Ozgur Donmaz

Thesis

On July 18, 2023, I started coverage of Daktronics (NASDAQ:DAKT) and explained how the company performed after posting buoyant Q4 2023 earnings results, despite the ongoing supply chain issues and inflationary pressures. Sales posted a record high, thanks to robust demand and smart pricing strategies; meanwhile, growth in gross profit margins was underpinned by the company’s efforts to keep costs down despite higher expenses and growing economic risks and I pointed out concerns over long-term drops in share value and dividends, plus inflation and global market risks. Still, their plans for growth and new tech stood out, so I gave them a “Hold” rating.

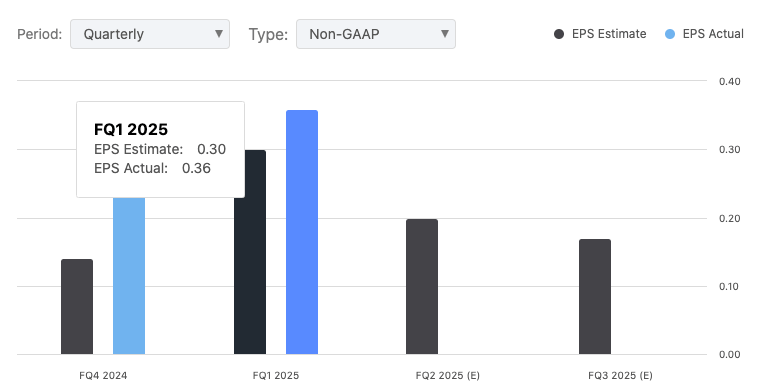

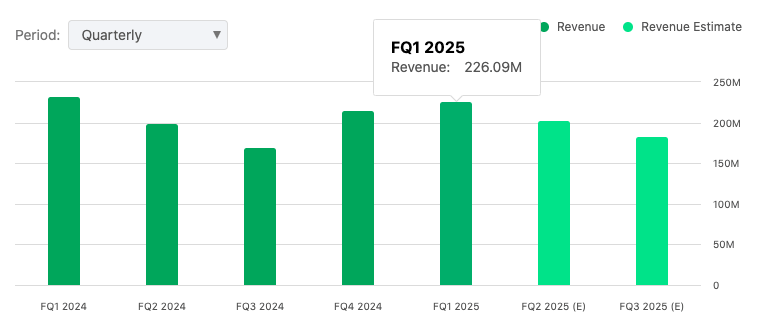

Since my original take, Daktronics has made a serious comeback. The stock’s up 88.18%, crushing the S&P 500’s 23.58% gain. That jump shows they’ve been executing well, and investors are feeling pretty good about their future growth. I’m checking in today to say Daktronics has shown strong resilience and serious growth potential after its Q1 2025 earnings. They beat expectations with an EPS of $0.36…

Seeking Alpha

…and revenue of $226.09 million.

Seeking Alpha

Despite my earlier concerns about inflation, dividends, and market risks, they’ve stayed on track with their growth strategies, boosted efficiency and tapped into strong demand. Because of their solid performance and undervaluation, I’m upgrading Daktronics.

About Daktronics, Inc.

