alberto clemares expósito/iStock via Getty Images

I have been following the Medical Properties Trust, Inc. (NYSE:MPW) saga over the past year, like many Seeking Alpha readers. I wrote my first article, a Hold rating effort in December here, on one of the leading hospital property owners in the U.S. and world. Then, it appeared to me that a number of variables were starting to move in the right direction, and I upgraded my MPW rating to Buy in March here at a price around $4 per share.

Seeking Alpha – Paul Franke, Medical Properties Article, March 8th, 2024

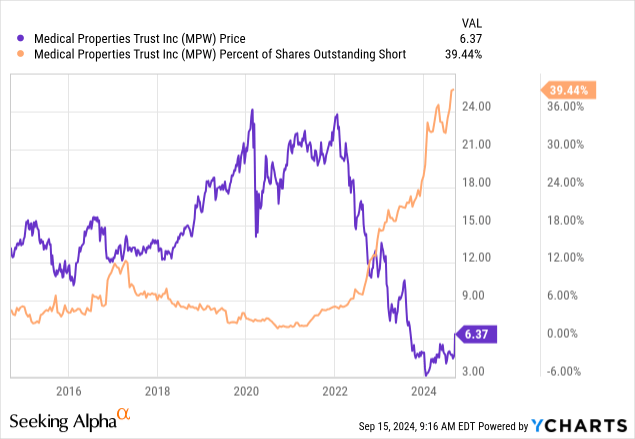

I personally have made several short-term trades on the bullish side of the equation for small gains. But, the real upside potential in the stock could now be playing out as an overzealous short interest position begins to cover en masse. Last week, the share price took off. All told, Medical Properties has gained +63% for a total return vs. the equivalent-period +10% S&P 500 index advance, since my initial optimistic report on this ownership security.

An extraordinary 39% of all outstanding shares have been borrowed and pre-sold into the marketplace by short sellers (10% is considered quite high on Wall Street) into August, depressing the stock’s quote and valuation. At the same time, the strong yielding MPW dividend payout has created significant real-world costs for remaining short (on top of high margin interest rates).

YCharts – Medical Properties, Share Price vs. Percent Outstanding Short, 10 Years

This combination of factors set the stage for a dramatic rally on any good news from management. Why? It’s core economic theory regarding the balance of supply and demand, rationed through price. What we saw last week was an earthquake of unusual buying both through the appearance of new investor purchase orders and existing shorts covering. That’s the share supply/demand imbalance story of September 2024, as management has made sizable strides this year dealing with its bankrupt Steward Health-related leases/debts and operating future.

According to the company’s September 11th press release,

Medical Properties Trust, Inc. today announced that it reached a global settlement agreement with Steward Health Care System (“Steward”), its secured lenders (“the Lenders”) and the Unsecured Creditors Committee (“UCC”) that restores MPT’s control over its real estate, severs its relationship with Steward and facilitates the immediate transition of operations to quality replacement operators at 15 hospitals around the country.

Honestly, it’s the type of positive fundamental news bears and shorts wrongly believed would be an impossible to achieve. So now what? Many short sellers have decided covering is the only logical way forward. Taking your lumps (trading losses) and moving on to the next idea sounds easy enough. The problem is few shares are available for sale each day on the unexpectedly bullish operating business announcement.

The end result is MPW’s share “price” must leap to find supply for transactions, allowing short covering to complete round-trip trades. That neatly explains what is going on in the stock the last couple of trading sessions. In essence, we’re witnessing something of a bull stampede overrun all selling supply.

