f11photo/iStock via Getty Images

Above: Denver metro looms as a key market for Monarch Casino & Resort, Inc.’s move to Colorado.

Premise: Amid the AI/tech deluge that has swung volume away from many industry groups stands the casino sector, with prices at very attractive P/Es. Many of today’s investors do not remember when casino stocks, per se, commanded such strong volumes, if not frenetic runs between 1978 and 1987.

Since then, there have been some fat returns north, and periods of flat lined trading. The only gambling stocks that have experienced soaring prices since then have been the sports betting subgroup. DraftKings (DKNG), for example, was losing money but delivering phenomenal sales growth. It ran its price from single digits to over $72 amid the craze in 2021. Casino stocks that have moved, attracted buyers mostly focused on their sports betting results, not live casino results. It is part of the overall obsession of anything moving online.

But I believe it is the brick and mortar casino sector that is loaded with solid entry points. It is timed right now for buying.

google

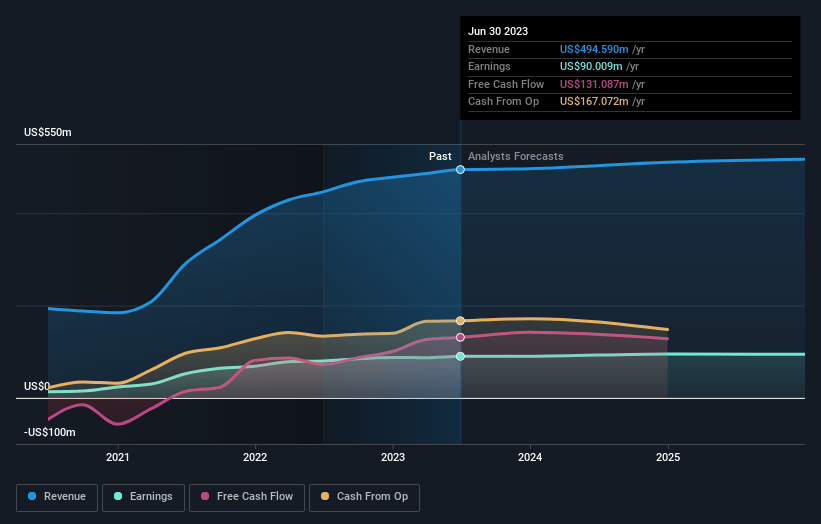

Above: Clear sailing ahead for MCRI through next year at least.

We have looked at that sector primarily using P/Es as a fairly representative metric of investor sentiment going forward now.

Of course, we realize there are literally a dozen measures of casino performance usually applied to analyst coverage of the sector.

We only look at market cap, price and P/Es as enough to impart a quick snapshot of investor confidence or lack of it. We realize the absence of many metrics typically in comparative analysis are not part of this viewpoint. As noted, in these days of massive data and shrunken attention spans, core metrics like P/Es have a place in helping build investor awareness.

Here are the “big 6”selected because they represent current opportunities stuck in prices comfortably below their value expressed by their P/Es. We assume that P/Es include baked-in appraisals of balance sheet leverage investors consider in buy, sell or hold decisions. It is a metric containing many metrics that often provides the final decision on action.

Above: This above all is what smart management over time yields to investors

In an article to come, we will present a similar look at the online gaming and sports betting sub-sector stocks. They have similarities but, on balance, are essentially different businesses.

Here’s our “big 6” selected stocks we believe are undervalued as expressed in their P/Es. All at one point or another have been on our SA buy or strong buy lists: The tickers are in order below. Some percentages rounded:

Monarch Casino & Resort, Inc. (MCRI), Boyd Gaming (BYD), MGM Resorts International (MGM) Wynn Resorts (WYNN) PENN Entertainment (PENN), Red Rock Resorts (RRR).

Company Market cap Price now P/E

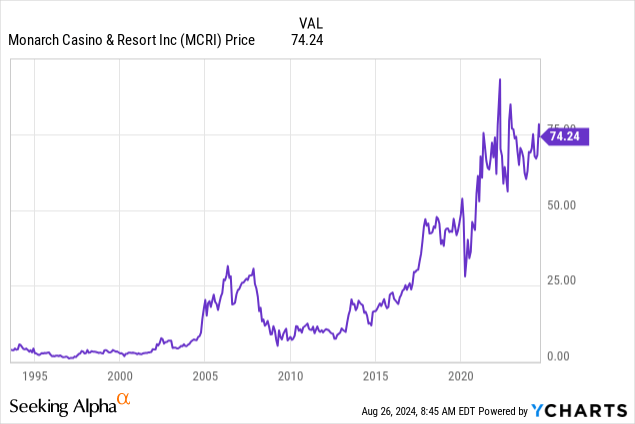

MCRI $1.37b $74 17X

BYD 5.5b 60 11.6X

LVS 29.90 40 19.04

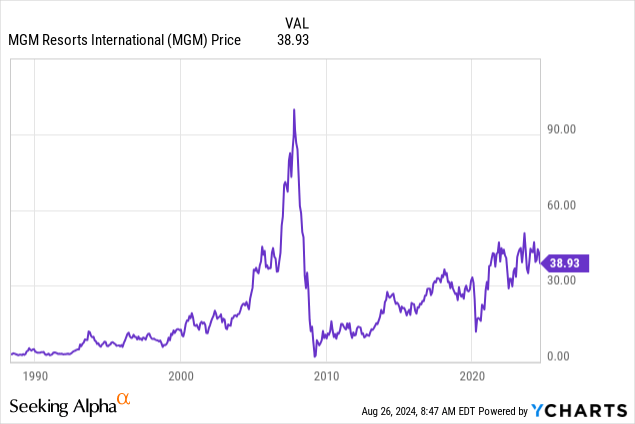

MGM 11.8b 39 14.6X

WYNN 8.5b 77 9.9X

Red Rock 5.9b 56 19.33X.

