Monty Rakusen

There are compelling reasons to favor a long position in copper. The AI boom and push toward EVs will require significant infrastructure investment around the world and other capital projects promoted by the US government, including the Inflation Reduction Act and the CHIPS and Science Act, are tailwinds.

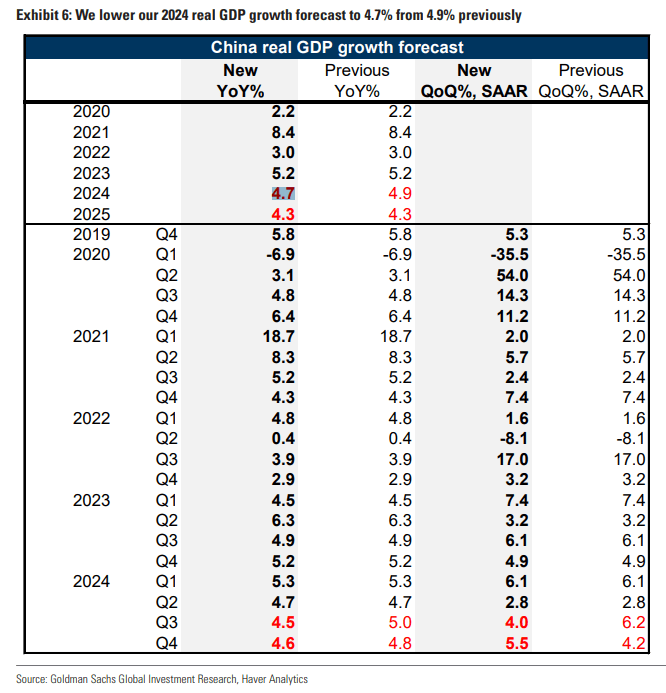

But the elephant in the room is China. So long as the world’s second-largest economy remains challenged, it will likely be hard for the industrial metal to perform well. Just this past weekend, Goldman Sachs took down their 2024 China GDP forecast, citing weak activity measures and softer-than-expected employment and retail sales data.

I have a hold rating on Southern Copper Corporation (NYSE:SCCO). I see the $78 billion market cap copper industry company within the materials sector as priced somewhat richly on valuation when considering earnings growth in the years ahead. Its technical situation is actually appealing, however, and I will detail key price levels on the chart to monitor at the end of the analysis.

Goldman Reduces Its 2024 China GDP Forecast

Goldman Sachs

SCCO is a global copper producer and touches many points of upstream and downstream activities. It also engages in the mining of iron ore, molybdenum, and even precious metals to a lesser extent. The Arizona-based firm reported a solid Q2 report back in July. Quarterly non-GAAP EPS of $1.21 beat the Wall Street consensus forecast of $1.06 while revenue of $3.1 billion, up a very strong 36% from year-ago levels, was a material $278 million beat.

Net income soared 74% versus Q2 2023 to $950 million and its margin expanded from 23.8% to 30.5%. Of course, the first half of this year featured very high copper prices, and we’ve seen a significant pullback in the metal over the last handful of months. But SCCO proved timely with a 6.6% sequential increase in quarterly copper production, taking advantage of the temporarily high prices. Its zinc and molybdenum production numbers were likewise robust.

Shares traded just slightly higher in the session that followed the second-quarter report. Investors might have been uneasy with the high $332 million in capex, but Southern Copper’s management team announced a $0.60 dividend along with a small stock dividend. Operationally, they detailed the resumption of operations at its Tia Maria project on the earnings call.

Ahead of earnings due out next month, the options market has priced in a significant 6.2% earnings-related stock price swing when analyzing the at-the-money straddle expiring soonest after the release, according to data from Options Research & Technology Services (ORATS). Seeking Alpha’s data show a consensus of $1.11 of operating EPS on revenue of $2.94 billion.

Key risks include a weaker global economy, which would pressure demand and prices for copper. Higher labor costs would be another headwind along with a spike in borrowing costs. Geopolitical conflicts and regulatory concerns are ongoing risks for this multinational and capital- and labor-intensive firm.

