We Are

As a value investor, I prioritize the long term. Having said that, some opportunities achieve their fair value rather quickly. This is a blessing. And it’s something that I never get tired of seeing. One of the latest examples of this can be seen by looking at Independent Bank (NASDAQ:INDB), a rather small regional bank with a market capitalization of $2.69 billion. Back in May of this year, I wrote an article about the company that recognized some of the firm’s problems but in which I ultimately rated the company a ‘buy’. In my view at the time, the stock just barely warranted that rating.

I never would have guessed that shares would have skyrocketed higher in such a short window of time. Since that article was published, shares are up 24.4%. By comparison, the S&P 500 has risen by only 7.2%. Looking at the picture again, I do see that the company has exhibited some improvements in key areas. But based on how the stock is currently valued, I have a difficult time imagining that additional meaningful upside could still be on the table. Because of this, I’ve decided to downgrade it to a ‘hold’ for now.

A look at recent growth

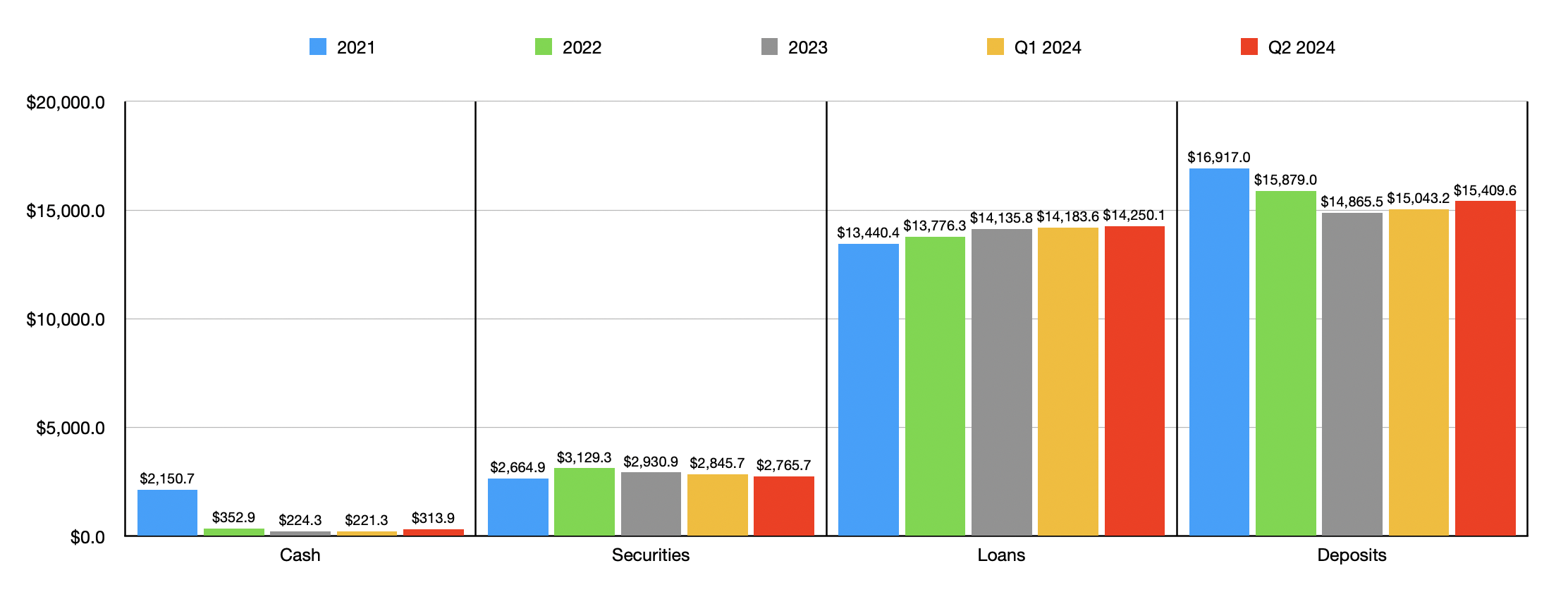

One of my biggest problems with Independent Bank when I wrote about it earlier this year was the fact that the company had experienced a decline in deposits. There was an increase from the end of 2023 to the end of the first quarter of this year. But that did not do enough to negate the fact that, from the end of 2021 through the end of 2023, deposits had fallen a whopping 12.1%. When you see a single increase from one quarter to the next in deposits, it’s unclear whether that’s part of a new trend. But now we have confirmation that, in this case, it was. That’s because, as of the second quarter of this year, deposits have now increased to $15.41 billion from the $15.04 billion that the company had at the end of the first quarter. Management attributed this increase to a couple of things, namely higher municipal deposit inflows and strong consumer demand for higher cost time deposits.

