imaginima

As the indices continue to surge higher, I’ve taken an interest in stocks that are more off the beaten track. Some of these companies include international picks in Japan, but as well as ETFs that focus more on the value end of the spectrum. My concern is that many companies in the traditional growth sectors such as tech could be in bubble territory, so I am now more interested in smaller businesses that have strong growth potential.

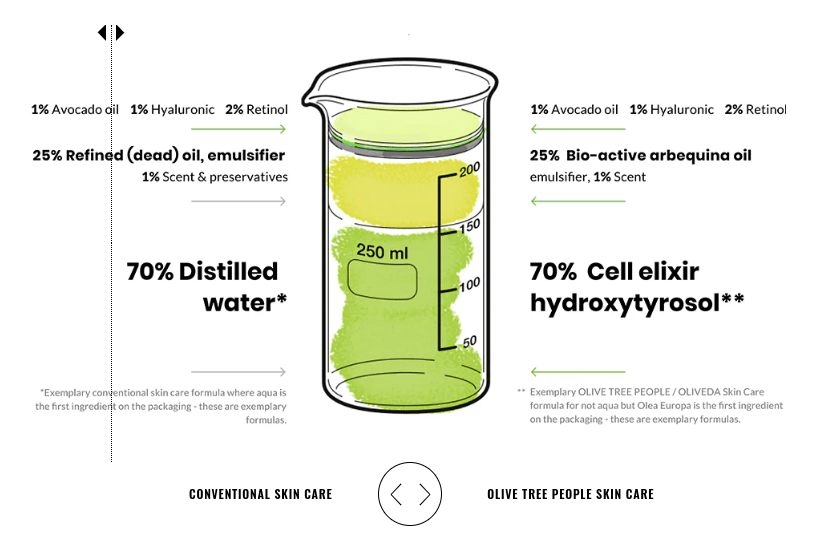

One company that has come on my radar is Oliveda International (OTCPK:OLVI). For those who are unfamiliar with this brand, it operates in the natural and holistic beauty industry, with a niche in combining cosmetics with mountain olive trees. Specifically, the firm offers serums, creams, elixirs and more that claim to help restore the user’s natural beauty. Conventional skin care products are mostly distilled water, but OLVI aims to differentiate its products by replacing the water content with ‘cell elixir hydroxytrosol’. This is claimed to be a “highly potent and bioactive cell elixir of the olive leaf” and aims to impart its regenerative and anti-aging properties onto the user.

Oliveda

The big picture for investors is that its subsidiary, Olive Tree People, has reported outstanding growth recently, with a 2,850% increase in sales within the first year of operations in the United States. My view is that OLVI deserves a place in investors’ portfolios, thanks to its dirt-cheap valuation and its realistic prospects for disrupting the cosmetics industry. The risks of investing in OLVI are significant, but I feel that owning a small position could pay off substantially even for conservative investors.

Company Overview

Oliveda International was founded by Thomas Lommel in 2003. The company’s genesis started with Lommel’s experimentation with the compounds found in olive trees. Lommel then patented a process for extracting these compounds, which has become one of Oliveda’s key competitive advantages. Water is the key base ingredient found in cosmetics, with my estimate being that 90% or more of products use water as one of their key formulations. The company then started trading in Europe and has been in business for 20 years. I think that through a combination of marketing savvy and replacing the (comparatively useless) water filler content with bioactive compounds such as hydroxytyrosol and polyphenols, the firm achieved commercial success, with $3.86 million in sales reported last financial year.