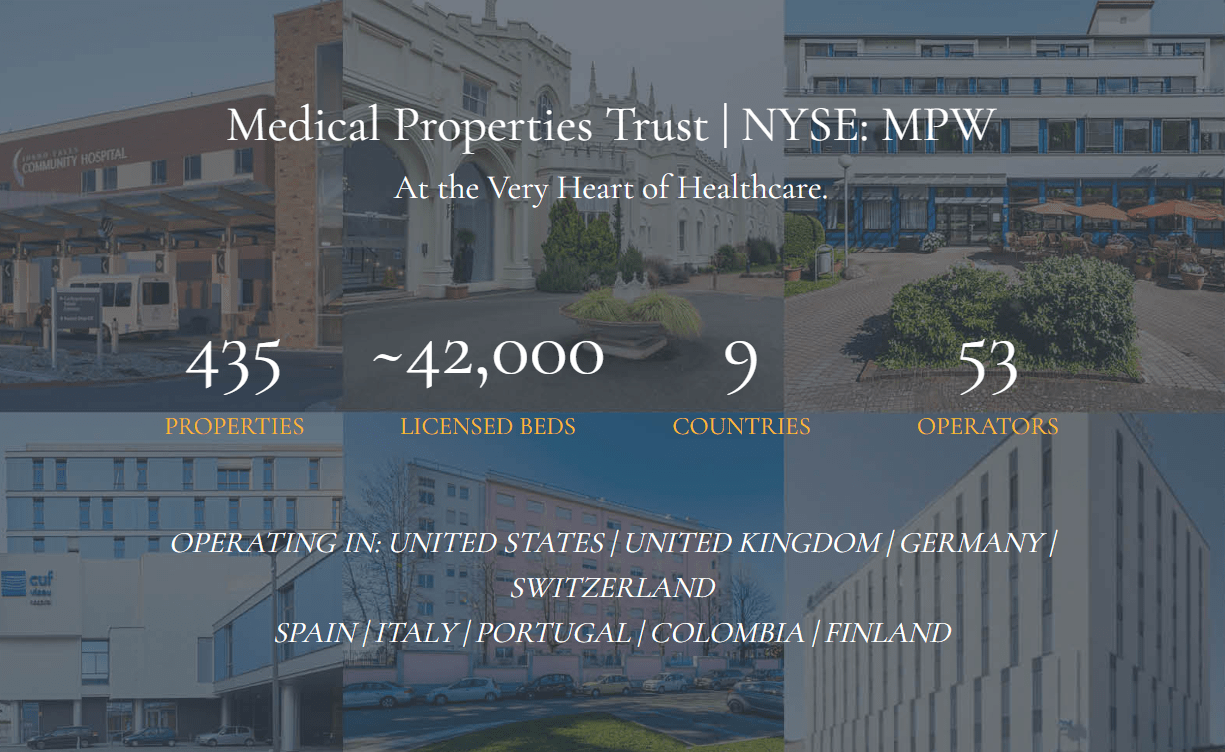

Medical Properties Trust Website – September 15th, 2024

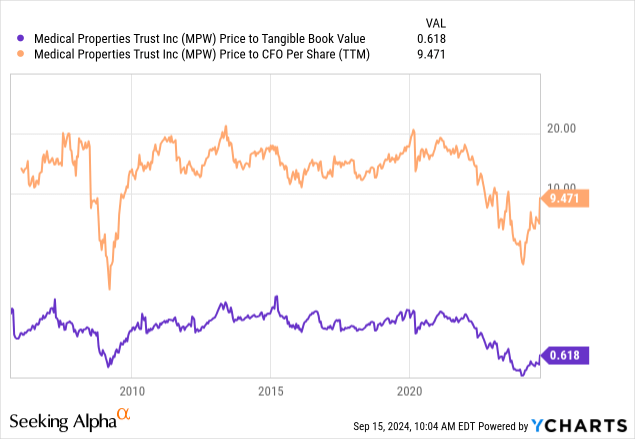

Valuation Still Quite Low

Believe it or not, the Medical Properties Trust 2024 valuation remains lower than any other period outside of the 2008-09 Great Recession and real estate bust, with only minor improvements vs. earlier in the year. Price to trailing cash flow of 9.5x and tangible book value of 0.62x still argue in favor of ownership.