Author – SEC EDGAR Data

It is worth mentioning that, unfortunately, even more of the company’s deposits are now uninsured. When assessing a bank, I prefer that no more than 30% of all deposits are uninsured. I gave Independent Bank some slack in my original article about the company because its number had come in at 31.2%. But today, that number is a bit higher at 33.1%. This disparity alone is not enough for me to turn from bullish to neutral. But it certainly doesn’t help. The reason why I want this number no higher than 30% is because, the higher it is, the more susceptible the institution is to bank runs.

In my original article about the company, one thing that I applauded management for was consistent growth in the value of loans. To see this occur at a time when deposits are falling is difficult. At some point, one or the other has to break. But the good news is that, as of the end of the most recent quarter, we are seeing loans rise further. At the end of the first quarter, the value of loans on the company’s books totaled $14.18 billion. By the end of the second quarter, this number had risen to $14.25 billion.

Author – SEC EDGAR Data

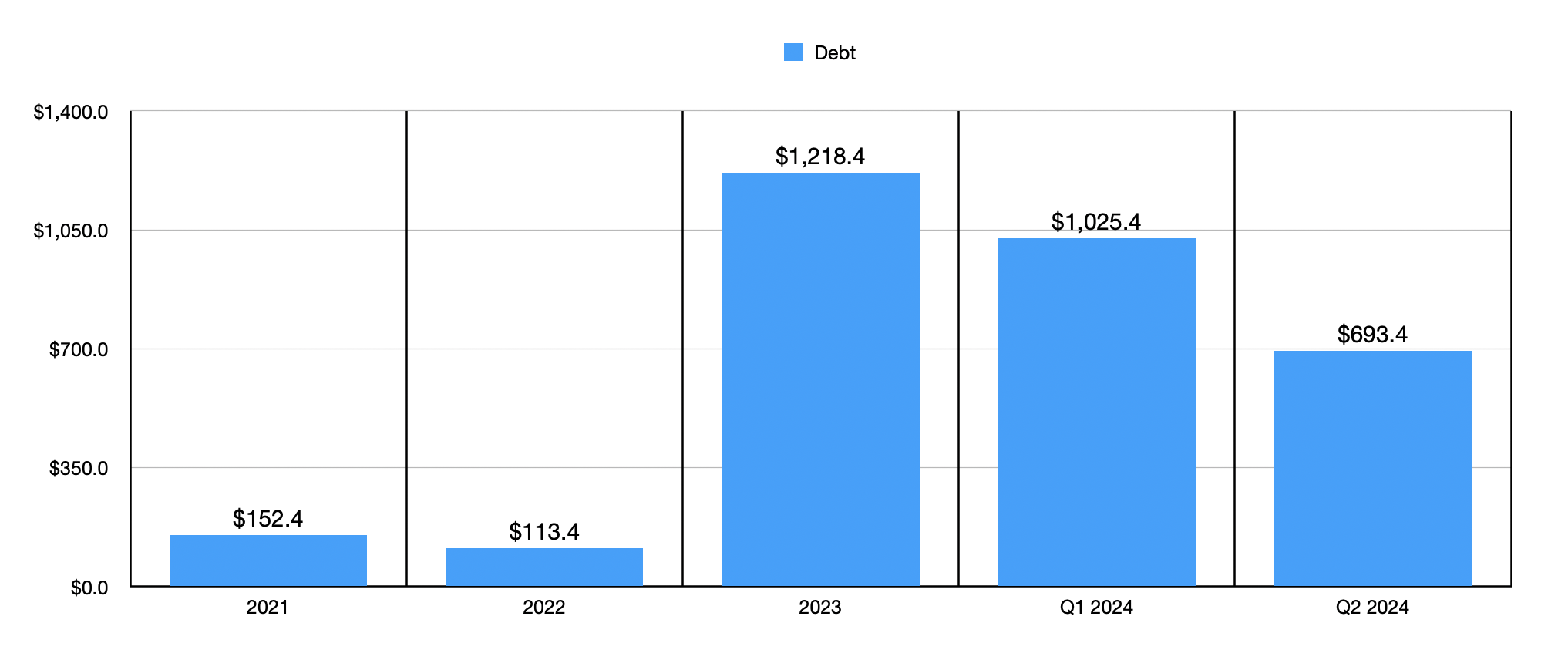

There are other aspects to the balance sheet that deserve attention. Securities would be one example. By the end of the most recent quarter, the company had $2.77 billion worth of securities. This was actually down from the $2.85 billion reported at the end of the first quarter. Since the end of 2022, the value of securities on the company’s books has been declining. So this is not terribly surprising to me. Cash and cash equivalents, meanwhile, increased from $221.3 million in the first quarter to $313.9 million in the second quarter. Other than the increase in deposits, the best thing that I saw involved a drop in debt. The company ended the first quarter of this year with $1.03 billion in debt. That number today is $693.4 million.