DAKT FQ1 2025 Slide Deck

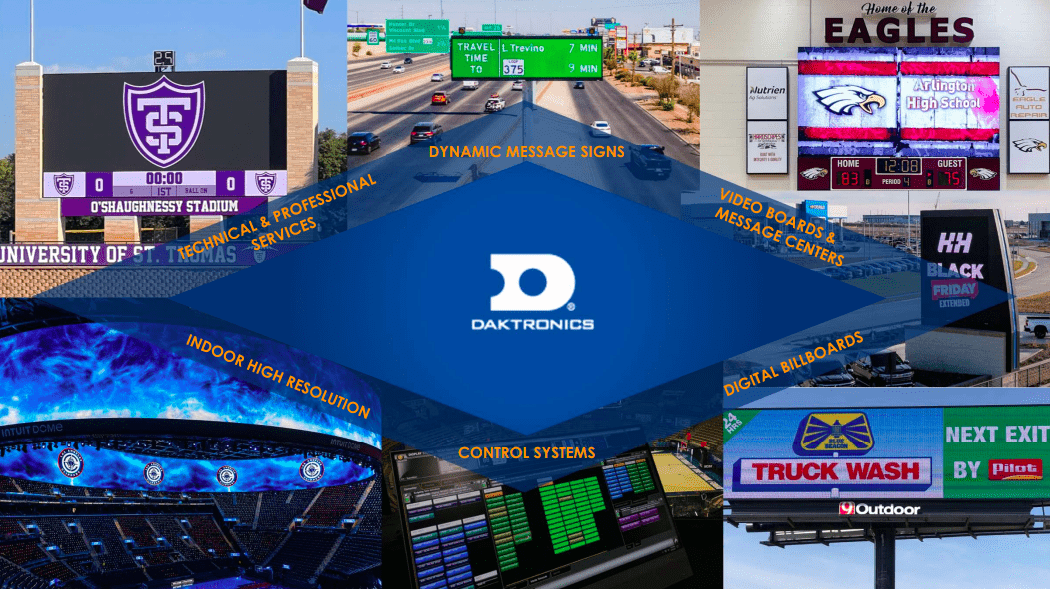

Daktronics, Inc., founded in 1968 in Brookings, South Dakota, makes everything from video screens at sports stadiums to electronic billboards everywhere. Its products serve the sports, transportation, and advertising industries. It has now diversified its business into smart transportation systems, dynamic message signs, and full audiovisual solutions.

Daktronics was already growing by leaps in the 1990s when the company started installing scoreboards for top international sporting events, such as the 1996 Atlanta Olympics, and replacing legacy big-display signs, such as New York City’s ‘Zipper,’ with large-scale electronic display screens. The company also developed new partnerships with major international corporations, such as Omega Electronics.

What sets Daktronics apart is its proprietary Venus software, designed to enable clients to operate dynamic video displays – and messaging – of any scale and complexity. The company has continued to improve its products and has diversified its customer base. Today, it employs close to 2,800 people, with offices and installations spread across the globe.

