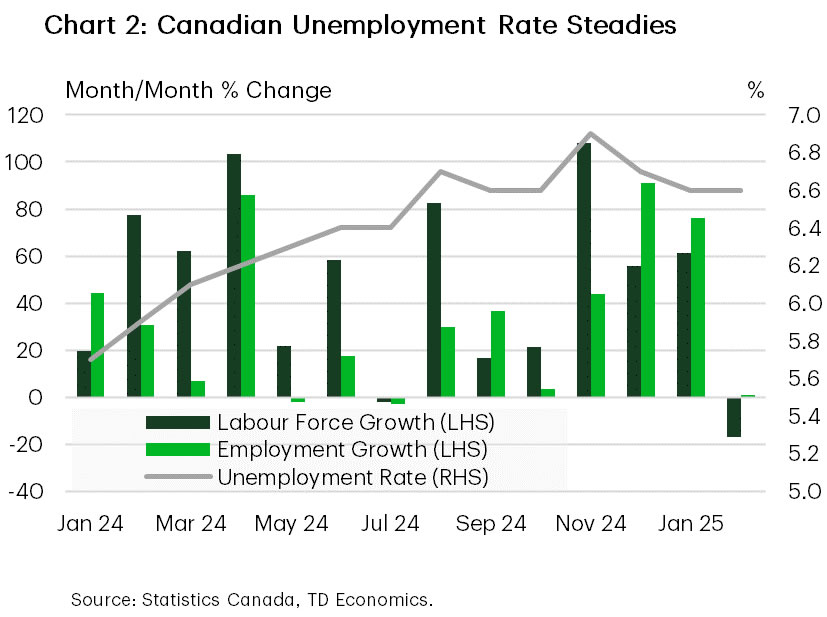

- Canada’s labour market got snowed-in in February. A labour force contraction balanced out the lack of job growth, keeping the unemployment rate steady.

U.S. Highlights

- On-again off-again trade policy continued this week as the U.S. implemented steep tariffs on imports from Canada and Mexico, but then backtracked, announcing carve-outs for USMCA-compliant imports until April 2nd.

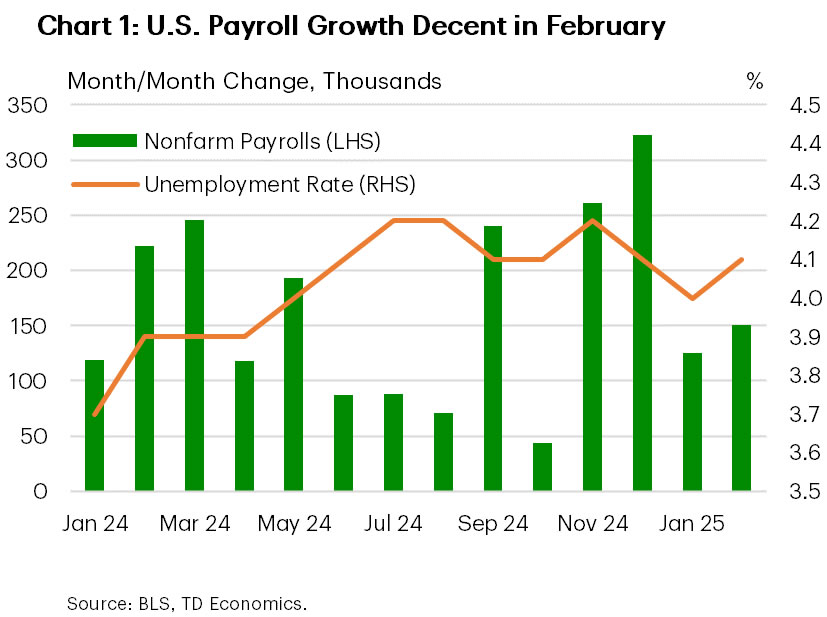

- U.S. hiring activity improved moderately in February, with the U.S. economy adding 151 thousand jobs last month. The unemployment rate ticked up from 4.0% to 4.1%.

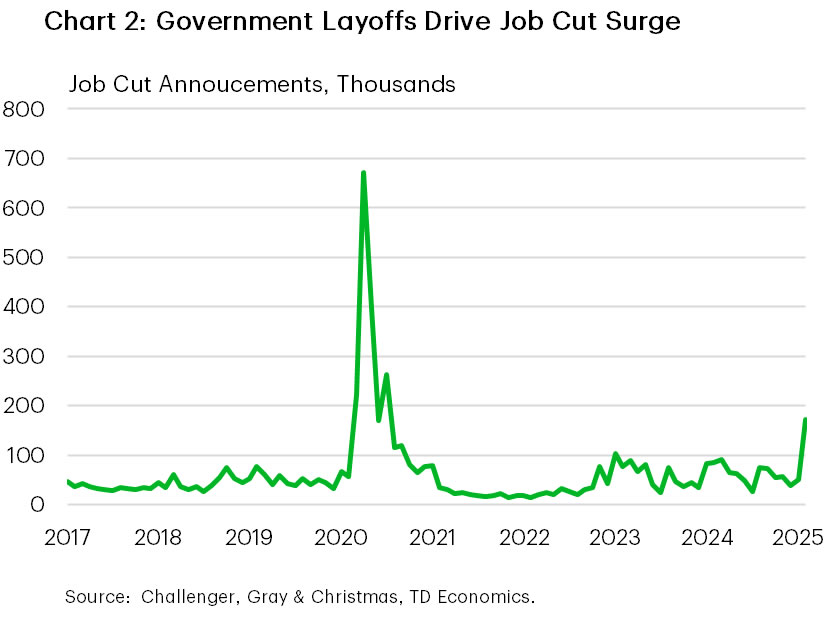

- One measurement of job cut announcements surged to 172 thousand in February, with government sector layoffs driving the surge.