Author – SEC EDGAR Data

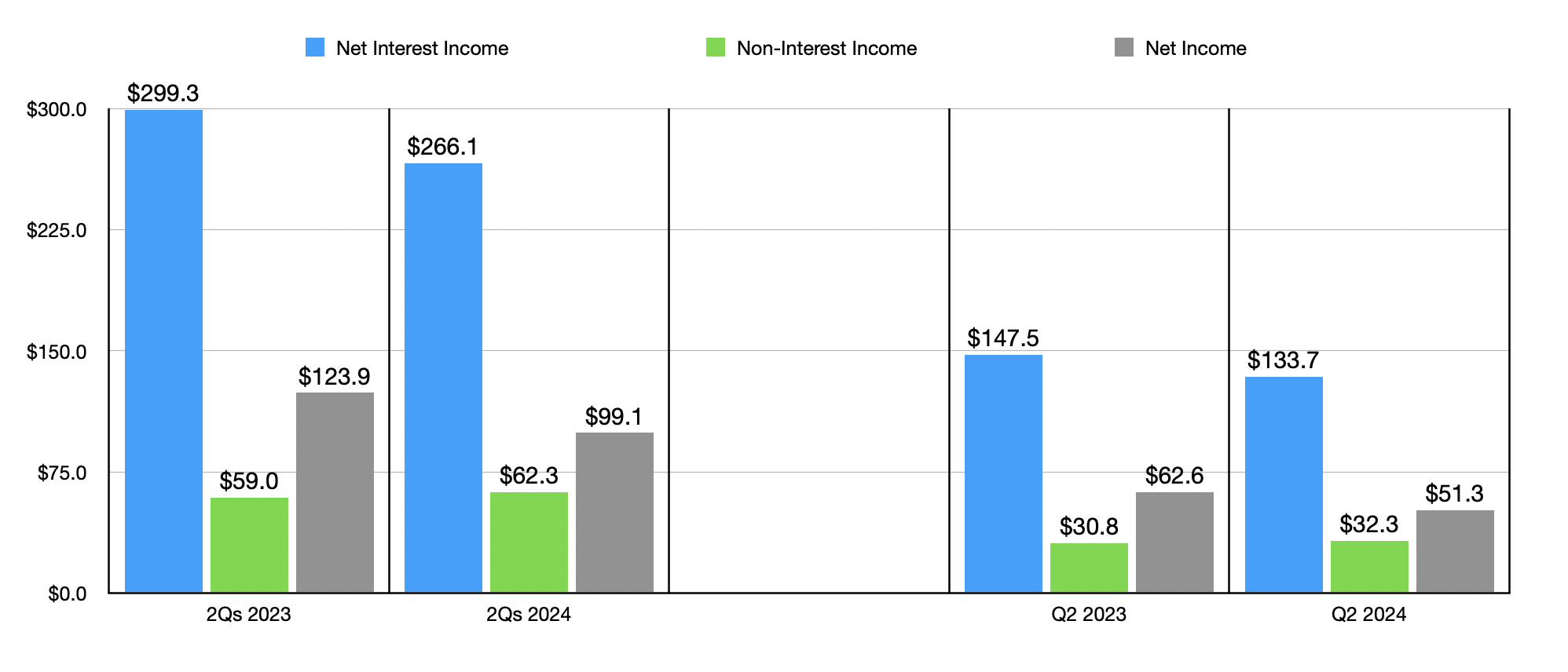

Moving on to the income statement, this is where we do see some continued pain. For the most recent quarter, the company had net interest income of $133.7 million. This is down from the $147.5 million reported one year earlier. A rather meaningful drop in its net interest margin from 3.54% to 3.25% can be considered responsible for this. This might not seem like much of a difference, but when applied to the interesting assets that the company had during the most recent quarter, that difference is an extra $49.9 million per year, or $12.5 million each quarter. This was instrumental in pushing net interest income down for the first half of this year compared to the same time last year from $299.3 million to $266.1 million.

There was a slight improvement in the most recent quarter when it came to non-interest income. This metric expanded from $30.8 million to $32.3 million. Based on the data provided, this was driven mostly by a rise in deposit account fees from $5.5 million to $6.3 million, and by an increase in mortgage banking income from $0.7 million to $1.3 million. Unfortunately, this was not enough to prevent total net profits for the institution from falling from $62.6 million last year to $51.3 million this year. And for the first half of this year, the $99.1 million in profits that the company generated ended up representing a rather meaningful decline from the $123.9 million the company reported for the first half of 2023.