Daktronics Stock Performance vs. S&P500

Fast Graphs

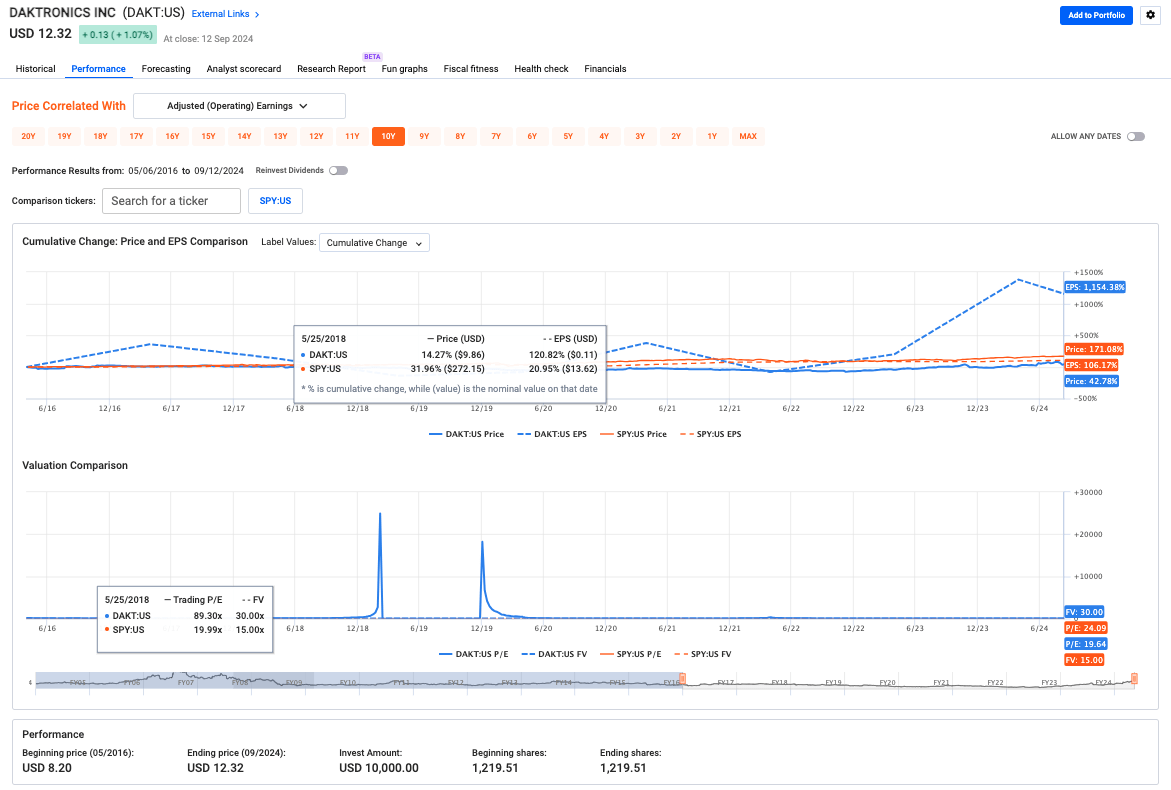

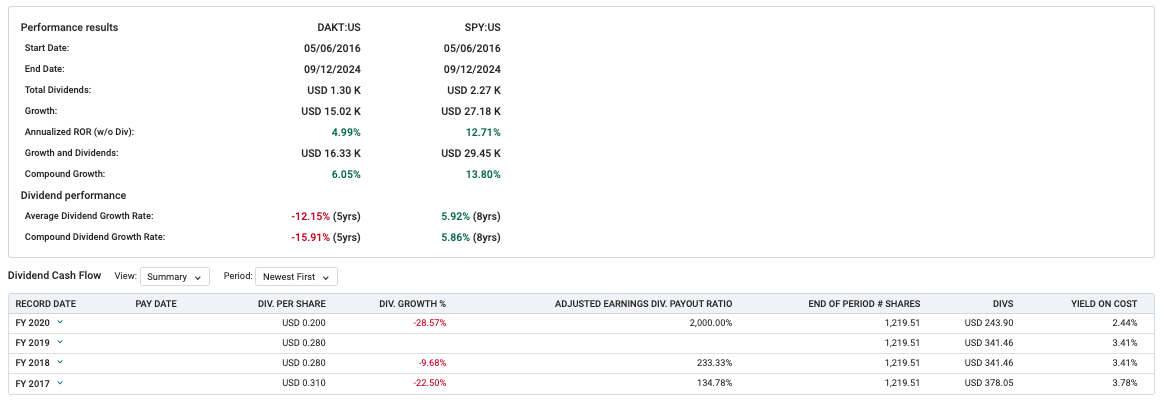

Daktronics’ stock price demonstrated a smooth but positive upward trajectory between 2016 and 2024. This equals a 4.99% annual return, which isn’t bad but falls short compared to the S&P 500’s 12.71%. Daktronics definitely underperformed the overall market, which I mentioned in my “cautious” rating call last year. The bigger gains started from the day it cracked through its long-term technical resistance—around July 2023 at $7.50—that acted nicely as a cushion and converted to a support level after a brief selloff in February this year.

Seeking Alpha

As with my previous analysis, the biggest problem was the decline in the dividend. Over five years, the average dividend growth rate dropped by -12.15%, while the compound was worse at -15.91%. If you’re a dividend growth investor, you may want to steer clear because, over the long term, the broader market SPY offered a much better total return.