YCharts – Medical Properties, Price to Tangible BV and Cash Flow, Since 2006

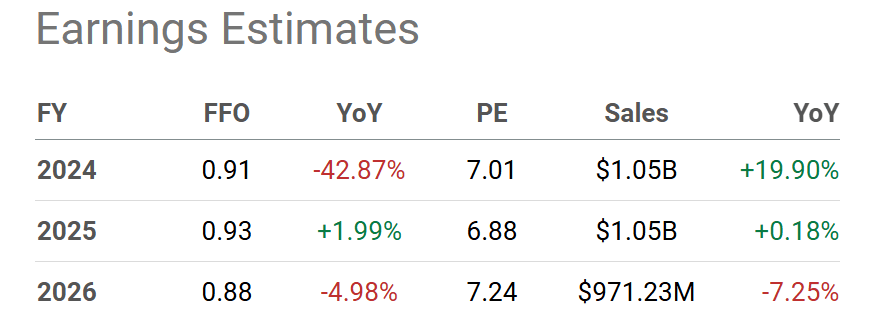

Analyst estimates are calling for basically flat results during 2024-26, with a price to FFO ratio of 7x. The good news is this ratio is better than the vast majority of REITs in the 12x to 16x range.

Seeking Alpha Table – Medical Properties, Analyst Estimates for 2024-26, Made September 13th, 2024

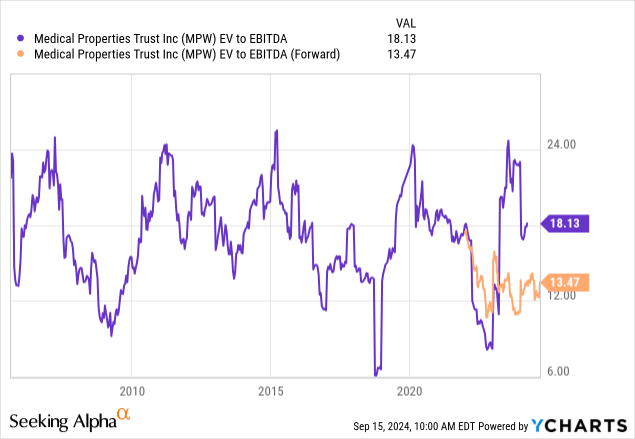

When we include debt and cash levels, the enterprise valuation appears equally cheap. After the problematic 2023-24 period is put in the rearview mirror, future EV to EBITDA is projected for land closer to 13x. This ratio remains a -30% discount to long-term averages, with lower readings outlined only about 10% of the time since 2006.

YCharts – Medical Properties, EV to EBITDA, Since 2006

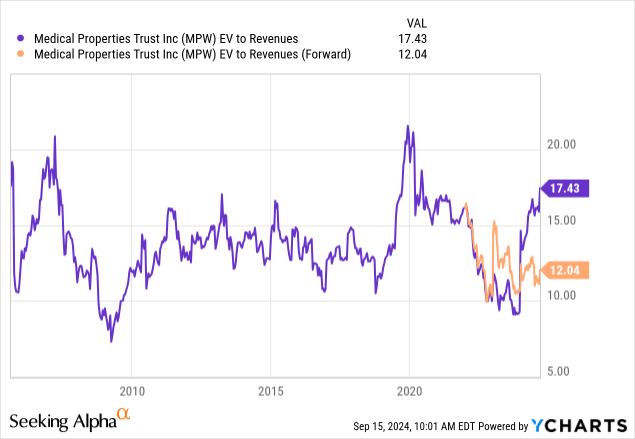

EV to sales provides a similar bargain argument. After the Steward Health debacle, forward estimated results are sitting at a solid -20% discount to long-term averages.