Author – SEC EDGAR Data

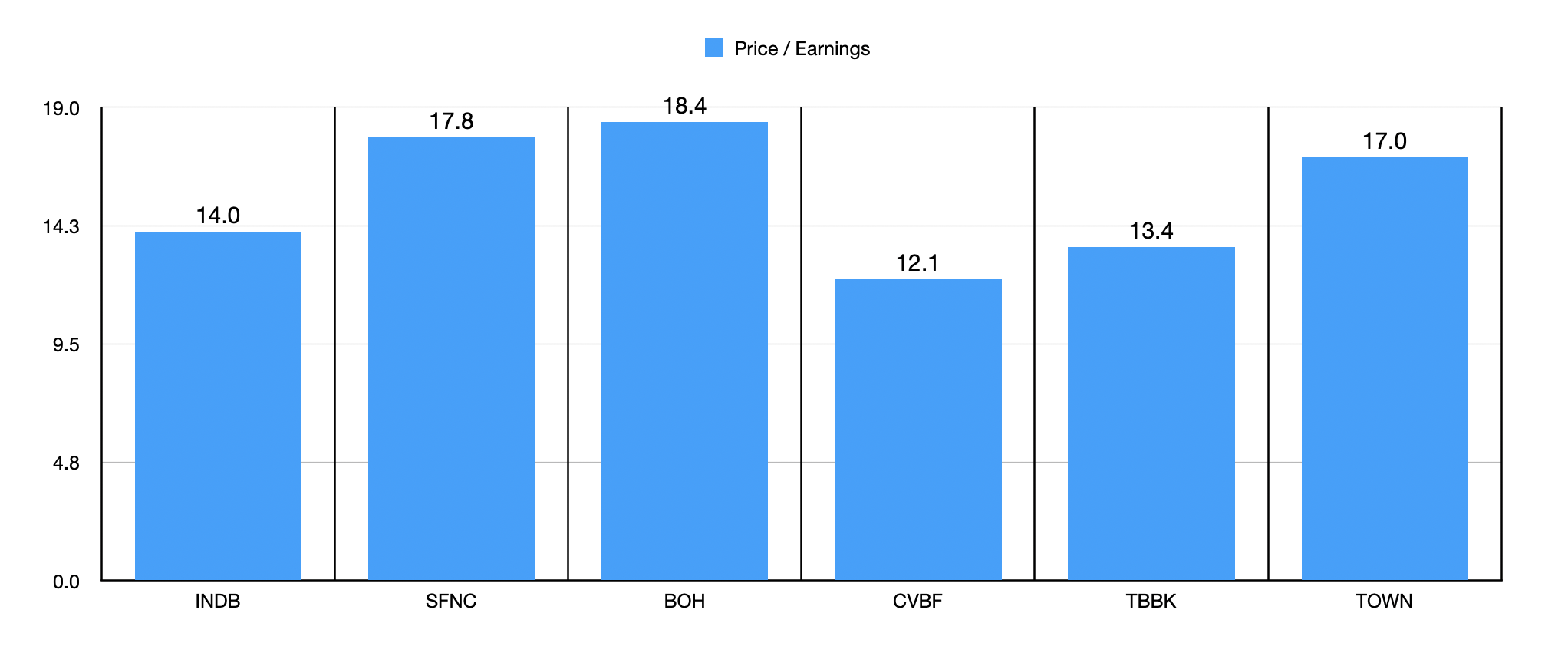

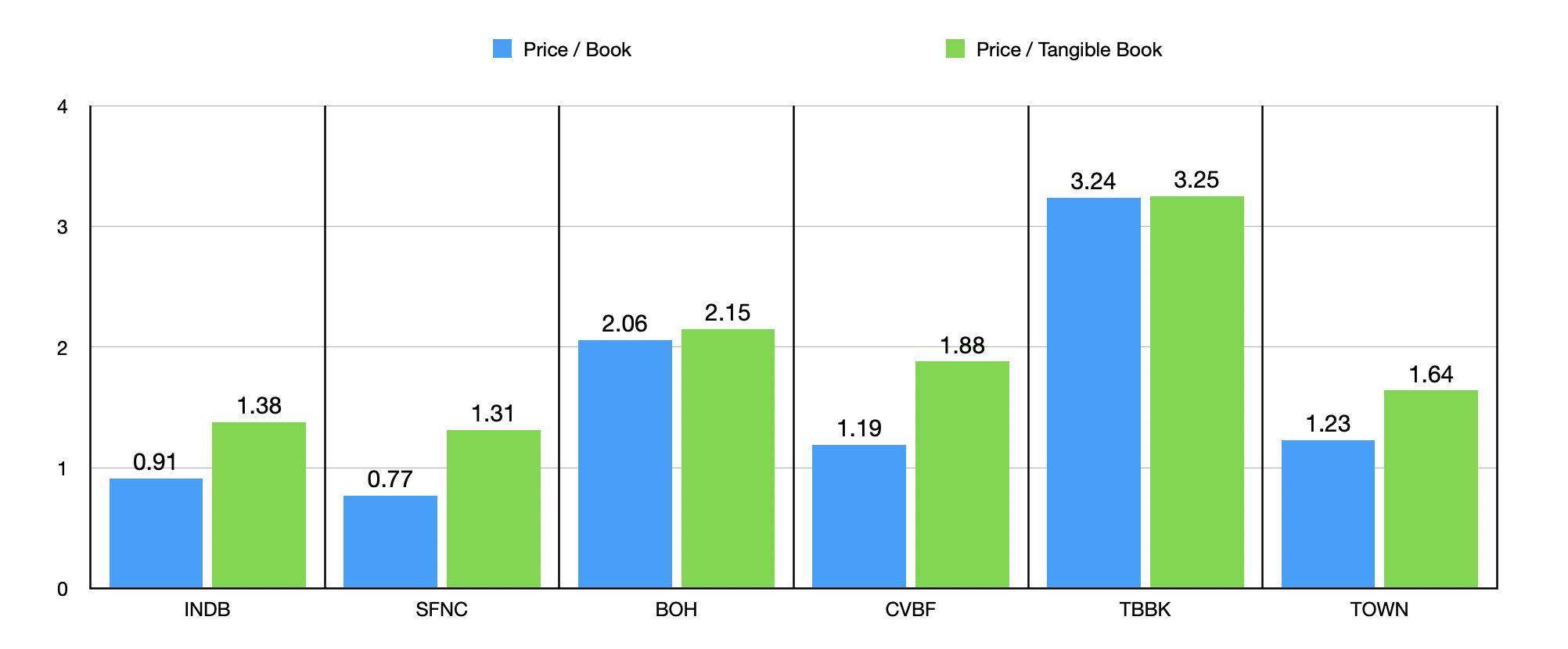

If we annualize the results the company experienced for the first half of this year, we would anticipate net profits for 2024 of $191.6 million. This translates to a price to earnings multiple of 14. But even if we were to use last year’s results, the price to earnings multiple would be 11.2. This is still above the 6 to 10 range that I typically prefer in this space. In the chart above, you can see that, using the forward estimates, two of the five companies that I stacked Independent Bank up against our trading at multiples lower than what it is. This indicates that it’s near the middle of the pack on this basis. Another way to value company is using the price to book approach and the price to tangible book approach. As the chart below illustrates, in both instances, Independent Bank is cheaper than all but one of the five firms I compared it to.