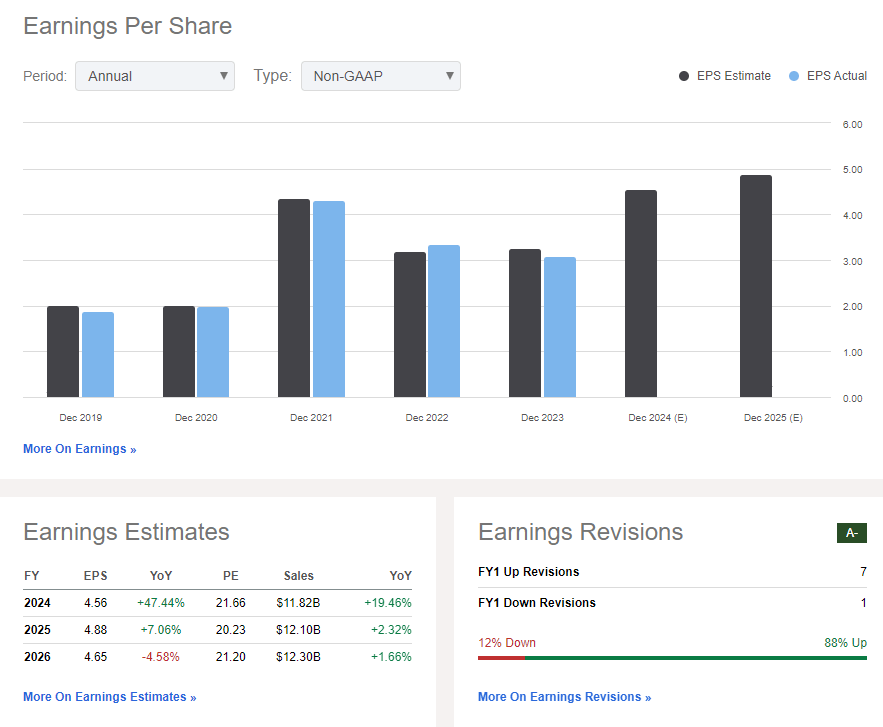

On the earnings outlook, 2024 is indeed seen as a year of abnormally high growth. EPS is forecast to rise next year, but hold under $5 through 2026. That gives us as investors a good sense of what normalized EPS is. Moreover, annual revenue is expected to approach $12 billion in 2024 and only gradually increase from there. With a low free cash flow yield during what was a bull market in copper, I’d like to see improved cash flow metrics.

Southern Copper: Revenue, Earnings, Revisions Trends

Seeking Alpha

On valuation, if we assume normalized EPS of $4.60 and apply the stock’s five-year average price-to-earnings multiple of 21.3, then shares should trade near $98 – right where it closed last week. I see downside risk to the P/E, however, given that the earnings growth story is simply not as strong or durable as that of the broader S&P 500.