Canada – Tariff-Induced Headaches

Canadians’ necks are likely sore from following the back and forth of this week’s tariff volleys. Beginning on March 4th, the previously unthinkable happened – the U.S. implemented 25% tariffs on Canadian and Mexican goods— with a 10% tariff on energy. Over the next 72 hours, Canada doubled-down on its retaliatory plan, the auto sector was granted a one-month carve out, and an executive order was signed pausing tariffs on Canadian and Mexican goods compliant with the United States-Mexico-Canada Free Trade Agreement (USMCA). And as it turns out, markets aren’t loving the uncertainty. Stocks continued to slide, with the S&P 500 and Canadian benchmark TSX dropping around 2% on the week. Canadian two and ten-year government bond yields rose modestly, helped by easing growth concerns, and the CAD nudged higher, finishing the week at 69.6 cents US.

Trade data confirmed that U.S. importers were proactive, and stockpiled Canadian goods to get ahead of tariffs. Canada’s monthly trade balance with the U.S. widened to over $14 billion in January, a new historical high (Chart 1). This was driven by a 7.5% month-on-month (m/m) surge in exports focused in the automotive sector, consumer goods, industrial machinery & equipment and energy products, which are key sectors impacted by tariffs. What’s more, since Trump won the election in November, nominal exports to the U.S. are up by a whopping 22%, the largest three-month gain on record, and by a considerable margin—excluding the frenetic export recovery in mid-2020. In the near-term, Canada’s economy will benefit from this tariff front-running, with early tracking showing a sizeable contribution from net trade to first quarter GDP growth. The expected broad-based weakness in the Canadian dollar could also buffer exports as trade flows constrict if and when tariffs set in.

Meanwhile, Canada’s labour market flatlined in February, with virtually no job created in the snowy month. Despite this, the unemployment rate held steady 6.6%, as the labour force contracted for the first time in seven months (Chart 2). On the margin, it was a weak report relative to expectations, but the readings were skewed by the intense snowstorms that occurred during the survey’s reference week. Almost half a million employees saw a reduction in hours worked because of the weather, pulling nation-wide total hours worked lower by 1.3%. This may have a negative impact on February’s industry-based GDP readings, but we’d expect a positive kick-back in March.

The Bank of Canada is set to make a highly anticipated interest rate announcement next Wednesday. For several weeks, we’ve expected the BoC to deliver a 25 basis point (bps) cut to take out insurance against a trade war escalation, despite the domestic economy running at a decent clip. Indeed, market pricing is aligned with our call, now predicting a 90% chance of a 25 basis (bps) rate cut, up from only 30% a couple weeks ago.

U.S. – Trade Policy Rollercoaster Rattles Markets

The first week of March proved to be a rollercoaster for financial markets. While plenty of important data reports were published, these generally played second fiddle to developments on the trade front. Early in the week, the U.S. imposed 25% tariffs on Canada and Mexico, and an additional 10% tariff on China. Canada and China retaliated, albeit in a more measured approach. As the trade conflict heated up, stock markets trended lower. But, slightly cooler heads seemed to prevail in the following days, with the U.S. first announcing a carve-out from tariffs for the auto sector, then announcing that all USMCA-compliant imports from Canada and Mexico would be exempt from the 25% tariff until April 2nd.

At a first glance, the latest backtracking on the tariff measures can be viewed as a positive development. However, the amount of trade that will ultimately be tariff exempt is still unclear, with at least some portion of imported goods from Canada and Mexico expected to face a higher tariff rate than they had until recently. The complicated nature of trade rules and processes is likely to cause delays and disruptions to supply chains.

Furthermore, the fact that this latest move provides only a partial reprieve from higher tariffs, with trade tensions likely to flare up once again in a month from now, does little to alleviate concerns. In fact, come April 2nd, tariff action is expected to involve many other countries. On that day, the U.S. is expected to impose reciprocal tariffs on all nations that place tariffs or tariff-like barriers on U.S. goods.

Tariff threats have already effected business decisions, as many firms ramped up shipments early in the year to get ahead of tariffs. Imports surged 10% in January, which widened the U.S. trade deficit to a record of $131 billion. This is likely to weigh on growth in the first quarter. The stop-start nature of policy moves also undermines consumer and business confidence, and is expected to weigh on investment decisions.

For the time being, the job market remains on solid footing, with the U.S. economy adding 151k jobs in February (Chart 1). However, job growth is likely to soften ahead. Apart from the potential for trade policy uncertainty to weigh on near-term hiring intentions, federal layoffs related to DOGE also continue to mount. Job cut announcements surged in February, with a steep increase in layoffs in the government sector being the largest contributor to the overall tally (Chart 2). The potential for a government shutdown, which could happen as early as next weekend, may pose additional downside risk over the near-term.

The Fed will have to carefully weigh the risks of a potential slowing in economic activity against the risk of a near-term boost in inflation. The price measures in both the Manufacturing and Services ISM surveys increased in February. For the time being, the Fed is expected to remain on hold, but come summer we could see chair Powell taking out the interest rate scissors.