*Note: Caesars Entertainment (CZR) and PENN P/Es are in negative P/E territory and are not listed here, but are covered in our regular cycle of reporting.

- Compared with S&P 500 (SP500) average P/Es 27.7X

- Average sector P/Es for this group: 11.13X

- 12 analysts regularly covering the sector expect an overall upside of 31% for the group.

- By most standard appraisals of a P/E range which consensus analysts generally consider healthy for a strong buy or buy recommendation, the group above can clearly be characterized as value stocks.

Monarch: is among our long-term picks that have nearly tripled since our coverage began before 2016 when its strong upside momentum began.

This stock has turned in a particularly powerful performance since 2016. It was under $20 when I began following it. It was then a Reno-based casino with one fairly large property run with a golden touch in operations and wisely conservative growth prospects.

What I liked then and now was the business approach of the family management: father and both Farah sons. It kept debt low, operating expenses in line and marketed with great savvy and understanding of the markets they shared. They grew from the 1970s with motels.

They expanded their Atlantis crown jewel in Reno, reaching a sharply predictive projection of the Reno/Sparks, Nevada market—plus the flow of business from northern California. The property now has 848 rooms and over 64,000 square feet (0.59 ha) of gaming space. It opened in 1974 and has been expanded several times.

Only when they were convinced that Atlantis was performing near peak vs. capacity, did they turn their heads elsewhere. Then they studied a market they determined had the most viable future profile:

Black Hawk Colorado checked all the boxes.

The Black Hawk casino market had a strong gaming profile. Under an hour’s drive from Denver, it had a younger population below the national casino visitor profile of age 42. It has household income higher than average due to a large population of tech related employment, and virtually no disruptive elements to the outdoor and indoor lifestyles of the area.

MCRI continued to meet and beat earnings forecasts at the same time it was developing a street level casino it had purchased. The rebranded Monarch Black Hawk was expanded at a steady pace from a garage and casino space addition to a 504 room hotel, which debuted in 2022.

The two Monarch casinos now consistently operate above industry averages in margin and profitability. The savvy and prudence of the Farah family management has paid off for investors.

I believe Monarch is still a low-risk, high return buy because its strategy works. Once management sees results from Black Hawk steadily reaching its projections, I have little doubt that the sharp eye of Monarch management will find another market to explore. Or perhaps expand in Colorado.

And as I have also noted in several Seeking Alpha articles on MGM Resorts, its strategy to become a dominant global player wherever casinos go will support a strong upside low-risk buy. At under $40 at a 14.6X P/E I see it difficult to pass.

Above: MGM since the COVID-19 year of 2020 and management shift is very attractive as a relatively undervalued stock. Their “asset light” strategy of selling its realty to REIT is now focused on global expansion.

As noted above, the Monarch stock now trades at $74 with a P/E of 17.03X. Along with MGM, it is our current best pick among the group. MGM’s assets and presence in every big gaming mode globally is undervalued by its P/E.

Macro performance expectations

Brick and mortar casinos have a sunny future

US casinos drew 84m visitors in 2023, a record. Despite headwinds in key regions like extended poor weather, erratic hold in high-volume areas, increased competition and some early bankroll fatigue showing up sporadically, the overall growth of the casino business is running up to a 12% CAGR to 2030. (Some forecasters put it at 10.4% CAGR. Either number spells healthy).

The US casino industry did grow over 10% YOY in 2023, reaching $67b. Visitation to Las Vegas has always been a harbinger of industry health. Grandview Research projects an average CAGR for the US industry at 12% up over prior 10% forecasts through to 2030.

In 2023, Vegas alone hosted over 40m visitors, two million more YOY. Regional casinos reached $11.3b and are expected to double by 2030 to $21.9b. Population growth is still strong by national standards by state, but has begun to wane due to skyrocketing costs of housing. But the outward flow of California refugees from taxes and lifestyle threats continues strong. Retirees from the northeast who like the resort lifestyle offerings are continuing to rise.

Near 200,000 Californians have moved to Vegas since 2020. So the overall industry profile in which these value plays exist is highly positive.

In general, I’m looking for price targets (“PTs”) for this group in the 30%+ range by year’s end or early 2025.

The casino industry was propelled by the allure of legal casino gambling spread shortly after Atlantic City burst on the scene in 1978. What followed was a spread of now of 1,500 (commercial and tribal) casinos in 21 states, plus tribal bringing it near 44, which have some kind of gambling legal, which ultimately feeds casino visitation.

Conclusion

We realize the many metrics used to round out an investor decision to buy, sell, hold, add or sell down go far beyond just P/E. But we also believe the single most long-term metric to judge value is the P/E. There could be many reasons why some stocks trade with a bloated P/E, of course. But again, snapshots can tell a story that is sometimes lost in a portrait.