hapabapa

Introduction & investment thesis

I last wrote about HubSpot (NYSE:HUBS) in July after the stock price declined more than 30% from the canceled Google (GOOG) acquisition. Prior to that, I had a “sell” rating on the stock, where I believed that its revenue growth rate was not encouraging enough for its nosebleed valuation at the time. When the stock finally declined after Google walked away from the deal, I upgraded the stock to a “hold.” The reason I did not upgrade it to a “buy” was because I assessed its valuation to be at fair value and believed that the selling pressure would likely continue from weaker demand, increased deal scrutiny, and ASP (Average Selling Price) headwinds from its pricing updates.

HubSpot reported its Q2 FY24 earnings in August, where revenue and non-GAAP operating income grew 20% and 42% YoY, respectively, beating estimates. However, its ASPs continued to decline, where the positive impact from an increasing number of enterprise customers adopting multiple hubs is being offset by a higher volume of lower ASP starter customers with their new pricing model in place. Although the management is optimistic about its pricing strategy over the long term, its guidance on customer expansion rate is mixed for FY24.

Assessing both the good and the bad, I have decided to continue remaining on the sidelines while maintaining my “hold” rating on the stock. The company is due to present its Investor Day on September 18, where I believe it will be key to assess management commentary on how they plan to navigate growth across its customer segments while driving its AI-driven product innovation roadmap with higher attach rates.

ASPs continue to decline while NRR is telling a mixed story.

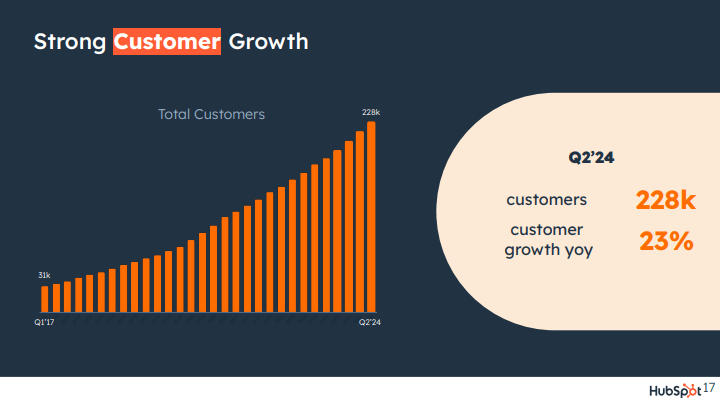

The company reported its Q2 FY24 earnings in August, where revenue grew 20% YoY to $637.2M, beating estimates, while non-GAAP operating income grew over 42% to $109.3M, with a margin expansion of 270 basis points to 17.2%. While customer count grew 23% YoY to 228,054, ASP continued to remain under pressure, declining 2% YoY to $11,215.

Q2 FY24 Earnings Slides: Trend of total customer count

This is related to its pricing changes that were introduced in early March, where they rolled out a seat-based pricing model to all subscription tiers by introducing Core Seat and View-Only Seat, allowing customers more flexibility and greater control over their total cost of ownership. While the management expected this to lead to lower initial ASP, the underlying strategy was to drive a higher volume of customers, which would eventually lead to more upgrades and expansion over time.

Yet, when we look at expansion rates, there is a discrepancy in the story. On one hand, while the management discussed that they are seeing a multi-point increase in net revenue retention at month three from customers that are on the new pricing model, they also admitted to seeing a challenge in their overall upgrade motion, thus holding their expectation for the net revenue retention rate to remain at 102 for the remainder of the year.

Striking the balance between small and up-market customers in a tough macroeconomic environment

I believe that the above phenomenon could be explained by the difference in performance between their customer segments. On one hand, the company is focused on fueling volume at the low end of the market through its product and pricing improvements, leading to strength in free sign-ups. On the other hand, it is the upmarket segment that is doing a greater part of the heavy lifting in ASP with multi-hub adoption with popular combinations of Marketing, Sales, Service and Content Hubs leading to larger wins in Q2, amidst continued vendor consolidation trends. Meanwhile, the management continued to reiterate that they are seeing slower decision-making and higher deal scrutiny on the macroeconomic front before companies are ready to spend, thus making it imperative for HubSpot to continue to differentiate itself with its product innovation roadmap.

AI-powered product innovation roadmap with growing product attach rates

HubSpot is set to present its Investor Day on September 18, and investors will be looking for commentary on how the management plans to navigate between their two customer segments with their product innovation roadmap that would lead to higher expansion rates in the coming quarters.

On the product innovation front, the company introduced major updates to their Service Hub in their Spring Spotlight, allowing customer support and customer success teams to be unified on a unified platform, leading to the number of wins with 100+ service seats growing 55% YoY. When it comes to their Content Hub, the management noted that the attach rate for Content to Marketing Hub has tripled since the launch in April, driven by innovative AI features like content remix, AI blogs, and more. As customers bring more data together within HubSpot, it has made a choice to embed AI in all of their hubs and within Smart CRM, enabling customers to create personalization at scale and increasing their new prospect engagement by 25% with higher conversion rates and selling prices.

Revisiting valuation: Not a “buy” yet.

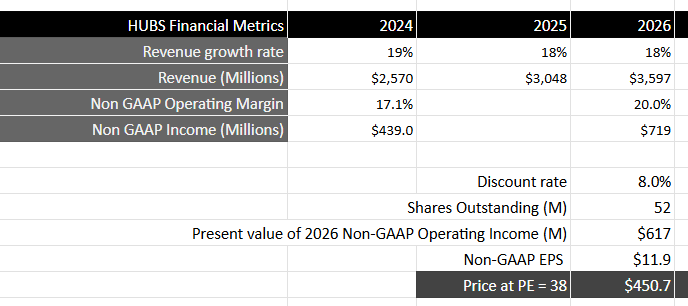

Looking forward, the management kept its long term financial framework anchored, while raising its revenue guidance slightly to approximately $2.57B in FY24. Assuming that HubSpot can continue to grow its revenues in the high teens over the next 2 years, as it sees the maturing of its seat-based pricing model to drive ASP and expansion in its customer base, it should generate close to $3.6B by FY26.

From a profitability standpoint, the management raised its guidance for non-GAAP operating income to approximately $439M, which represents a margin of 17.1%. Given its FY26 target of 20% non-GAAP operating margin, it should generate close to $719M in non-GAAP operating income, which is equivalent to a present value of $617M when discounted at 8%.

Taking the S&P 500 as a proxy, where its companies grow their earnings on average by 8% over a 10-year period, with a price-to-earnings ratio of 15-18, I believe that HubSpot should trade at approximately 2.25-2.5x the multiple given the growth rate of its earnings during this period of time. This will translate to a PE ratio of 38, or a price target of $450, which represents a downside of 8% from its current levels.

Author’s Valuation Model

My final verdict and conclusions

There isn’t sufficient evidence yet for me to upgrade my rating on the stock yet. While the management is driving a higher volume for its lower ASP customers along with positive commentary on the expansion rate they are seeing with customers that are on the new pricing model, I am slightly concerned with the overall trend and guidance for net revenue retention rate. Although I believe that HubSpot should benefit from vendor consolidation trends in its upmarket segment along with an AI-powered product innovation roadmap that drives higher product attach rates, it will be important to understand how the management navigates overall growth with its higher volume and lower ASP customers.

Given where the stock is currently trading, I don’t believe it provides an attractive entry point, given its risk-reward, and as a result, I will maintain my “hold” rating with a price target of $450.