malerapaso

Overview

When it comes to dividend investing, business development companies are the place to go when you’re looking to collect a higher than normal dividend yield. MidCap Financial Investment (NASDAQ:MFIC) operates as a business development company that generates its earnings by making various forms of debt investments to middle market companies. I previously covered MFIC back in May and issued a buy rating. Unfortunately, the total return since then has been negative. While this can be attributed to a variety of unknowns, I believe this underperformance can be sourced to uncertainty around the merger and a rising non-accrual rate as the underlying portfolio companies feel the burden of elevated interest rates.

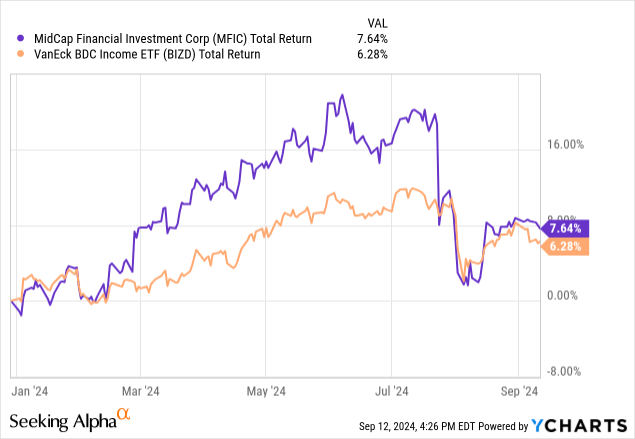

When we compare the total return of MFIC against the VanEck BDC Income ETF (BIZD), we can see that MFIC still outperforms on a YTD basis. The changes in price look to be a bit similar, which I find to be a bit reassuring for as an investor that typically maintains a long-term outlook with my holdings. While MFIC has lacked in price growth, the total return can be totally attributed to the continued high distribution rate of 11.3%. This double-digit dividend is what makes MFIC most appealing for income oriented investors that are looking to generate a stream of income from their portfolio.

When I previously covered MFIC, one of the reasons I issued a buy rating was because I felt that management would be able to benefit from the announced merger with some Apollo closed end funds. While the close of the merger is still fresh, and we’ve yet to see how this will play out, I still remain optimistic and believe it can be a source of future growth. Over the last earnings call, management seems to have a positive outlook on the whole situation, which is also reassuring.

Beginning with the mergers, we are pleased to announce that on July 22, MFIC successfully closed its mergers with AFT and AIF, two listed closed-end funds managed by Apollo. We believe these mergers mark an important step in MFIC’s evolution to becoming a leading pure-play middle-market BDC.

The completion of this merger leaves MFIC uniquely positioned to benefit from interest rate cuts. While interest rate cuts can be a negative thing for earnings potential, MFIC benefits from an increased level of liquidity that can help capitalize on deals that can offset any headwinds in earnings. Additionally, their portfolio continues to be structured in a way that limits risk and is highly diverse across sectors.