YCharts – Medical Properties, EV to Revenues, Since 2006

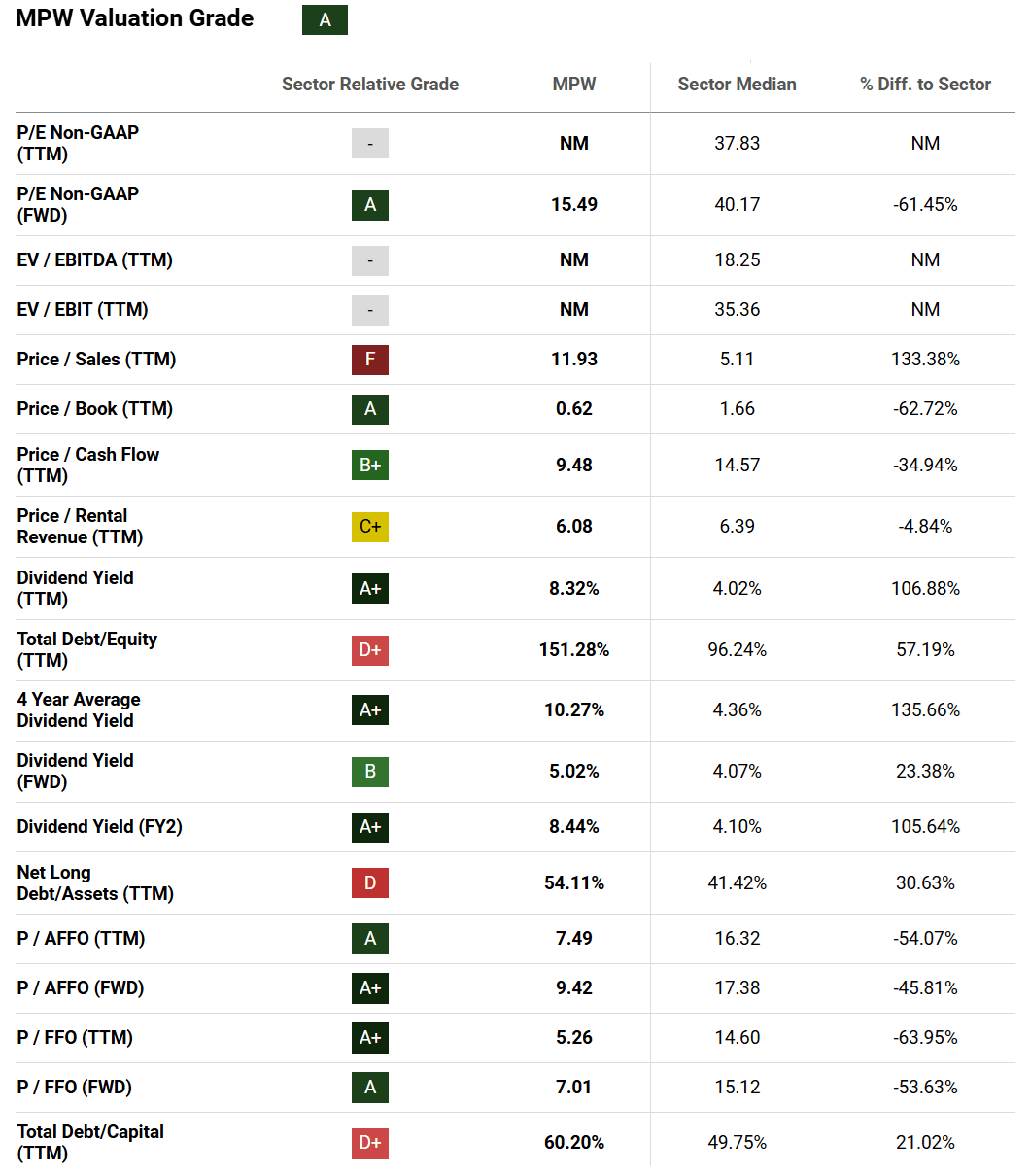

When measured against peer REITs, Medical Properties remains at a Quant Valuation Grade of “A” at $6.37 per share in the middle of September. Seeking Alpha’s computer-ranking formula still places MPW in the category of clear undervaluation.