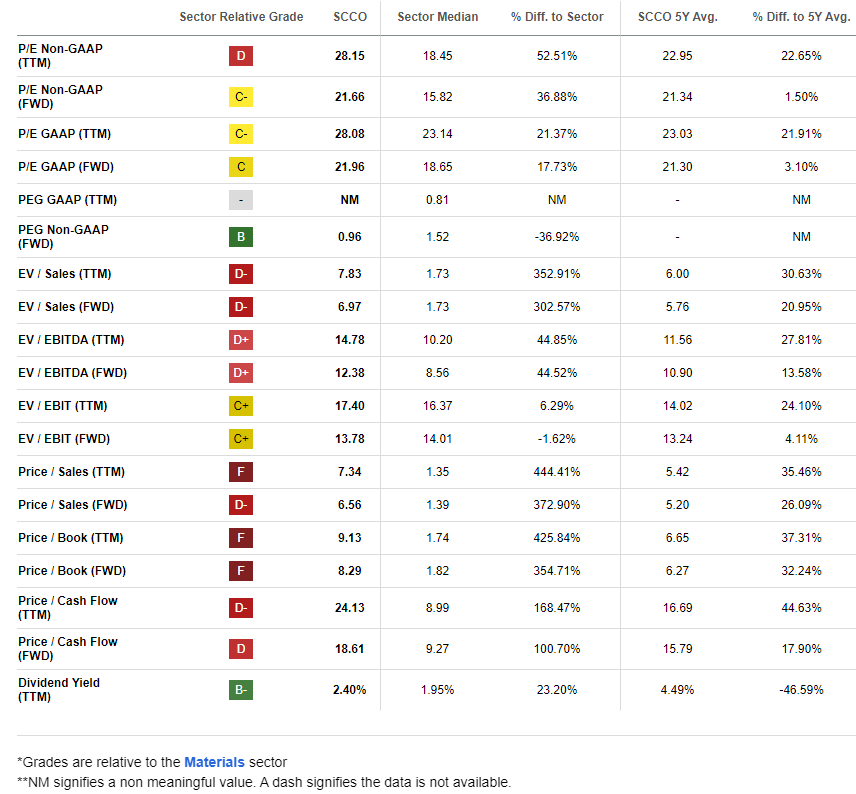

Giving SCCO the same earnings multiple as the SPX seems slightly aggressive, so I see downside risks to the valuation. Shares trade expensive on a price-to-sales basis too.

SCCO: Lukewarm Valuation Metrics, High P/S

Seeking Alpha

Compared to its peers, SCCO features a weak valuation rating, while its growth trajectory is lukewarm at best. But profitability metrics are healthy (though after a boom year, that’s to be expected).

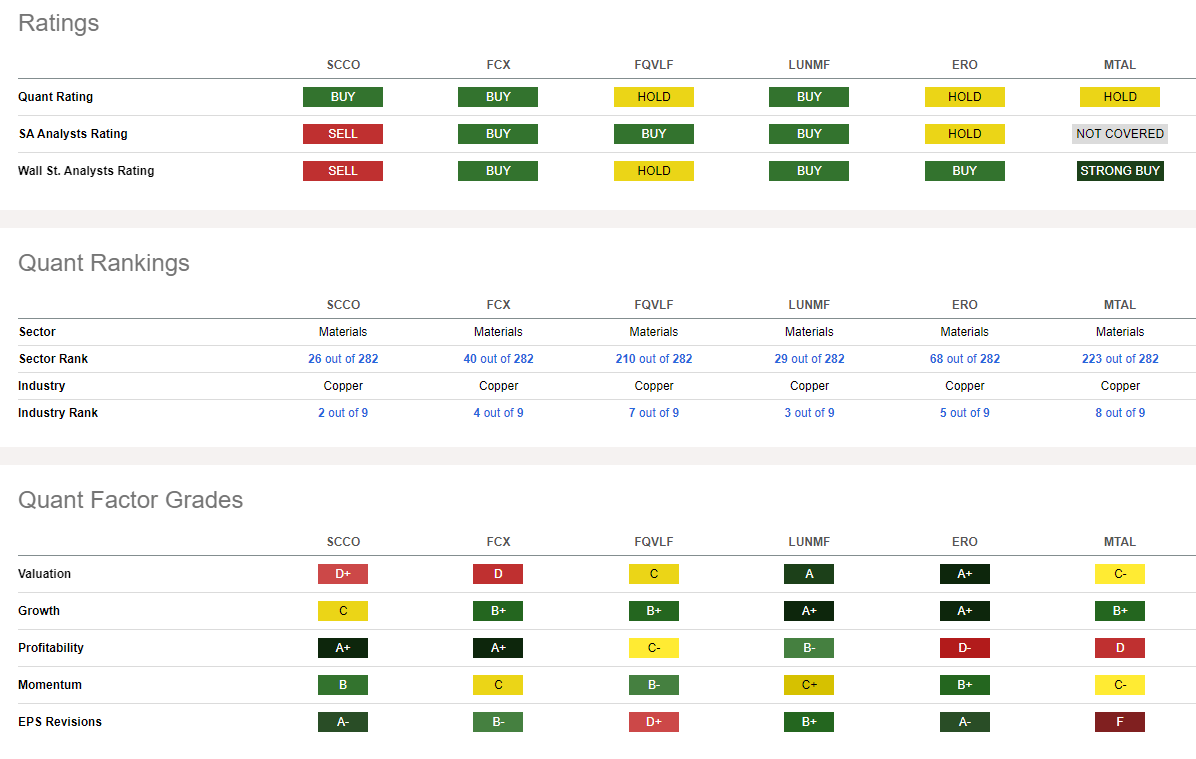

Share-price momentum is graded with a B, but both absolute and relative price action has been weak since May, when copper peaked around $5 per pound and $10,000 per ton. EPS revisions have been sanguine, though, given a solid 7 sellside upgrades in the past 90 days compared with just a single downgrade.

