ricochet64

On July 31, Johnson Controls (NYSE:JCI) reported its third-quarter results, with adjusted earnings per share (EPS) slightly surpassing expectations by $0.06, though revenues fell short by $140 million. While these results suggest that the company is largely meeting market expectations, recent strategic shifts, including the announcement of a new CEO and the divestiture of its residential and light commercial HVAC businesses, as well as its air distribution technologies segment, might raise concerns among investors. These changes could signal a need to reassess the risks and future prospects of the company.

Recent Financial Performance

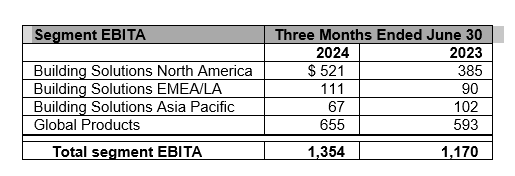

Johnson Controls’ third-quarter’s report revealed a 3% year-over-year increase in organic revenue, with service revenue surging by 9%, global product sales rising by 3%, and systems revenue increasing by 1%. The company also saw a significant improvement in operating profit, with segment (EBITA) expanding by 15.7%. However, this growth was largely driven by the Building Solutions North America segment, while the Asia Pacific region experienced a steep decline of over 34%. This sharp downturn highlights ongoing challenges in the business’s performance in Asia, particularly in the Chinese market.

Johnson Controls third Quarter Report 2024

As mentioned in their earnings call, JCI anticipates an increase in its exposure to the rapidly expanding data center market, projecting that this segment will account for nearly 10% of its sales in 2024, up from 7% in 2023. Additionally, management indicated an ongoing strong demand for its products, shown by a rise in new orders and a growing backlog.

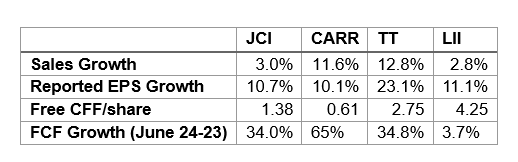

The quarterly report showed a drop in diluted (EPS) from $1.53 to $1.45. However, free cash flow increased remarkably by 34%. While sales growth appeared flat compared to industry peers, the company’s earnings and free cash flow growth were more competitive within the peer group for the same period.

Seeking Alpha

CEO and Strategic Changes

During the company’s earnings call, CEO George Oliver announced that he was stepping down and that Johnson Controls already started the search for a new CEO. Additionally, management provided updates on its recent divestitures, revealing that the net proceeds from these transactions are approximately $5billion and that they represent around 20% of the company’s current sales. According to Oliver, the goal behind these moves is to simplify the company’s business portfolio and to focus on the commercial building solutions business.

To estimate the financial impact of these changes, the following calculation provides some insights.

As mentioned in the earnings call, the company expects to net approximately $5 billion from the two transactions, with plans to use the proceeds for debt reduction and shares buyback. The management mentioned that debt reduction is important to keep favorable debt rating. My belief is that most of the proceeds will be used for shares repurchase because the divestitures will not have a significant impact on the company’s capital structure, as the cash proceeds from the transaction will be balanced by a decrease in long-term assets related to the sold divisions.

With a revenue estimate of $28.8 billion for 2025, the divestitures would result in a 20% drop in total revenue, bringing it down to $23.04 billion.

Assuming Johnson Controls can successfully enhance its 2023 net profit margin by 10% through its strategic focus on more profitable segments, their net profit margin would increase from 6.9% in 2023 to approximately 7.59% in 2025. With this improved margin, the estimated net income would be around $1.75 billion, based on projected sales of $23.04 billion.

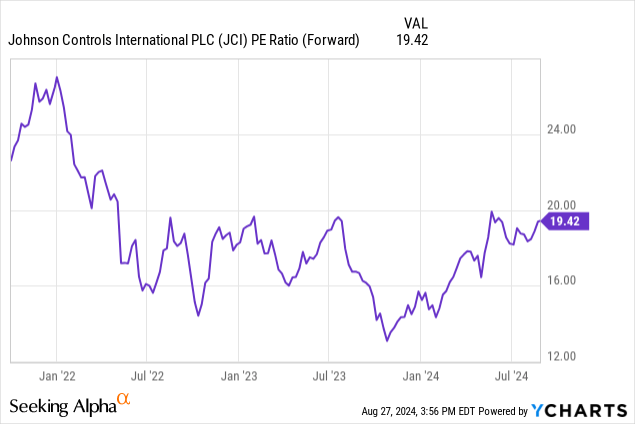

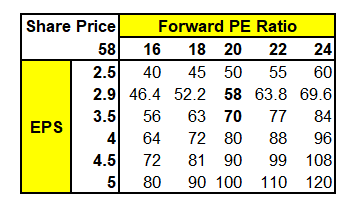

Assuming 10% of the sales proceeds are allocated to debt reduction and 90% to shares repurchases, the company would spend approximately $4.5 billion on buybacks. At an average share price of $70, this would result in the repurchase of about 64.29 million shares, reducing the total number of shares outstanding from 668.01 million to 603.72 million. This would bring (EPS) to approximately $2.90. This is a 29% decline from the current 2025 (EPS) estimate of $4.10. As shown in the chart below, JCI’s forward PE ratio has been hovering between 26 and 14. For an average forward PE ratio of 20 and $2.9 (EPS), the share price would be valued at $58.

As shown in the table below, to justify a $70 share price at 20 forward PE ratio, the (EPS) should be around $3.5.

Author

The above calculation highlights the potential impact of the company’s divestitures on its earnings and stock price. It is important to note that the actual outcome will depend on the company’s ability to effectively execute its strategy by offsetting the loss in earnings from the divested segments with additional earnings from the current and potential service segments. Successful implementation could mitigate short-term disruptions and ultimately lead to stronger long-term performance.

Risks

In my previous article, I highlighted the slowing economy as a potential risk to Johnson Controls’ financial performance. While this concern is still relevant, two new significant risks have emerged: the CEO transition and the strategic shift in the company’s business.

- CEO Transition: The change in leadership introduces uncertainty, as a new CEO may bring different expertise and priorities, potentially causing cultural disruption and impacting employee morale and talent retention.

- Strategic Shift: The divestitures, while aiming to simplify the business, will reduce revenue and earnings in the near future, potentially affecting the stock price. Additionally, the company’s new plan will increase its exposure to the commercial real estate sector, which has been challenging since the pandemic. Also, the exit from the light AC equipment business may weaken the brand’s recognition, as the presence in the residential market, though less profitable, helps maintain the company’s overall brand visibility and supports additional business opportunities.

Conclusion

Johnson Controls’ third quarter results, while largely meeting market expectations, come amidst significant strategic changes that could reshape the company’s future. The upcoming CEO transition and recent divestitures introduce new risks. While these moves could lead to short-term earnings dilution and potential stock price volatility, the long-term success will depend on the effective execution of these strategies. Given the new emerging risks, I downgrade the stock from Buy to Hold. I still believe the company has tremendous opportunities in the data center business as well as in the commercial building solutions business, however, as investor, I should carefully monitor the company’s ability to successfully execute the strategic changes and to capitalize on those changes to create new growth opportunities.