Seeking Alpha Table – Medical Properties, Quant Valuation Grade, September 14th, 2024

Final Thoughts

I am coming up with a “fair value” range of $8 to $10 per share, based on the new dividend payout rate of $0.32 (5% forward yield currently), and a normalized financial ratio valuation. My conclusion is considerable upside potential exists, which could materialize in quick order, given an expanding short squeeze situation.

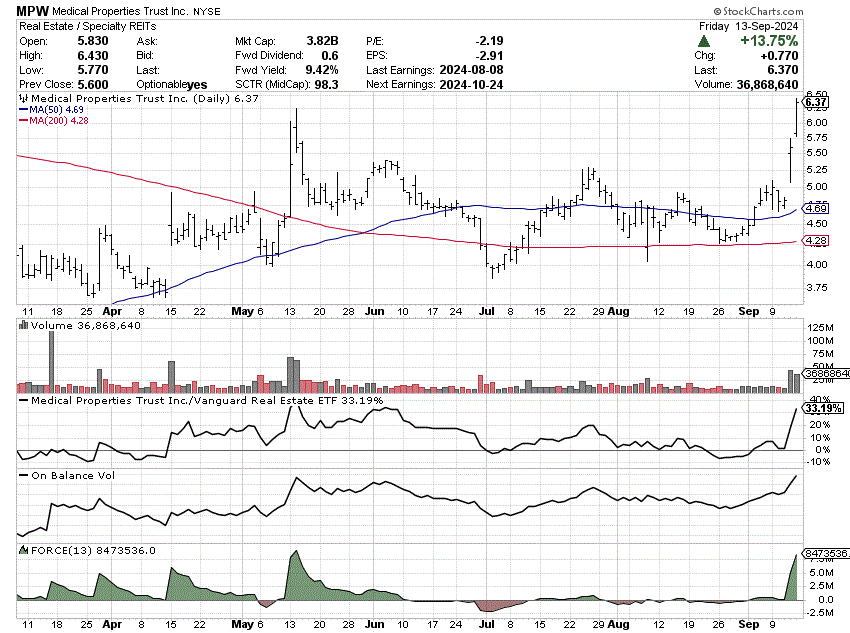

Since my initial bullish rating in early March, shares have witnessed bouts of high-volume short covering (as measured by the 13-day Force Index below). These episodes have helped put a floor under the price, with the 200-day moving average ready to turn higher in September.

In addition, On Balance Volume readings have been very constructive, and MPW has widely outperformed diversified REIT indexes/products like the Vanguard Real Estate ETF (VNQ).

StockCharts.com – Medical Properties, Daily Price & Volume Changes, Since March 8th, 2024

Are there other potential “short squeeze” ideas you should consider today, with a mirror investment setup to Medical Properties? I just wrote my bullish take on the enormous short position building in clothing retailer Kohl’s (KSS) here. Tremendous underlying value and a soft landing could be setting up this name for a particularly rosy outcome 6-12 months down the road for investors. Short covering provides the extra buying fuel for an oversized price advance.

What downside risk remains for Medical Properties Trust shareholders? With the Steward Health fiasco largely resolved, I would say the changing macroeconomic environment, regulations on hospitals, and the payout formulas from government agencies are places to watch for negative news events.

For sure, the direction of short interest changes is another key for pricing. If the shorts are reluctant to give up, MPW’s quote could be stuck in the $5 to $6 range for some time. Lastly, and perhaps holding the greatest odds for trouble, if the U.S. stock market crashes overall, Medical Properties will likewise be affected. So, investing in this name is not completely risk free.

I currently do not own shares but am looking to enter a stake on any material price weakness (possibly a function of a bear market dump on Wall Street). The bearish-betting short position no longer has the Steward Health argument or base valuation logic to support their view. As such, conventional wisdom by Wall Street analysts and shorts may have reached overly pessimistic levels on Medical Properties Trust’s stable to bright long-term future. A cyclical sentiment swing back toward optimism may be underway.

I continue to rate MPW shares a Buy, using a 12-month outlook as my yardstick.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.