Competitor Analysis

Seeking Alpha

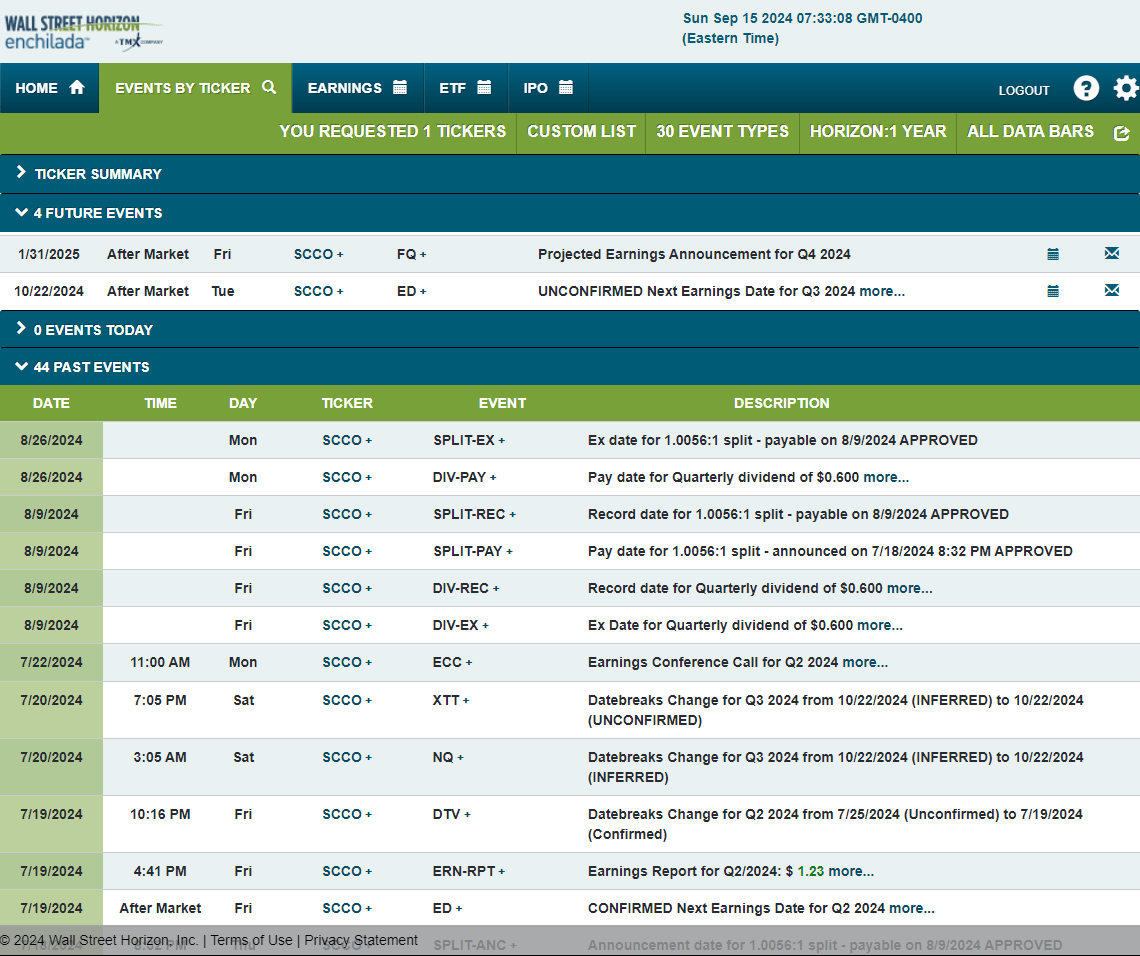

Looking ahead, corporate event data provided by Wall Street Horizon show an unconfirmed Q3, 2024 earnings date of Tuesday, October 22 AMC. No other volatility catalysts are seen on the calendar.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