Updated Portfolio Strategy

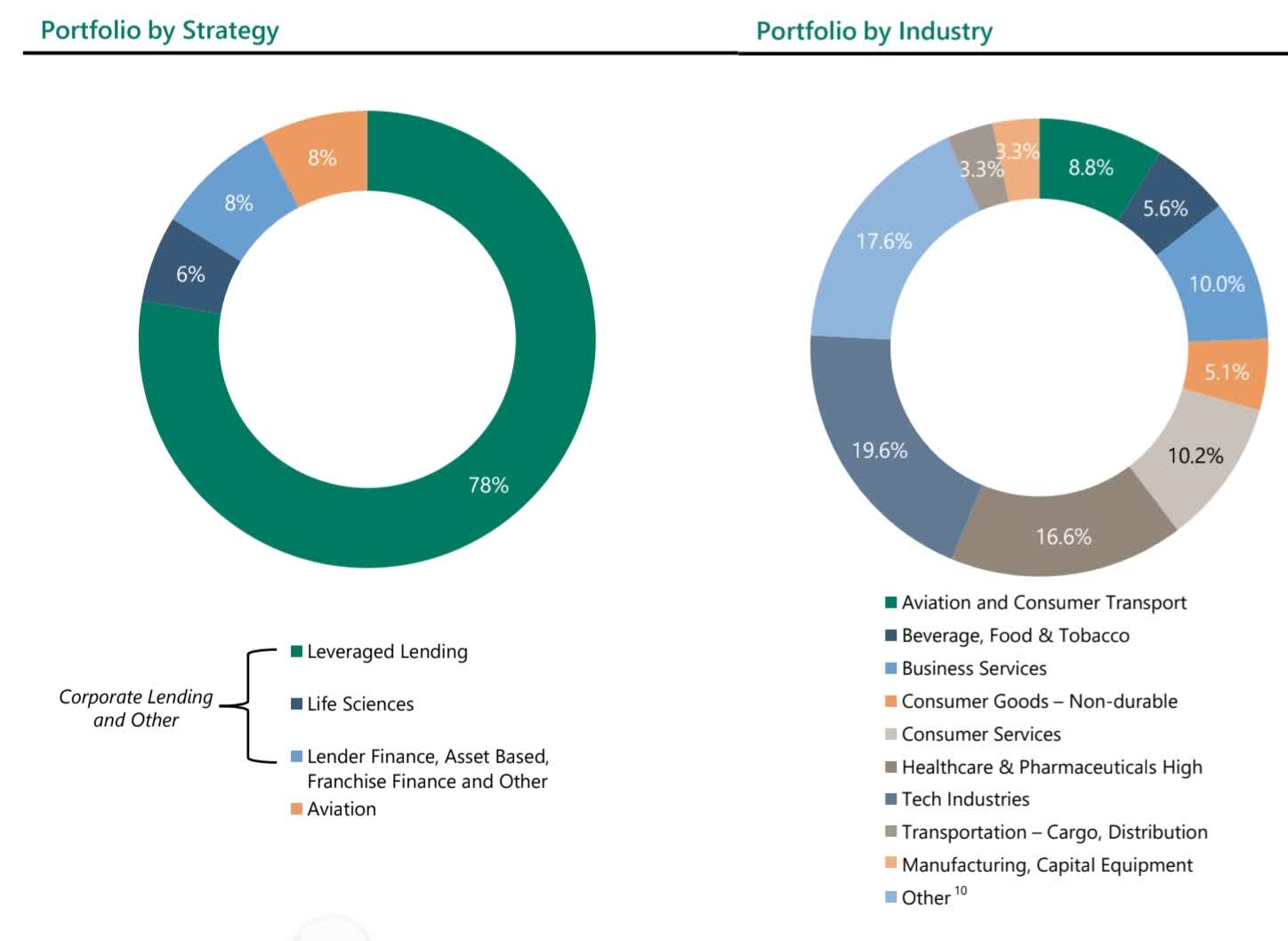

Since the merger has closed, I thought it would also be a good time to review the updated portfolio strategy. Leveraged lending still accounts for the largest earnings source for MFIC, accounting for 78% of their investment portfolio. The portfolio now includes exposure to life sciences, lender finance, and aviation investments. This portion of their portfolio consists of 100% floating rate debt and helps enable MFIC to capture higher levels of earnings while the federal funds rate sits at its decade high. As interest rates are elevated, so is the required debt maintenance that borrowers have to pay out on the capital borrowed from MFIC. The higher amount of interest income collected is one of the main drivers of the growth of net investment income.

Additionally, MFIC’s strategy still involves a high level of industry diversity across their investments. This helps mitigate any sort of concentration risk to one specific sector and can reduce overall price volatility. There are currently 165 individual portfolio companies within and the portfolio sits at a weighted average yield of 12% The heaviest weighted industry exposure remains to the tech sector, accounting for 19.6%. This is followed by allocation to the healthcare and consumer services sectors, making up 16.6% and 10.2% respectively. While maintaining a high level of diversity, I also like that the total portfolio has an average interest coverage ratio of 1.9x. This means that MFIC makes sure to only make investments with portfolio companies that have strong level of free cash flow and have the ability to navigate headwinds.

MFIC Q2 Presentation

97% of their portfolio is invested on a senior secured first lien basis, and this is reassuring because it helps reduce the chance that all invested capital is lost in a bad transaction. Senior secured debt sits at the top of the corporate capital structure. This means that the debt issued by MFIC has the highest priority for repayment above other forms of debt that a portfolio company may have. This is a form of protection is cases where a portfolio company is underperforming and may have to start liquidating assets in the case of a bankruptcy.

The most notable result of the merger is the huge increase in net assets under MFIC’s umbrella now. Total net assets now sit at $1.45B, representing an increase of 44% after the inclusion of the Apollo assets. This has also improved the level of liquidity and the capacity for management to allocate capital towards new deals that can contribute towards future earnings growth.

Financials

When it comes to the earnings potential of MFIC, we are yet to see how efficiently management will capitalize on the growth of assets and earnings potential following the merger. In the short term, I wanted to take a look at the most recent Q2 earnings that were reported at the beginning of August. Most importantly, net investment income landed at $0.45 per share, beating expectations by $0.05. Net investment income also grew by a very modest $0.01 over last year’s total of $0.44 per share. Total investment income landed at $0.69.1M, which was a slight increase of 0.8% year over year. Despite an increase in net investment income, the total net asset value dipped down to $15.38 per share from the prior quarter’s total of $15.42 per share.

While I don’t necessarily think this is anything to worry about, it is a sign of a weakening portfolio strength. The decrease in NAV can also be attributed to the $0.11 per share of net realized losses from underlying portfolio companies. This brought earnings per share – basic down to $0.35 per share. However, I believe that this is overshadowed by the increasing amount of new investments allocated to portfolio companies. The latest earnings revealed that $398.2M was allocated for investments into portfolio companies, representing a sizeable increase from the prior year’s total of $252.7M six months into the year. This represents investments into 18 new portfolio companies and 58 existing portfolio companies, and helps solidly the fact that management is focused on growing their portfolio of investments and earnings.