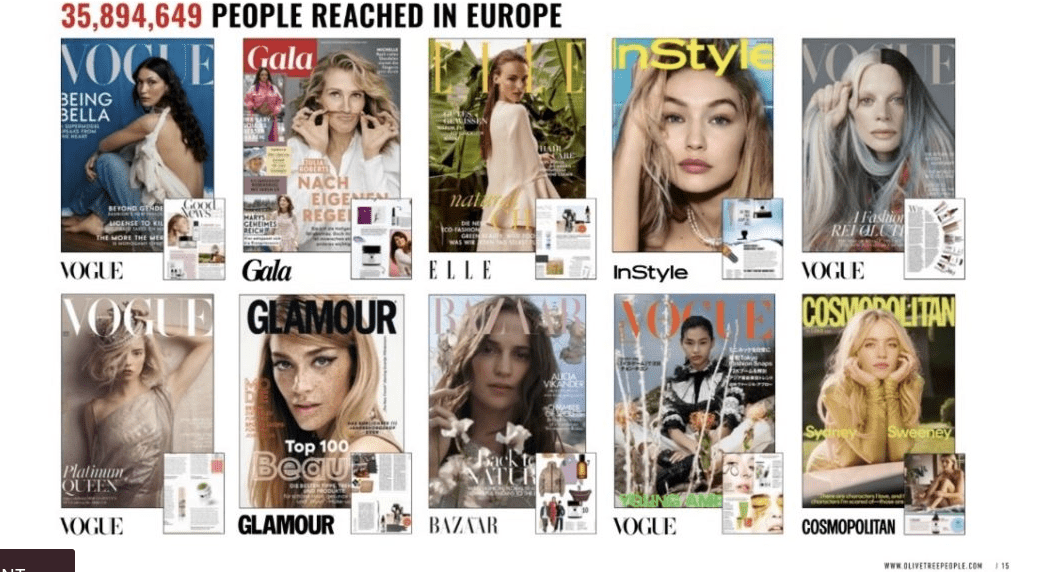

Finally, Oliveda has been featured in numerous women’s cosmetics, and fashion magazines, and has also been endorsed by celebrities such as Gigi Hadid, Charlize Theron, and Madonna.

Oliveda International

Finally, Oliveda is planning to list on the Nasdaq, which, I feel, will garner it considerably more credibility from investors as well as being easily purchasable from most brokerages. Management has guided that it will pursue its listing on the Nasdaq in October 2025.

Company Operations

The company is split between its European base (located in Germany) and its expanding presence in the U.S. through its subsidiary, Olive Tree People. Lommel has made some very bullish predictions regarding the Oliveda’s potential in the near future, stating “the future of beauty is waterless, and the waterless beauty movement will change the beauty industry over the next two to five years. In our second year in the United States, we are projected to reach more than 50,000 waterless beauty consultants and more than $100 million in revenue.”

Waterless beauty consultants are its agents as part of its direct sales strategy, which is an integral part of the brand’s operations. One thing I appreciate about Oliveda is that this approach is not a multilevel marketing (MLM) strategy, but instead relies on the agents solely selling Oliveda’s products to the end users. It’s claimed that prospective consultants simply pay the $50 joining fee, and they can receive training and marketing materials to help them start their business. I prefer this approach over the MLM model, as Oliveda is fundamentally a premium brand that requires a strong positioning in the market. In saying that, almost anyone could make a few bucks by recommending their products, and the consultants receive up to 35% in commissions from their sales. Driving the point home further is that the company also claims a 84% retention rate with its customers.

In addition to growing its network of beauty consultants, it also has a long-term view of expanding its retail presence. “The Company intends to open more corporate-owned stores, with a target of 60 stores worldwide in 5 years,” according to its most recent quarterly report.

Financials

For FY2023, Oliveda reported revenues of $3.86 million, a decrease from $4.93 million in 2022. The gross profit for 2023 was $2.5 million, down from $4 million in 2022. Although commentary was sparse in the report, I feel that this could be chalked up to its pivot to the American market, where significant growth is taking place.