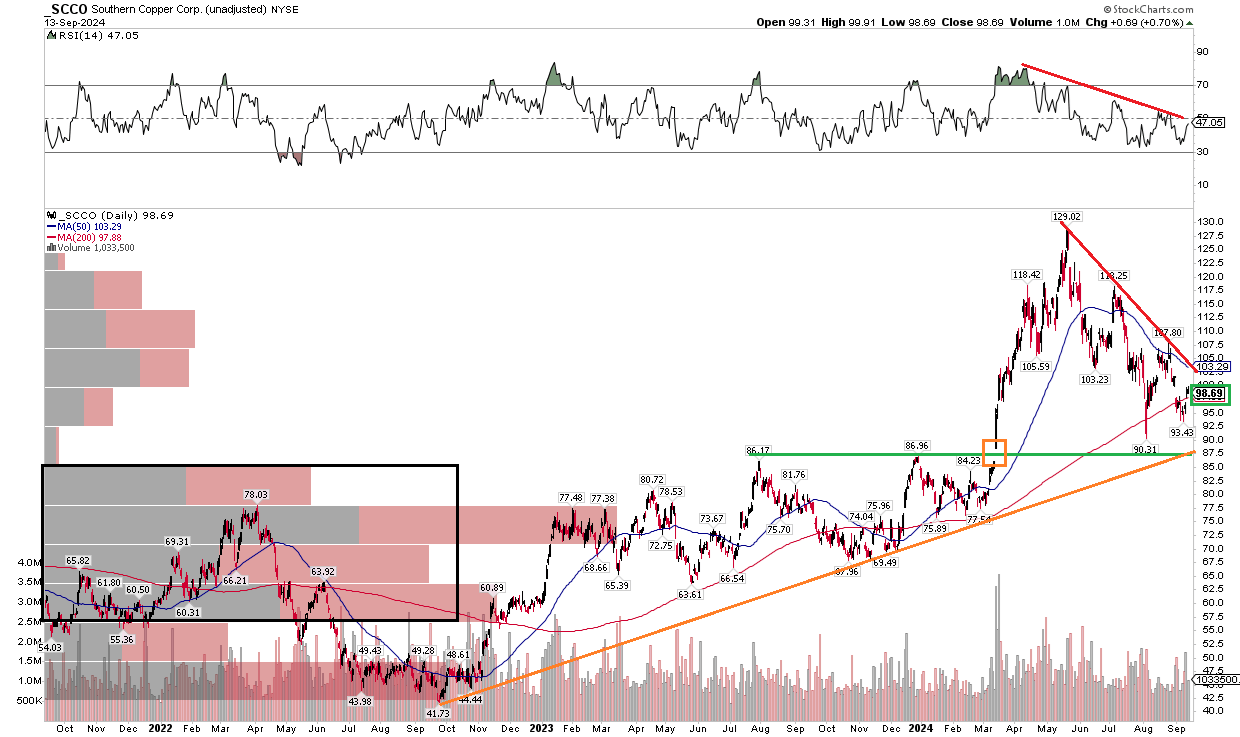

While I am worried about the valuation amid global macro risks, SCCO’s technical chart offers an opportunity for investors. Notice in the graph below that shares have approached key long-term support in the mid to high $80s. After peaking just shy of $130 in the second quarter at the height of copper’s rally, the stock pulled back by more than 30% to $90. The high $80s is a confluence of key support. First, an area of polarity comes into play from the range highs from August 2023 through the following January. Next, an uptrend support line enters the scene at the same spot.

Also, take a look at the long-term 200-day moving average – shares are attempting to hold that indicator line, but the bears are showing their muster to an extent by keeping SCCO from bouncing hard off the 200dma. There is also a downtrending resistance line just about the $100 mark. Furthermore, the RSI momentum oscillator at the top of the chart confirms the move lower in price. I’d like to see SCCO either dip to $87 to buy on a pullback or rally through the $108 high a month ago.

Overall, SCCO is near critical support, offering a chance to buy the uptrending long-term chart amid a correction.

SCCO: Shares Approaching Key Support

Stockcharts.com

The Bottom Line

I have a hold rating on SCCO. I see the valuation as fair at best, while the technical situation is encouraging after a significant retreat off the May 2024 all-time high.