With anticipation around interest rate cuts, I think that investors are a bit antsy about how this will affect the value of BDCs. However, I believe that the recent merger completion and strong reinvestment into portfolio companies that MFIC is prioritizing will ultimately offset this. As interest rates start to fall, so would the level of net investment income received if their investments were made on a floating rate basis. MFIC stands out as a unique choice in the sector because even if short-term performance is effected, the BDC has the financial liquidity to offset any impact in earnings with additional growth from new borrowers.

For instance, total cash and equivalents currently sit at $67M. This gives MFIC a decent cash buffer that can be used when management identifies a strong investment opportunity. What could be improved, however, is the current long-term debt, which now sits at $1.51B. This has grown since the prior year’s total of $1.46B and sits near one of the highest levels it’s ever been over the last decade. However, future interest rate cuts can soften the expense of any of this debt issued on a floating rate basis, and any future portfolio growth could also help offset this amount.

Dividend & Valuation

As of the most recently declared quarterly dividend of $0.38 per share, the current dividend yield sits at 11.3%. The great news about this large double-digit yield is that it’s fully supported by earnings with a little extra cushion of safety. As previously mentioned, net investment income totaled $0.45 per share. This represents a healthy dividend coverage rate of 118.4, which means that NII fully covers the distribution and leaves a bit of a cushion that can be reallocated back into the portfolio and fuel more growth. This also creates a sense of greater stability because stronger coverage means that the distribution is less likely to get reduced if net investment income falls as a result of interest rate cuts.

Although, investors should be aware that MFIC has previously cut the distribution throughout its lifetime. The distribution was reduced in 2016 and once again in 2020 following the pandemic related market drop. While this doesn’t necessarily mean that management will cut the dividend again if earnings drop, it does show that MFIC isn’t afraid of reducing the dividend payout if they must. As a result, I believe there’s always a chance of the distribution being reduced if earnings are severely impacted by the drop in interest rates. For now, it seems to be safe, but if you think the current distribution coverage isn’t large enough for your liking, I may hold off on starting a position until after we see the effects of interest rate cuts.

When I previously covered MFIC, the price traded near fair value, as it didn’t sit near a significant premium or discount to its NAV. Instead, it traded at a very slight discount to NAV of about 0.5%. Since then, the price has fallen a bit as following the completion of the merger and a result of a new investment portfolio that has a lower credit quality. I believe this to be a solid opportunity for entry if you believe in the future success of MFIC as a result of the merger, since the price now trades at a discount to NAV of about 12.8%. Wall St. also seems to be a bit optimistic with the outlook here, as they current sport an average price target of $14.97 per share. This represents a sizeable upside of 9.6% from the current level.

CEF Data

I believe that this is totally reasonable when we consider that interest rate cuts may actually have a positive effect on earnings as well. Even if total net investment income is impacted in the short term, interest rate cuts would ultimately create a more attractive borrowing environment for companies that may be looking to take on some debt capital at more affordable rates. As a result, it’s entirely possible that we see an influx of borrowers hit the market and MFIC can use this as an opportunity to capitalize. As an influx of borrowers hit the market, MFIC will have a larger amount of new portfolio companies to choose from.

Risk Profile

When it comes to measuring the risk profile of a business development company, I like to take note of how the non-accrual rate changes throughout each quarter. Non-accruals represent the percentage of portfolio companies that are significantly underperforming expectations and are no longer capable of making the required payments on their debts. When I last covered MFIC, the non-accrual rate sat at 0.9% of cost and 0.6% of their portfolio at fair value. I thought this was very healthy and fell within a similar range of some of the more popular BDCs out there. However, the non-accrual rate has increased since the time of my last coverage and now sits at 1.8% of fair value and 2.3% at cost. However, here are some relevant non-accrual rates for peer BDCs:

- Barings BDC (BBDC): 0.3% non-accrual rate at fair value.

- Ares Capital (ARCC): 0.7 non-accrual rate at fair value.

- Runway Growth Finance (RWAY): 3.8% non-accrual rate at fair value.

- WhiteHorse Finance (WHF): 5.7% non-accrual rate at fair value.

Even though the non-accrual rate grew a bit, I don’t think there’s anything to necessarily worry about right now. The caveat is that this non-accrual rate is spread across eleven different portfolio companies, six of which were inherited from the close of the new merger. Therefore, the growth of the non-accrual rate isn’t necessary anything that should be a cause for concern at the moment. This is especially true since the non-accrual rate still sits under the 2% mark.

Takeaway

In conclusion, I maintain my buy rating on MFIC due to the growth possibility as a result of the merger with the Apollo funds. The distribution rate continues to be well-supported by the current level of net investment income. However, the distribution coverage rate could weaken as earnings are impacted by lower interest rates. I believe that the improved financials of the merger can offset any impact in earnings over the long term, but there may still be short-term impacts. Additionally, the price trades at an attractive discount to NAV. The non-accrual rate may have increased, but this is likely due to the new portfolio companies adopted as a result of the merger.