Daktronics Growth Metrics

Seeking Alpha

While diluted EPS growth year-over-year plummeted 68.96%, the forward estimate shows a 98.32% rebound, crushing the sector’s 7.28%. This massive 1,250% potential jump suggests earnings could bounce back fast. The 393.33% rise in EPS GAAP growth year-over-year hints at better core profitability.

Seeking Alpha

Cash flow also shows strength: levered free cash flow is up 163.59%, compared to the sector’s 22.57%. This means DAKT is generating a lot more cash after paying its debts. Over five years, levered free cash flow growth hit 94.53%, but free cash flow per share is down 11.93%, showing some inconsistency in delivering value to investors.

Seeking Alpha

On the bright side, working capital grew 26.46%, way above the sector’s 1.05% which shows DAKT is managing liquidity well, which could help in a cash crunch.

Demand for Dynamic Content in Public Spaces

Data Intelo

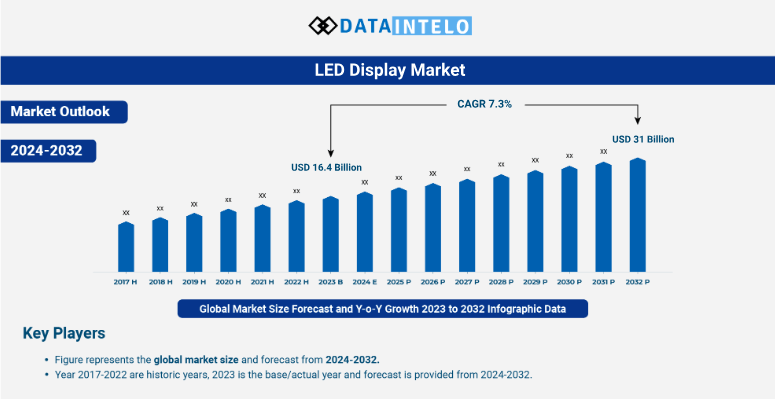

The LED display market, where Daktronics plays, is set for big growth in sports, transportation, and advertising. Between 2024 and 2031, the market is expected to grow at an annual rate of 7.3%. The Asia-Pacific region will lead the charge, encouraged by fast urbanization and growing infrastructure, especially in China and India. The appetite for high-res visual experiences that form part of the stadium and arena experience is fueling demand.

Grand View Research

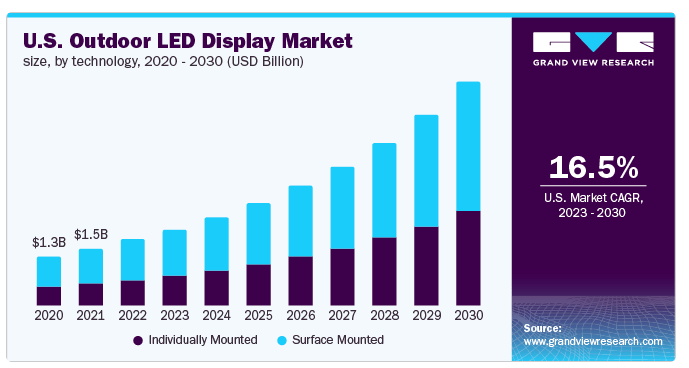

Recent forecasts suggest outdoor LED displays like billboards and video walls are expected to register a growth rate of up to 16.5% annually, and the demand for dynamic, real-time content in outdoor ads and public spaces is driving this trend. Also, energy-efficient solutions like mini-LED and micro-LED tech are trending and taking up more market share, which is helping push this market forward.

Daktronics Q1 2025 Earnings Highlights

Daktronics reported strong execution in Q1 2025, with sales hitting $226 million. That’s a 4.7% bump from Q4 2024. They also boosted operational efficiency, with gross margins up to 26.4%.