Author – SEC EDGAR Data

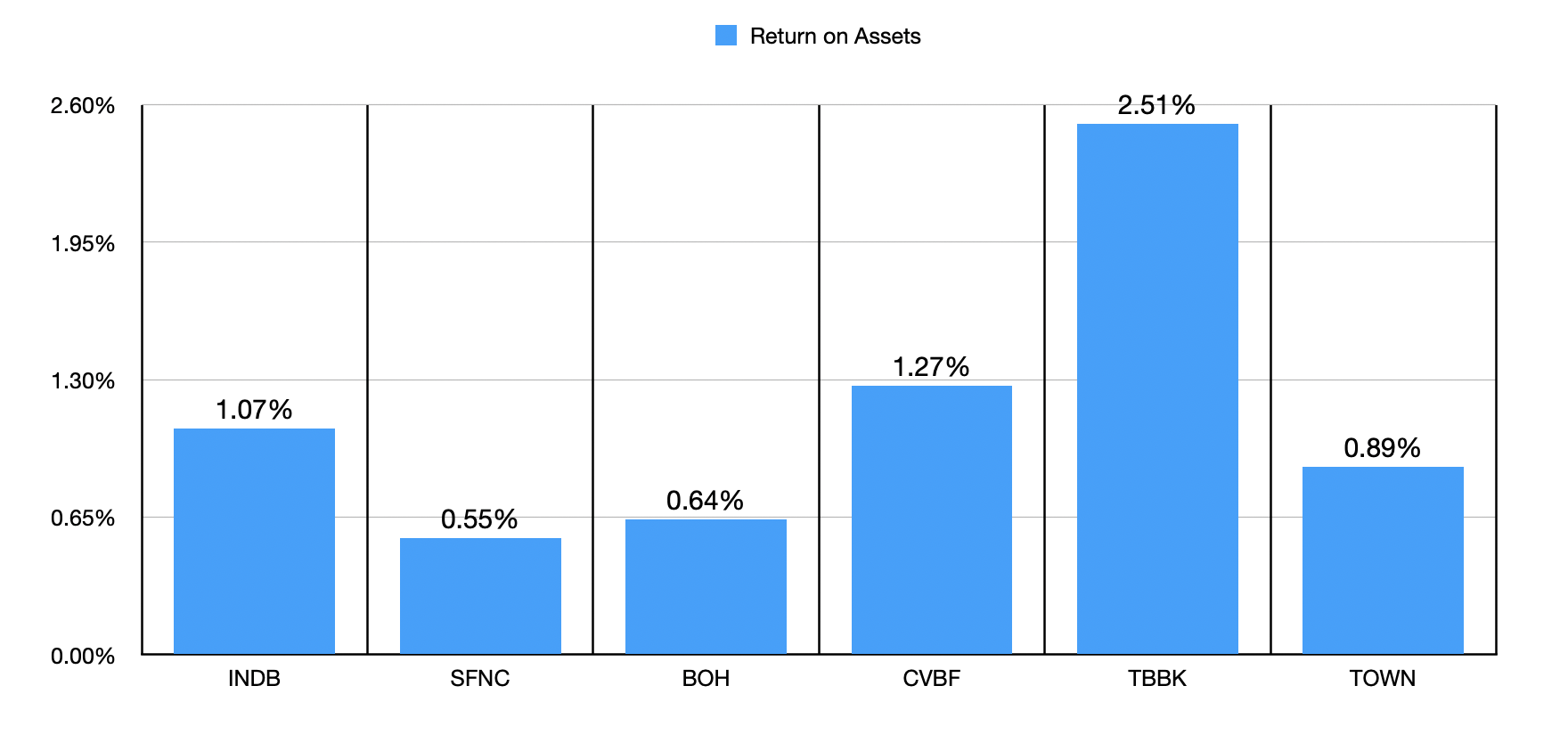

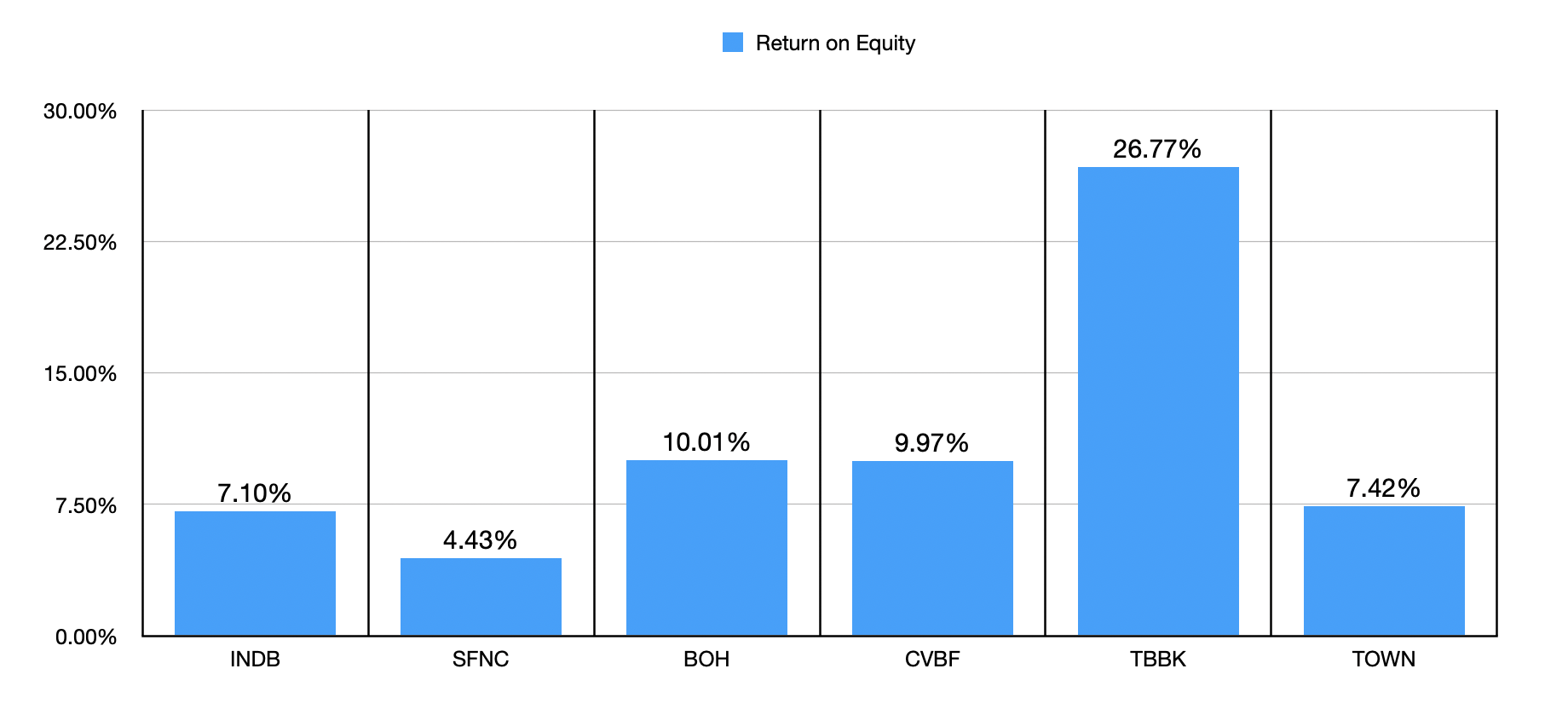

Relatively speaking, Independent Bank does appear to be fairly attractively priced. But on an absolute basis, I’m not sold. In the event that asset quality is high, I think that could bridge the gap. But unfortunately, this doesn’t appear to be the case either. In the first chart below, you can see the return on assets for our candidate, for five similar enterprises. Three of the five have return on assets lower than what it does. So once again, we are around the center of the pack. But in the subsequent chart, we can see that the picture is even worse when it comes to return on equity. Four of the five comparable businesses have return on equity ratings higher than what Independent Bank does.

Author – SEC EDGAR Data

Author – SEC EDGAR Data

Takeaway

All things considered, it has been quite a great run for Independent Bank. The company has fared far better than I expected it to, especially considering the short window of time we’re talking about. But alas, I think that the evaluation of the company no longer justifies a ‘buy’ rating. So because of that, I’ve decided to downgrade it to a ‘hold’.