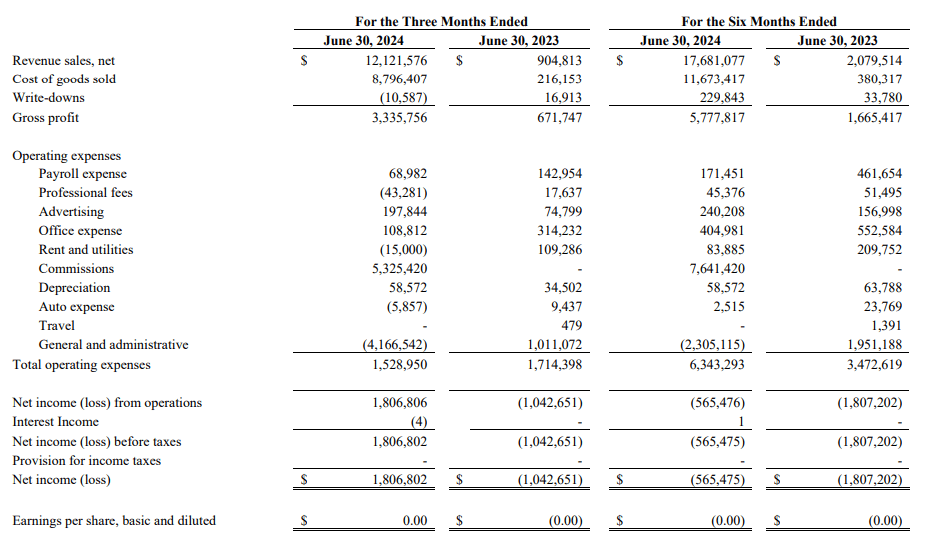

Meanwhile, for its most recent June quarter, the firm’s revenue surged to $12.12 million, from $0.94 million in the previous corresponding period. As previously mentioned, a large chunk of this growth came from its Olive Tree People subsidiary taking off in the U.S. Net income also saw a sizable boost, coming in at $1.8 million, up from a net loss of $1 million.

Oliveda International

In terms of liquidity, the firm has $6.7 million in cash and is cash flow positive, with total liabilities of $0.81 million. Around 80% of those total liabilities are in the form of accounts payable. The firm has no current promissory or convertible notes, and there are no long-term debts recorded on its balance sheet.

My view then is that Oliveda is in a strong financial position to help achieve its ambitions in the cosmetics industry.

Valuation

If management’s vision for the company is to be believed, then the firm could be substantially undervalued at current levels. In a press release, the firm is targeting sales of $108 million and a stock price of $12.50 per share.

Over the past year, the firm has seen a massive boost to its valuation on news of its success in the U.S. market, with it increasing over three thousand percent.

Seeking Alpha

One thing to note with Oliveda’ valuation is that it has 617,056,809 shares outstanding at the time of writing. Although it reported increasing net income last quarter, its earnings are currently negative. To be more specific, my calculations put its EPS at $0.0029, which of course is rounded down to $0, and this also means its P/E is negative as well. I don’t foresee the company needing to raise additional capital in the future due to its very high sales, gross profit, and net income growth expectations, with the cash generated from sales being able to cover its operational expenses. Its price-to-sales ratio of 90.53 gives me some confidence that there is even more significant growth potential ahead of it.

In order for Oliveda to have a positive EPS of $0.01, it would need to grow to approximately $6.17 million. This means the current net income of $1,806,802 would need to increase by about $4.36 million to reach this target. Even if we assume that its net income growth remained constant last quarter, it should be able to reach positive EPS territory within the next four quarters at the latest. I then believe that it’s undervalued relative to its growth potential, as I don’t see many substantial roadblocks to inhibit this growth, aside from a few exceptions.

Risks

One of the key risks with Oliveda is that there’s nothing stopping other companies from also using olive products in their cosmetics, or some other type of base ingredient other than water. Although Oliveda would retain its first-mover advantage in this situation, I think this hypothetical outlines that its competitive position it’s far from rock solid and may be comparatively weaker than it looks like on the surface.

Another potential risk that I see is the risks of ongoing dilution to shareholders. If the company experiences a downturn and sales don’t grow fast enough to cover its expenses, its history indicates that it will continue to make equity raises to free up cash. I am recommending Oliveda as a buy now as I believe that its dilution has ceased for the foreseeable future, but this is definitely something that investors want to keep on their radars as a potential issue.

Conclusion

I think that Oliveda is a buy and that it has plenty of gas left in the tank to continue to surge higher. The company has great growth potential, and it’s headed towards breakeven profitability on an EPS basis within the next four quarters if all else remains equal. The stock is undeniably risky, but owning even a small position could allow investors to achieve great returns as it continues to disrupt the cosmetics industry.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.