Margin Growth Drivers

Some of the things that helped boost margins were an increase in orders from high schools compared to last year and last quarter, thanks to more schools switching to full video displays. They also introduced a new product with higher margins, helping both customers and their own profits. Last quarter, they completed two big display projects, one in Texas and one in Hawaii, showing the growing use of digital technology in schools. And since they’ve already hit their target operating margin, management says there’s still room to grow that margin further.

Pricing and Competitiveness

Pricing is always a factor in margin growth, and while it’s competitive (mostly from Southeast Asia) Daktronics has a lot of control over how the screens and systems are made, and they have a feature set that’s very difficult for competitors to match. That full-service aspect, where they set the equipment up, it looks great, and the customer gets the most out of what they’re buying, is all together what’s kept them strong competitive-wise.

Daktronics’ New Orders Surge

Additionally, new orders jumped 11% year-over-year, showing strong demand in key markets, which helped the company pull in $19.5 million in operating cash flow, proving its solid liquidity. A strong balance sheet and a $267 million backlog point to a steady flow of future work and seasonal backlog growth is expected to keep rising through Q3 FY2025, reflecting confidence in future demand and project completion.

Regarding demand, the company won new projects with the University of Connecticut, Alabama, and Auburn. Sports and entertainment events should keep growing as venues continue to renovate to keep fans happy and attract athletes. The attention is shifting to the spaces outside the core – entryways, atriums, concourses – and their Narrow Pixel Pitch products (high-resolution LED displays for close viewing) are a great fit for those spaces, and demand is still healthy.

Commercial Sector Resilience

In the commercial sector, they deal directly with resellers, who serve a much broader client base, including military, transportation, retail, restaurants, casinos, building owners, as well as those in the out-of-home advertising sector. Year-to-date, commercial orders are up from last year, with steady demand from display users, property owners, and advertisers. The market can be volatile from economic changes and ad spend, but, for now, it’s holding up. Helping those independent out-of-home operators has bolstered the sale of large, attention-grabbing displays called ‘spectaculars.’

The plan is to keep growing in these core areas, working more with AV integrators to push their Narrow Pixel Pitch products, especially for control rooms in the military, utilities, and transportation. In transportation, orders have increased compared to last quarter and last year. They’re focused on landing more projects for intelligent transportation systems, airports, and mass transit. They recently snagged a contract with Dallas Area Rapid Transit to roll out displays across their network.

Daktronics Digital Transformation Plan

Lastly, the company’s digital transformation plan is on track: key goals for 2025 and 2026 aim to boost profits and big projects, like those for Penn State, the University of Texas, and the LA Clippers, show strong demand in live events which keeps driving the company’s growth.

Meanwhile, in terms of that ‘transformation plan,’ by 2025, the company will release new generations of service and management tools for scheduling and speeding up operations, reducing response times, cutting down on errors, and increasing the quality of its services for the user overall.

They’re also automating parts of the sales and quoting process via phased rollouts beginning in 2026 while targeting product and structural costs to remain competitive.

Simply put, the point of these digital upgrades is to enable them to cut costs or boost productivity.

Daktronics’ Valuation

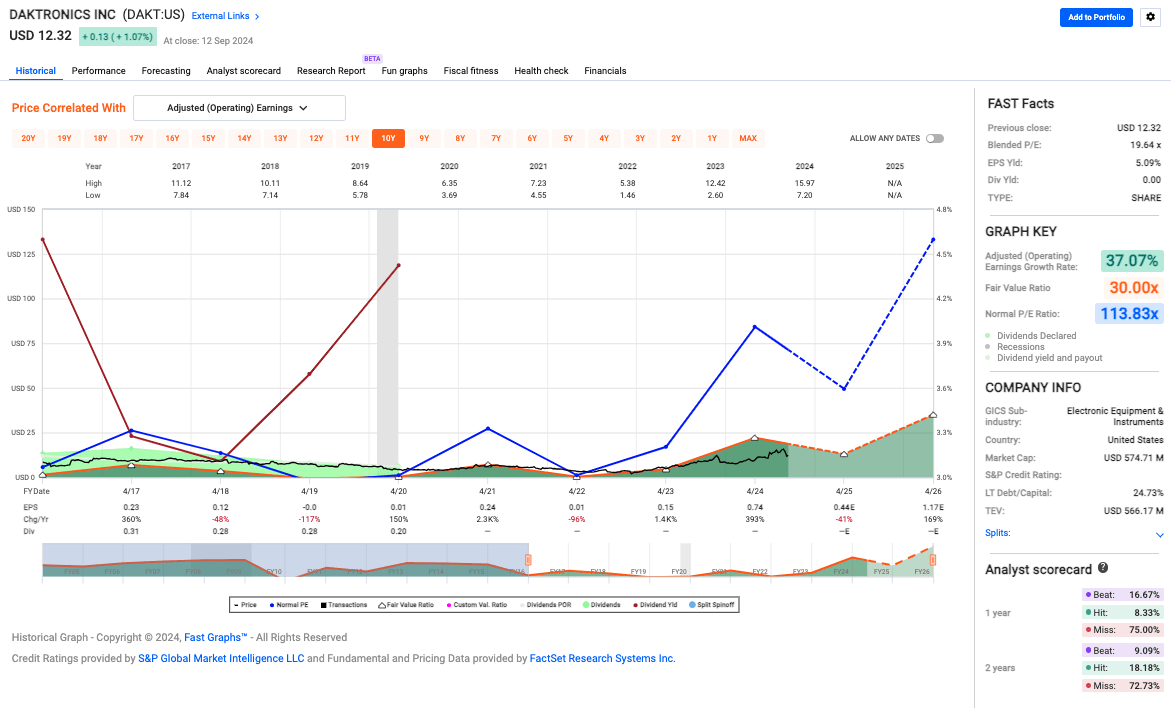

DAKT’s blended P/E ratio of 19.64x tells me that the market is valuing Daktronics fairly (though it’s still priced higher than most of its competitors). All in all, with a fair value ratio of 30.00x, Daktronics looks undervalued, meaning there’s room for price growth if the market catches up.

Fast Graphs

The gap between fair value and its normal P/E (113.83x) hints the market hasn’t fully accounted for its growth potential. I also want to point out that DAKT’s growth rate stands at an impressive 37.07%. For a company with a market cap of $574.71 million, that’s solid.

Bottom line: as for valuation, Daktronics is an outlier. Its current price and blended P/E ratio, compared to its fair value, show there’s serious upside potential.

Daktronics’ Risks & Headwinds

Daktronics still faces some challenges. Revenue grew from last quarter, but Q1 FY 2025 numbers were down from last year’s record. Operating expenses climbed with wage hikes, more hiring, and consulting fees, which could hurt profitability if not controlled. International sales, though up 20%, are still slow due to economic and political uncertainties, limiting global growth.

The backlog, once high from supply chain issues, has mostly leveled off, hinting at more moderate growth ahead. Price-sensitive challenges still affect some customer segments. Daktronics may not hold the same market share it had before COVID, especially in competitive regions. Unclear market share data makes it tough to gauge their overall position.

Furthermore, planned investments of $8 to $10 million for fiscal 2025 (the digital transformation resources I mentioned earlier) could hit operating margins, adding short-term cost pressure. However, I’m not overly concerned about this cost, as I think it’ll pay off in the long run.

And finally, for anyone considering investing here for the first time, you should understand that Daktronics is very seasonal, especially in sports installations, and those trends can cause performance to ebb and flow a bit. The commercial business is tied to the economy and advertising budgets, so if that is weakening, it could hurt them going forward.

Daktronics’ Rating

I’m upgrading Daktronics to a “Buy.” Sure, dividends dropped and costs are up short-term, but the company bounced back strong. Earnings and margins look good for the long haul and the stock’s undervalued, so there’s room to grow, especially with demand high and their digital strategy on point.