LewisTsePuiLung/iStock Editorial via Getty Images

I rate Hermès (OTCPK:HESAY)(OTCPK:HESAF) as a buy, as the French company has a long history of delivering long-term value thanks to the company’s very strong position in the luxury global market. In my particular view, it’s the best company in the sector in terms of pricing power due to the excellent execution of its strategy of exclusivity, which is unmatched in the sector. I think that Hermès is an excellent alternative for any investor who is looking for buying an excellent company to buy and hold for many years, as Hermès is able to raise prices of its different products, particularly those related to its famous bags, deliver double-digit revenue growth while generating a consistent growth of its free cash flows without using much debt. I think that most reports about the company do not explore deeply what is the source of Hermès’ excellent performance over the years; this is a very important factor when we are considering buying a stock for our portfolio to hold for the next few years since we know that the stock markets might face significant volatility over the years, so it’s very important to be invested in stocks that gave us a lot of conviction to buy more when the stock markets offer us those opportunities.

Context

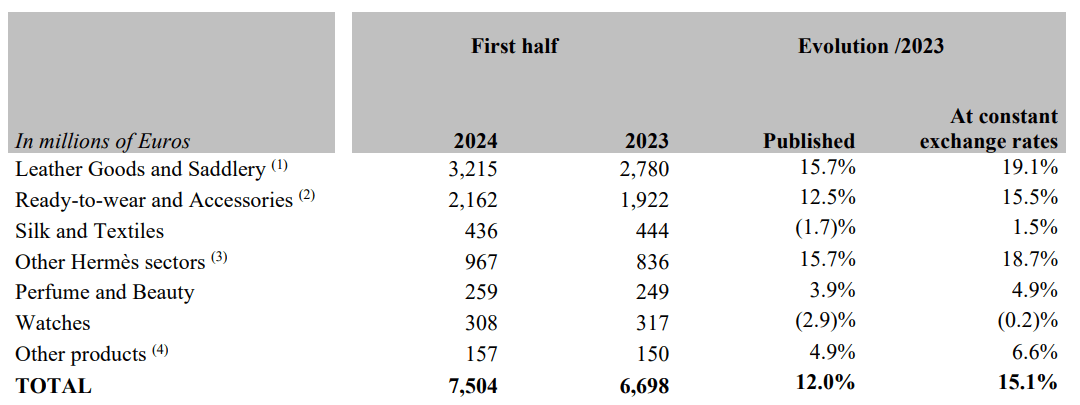

Hermès experienced a revenue growth of 15.1% in the first half of 2024 YoY at constant exchange rates. In the same period, the net income grew 6.4% YoY and free cash flow grew 3.6% YoY. In a context of high interest rates, I would say that these are very decent results. Looking at the revenue breakdown by type of product, we can see the following:

Hermes Financial Report

Leather goods and saddlery grew 19.1% YoY in the period, which actually represents more than 40% of the total revenues. I like to see that the most important business segment is the one with the best performance, growing 19.1% YoY at constant exchange rates. Other segments to highlight in the first half of 2024 are ready-to-wear and other Hermès sectors, which include jewelry and home products.

Hermes Financial Report

Competitive advantages: the brand and its exclusivity

In my view, it’s very important to understand the competitive advantages of a company in order to anticipate how it might perform in the next few years; in this sense, it’s important to identify if Hermès has something special since there are other companies in the luxury sector.

Since the company was founded by the harness-maker Thierry Hermès in 1837, when the company already produced high-quality harnesses combined with refined delicacy. Next generations kept expanding the type of Hermès’ products over the decades, from ties, mufflers, and scarves to its most famous handbags—Birkin and Kelly.

CEO Axel Dumas, who is a sixth-generation member of the family, has solidified the company’s strategy in the last years to keep the heritage and exclusivity that give it a rock-solid competitive advantage. Hermès is a largely family-controlled company now, in which the Puech, Dumas, and Guerrands controlled a 70% stake.

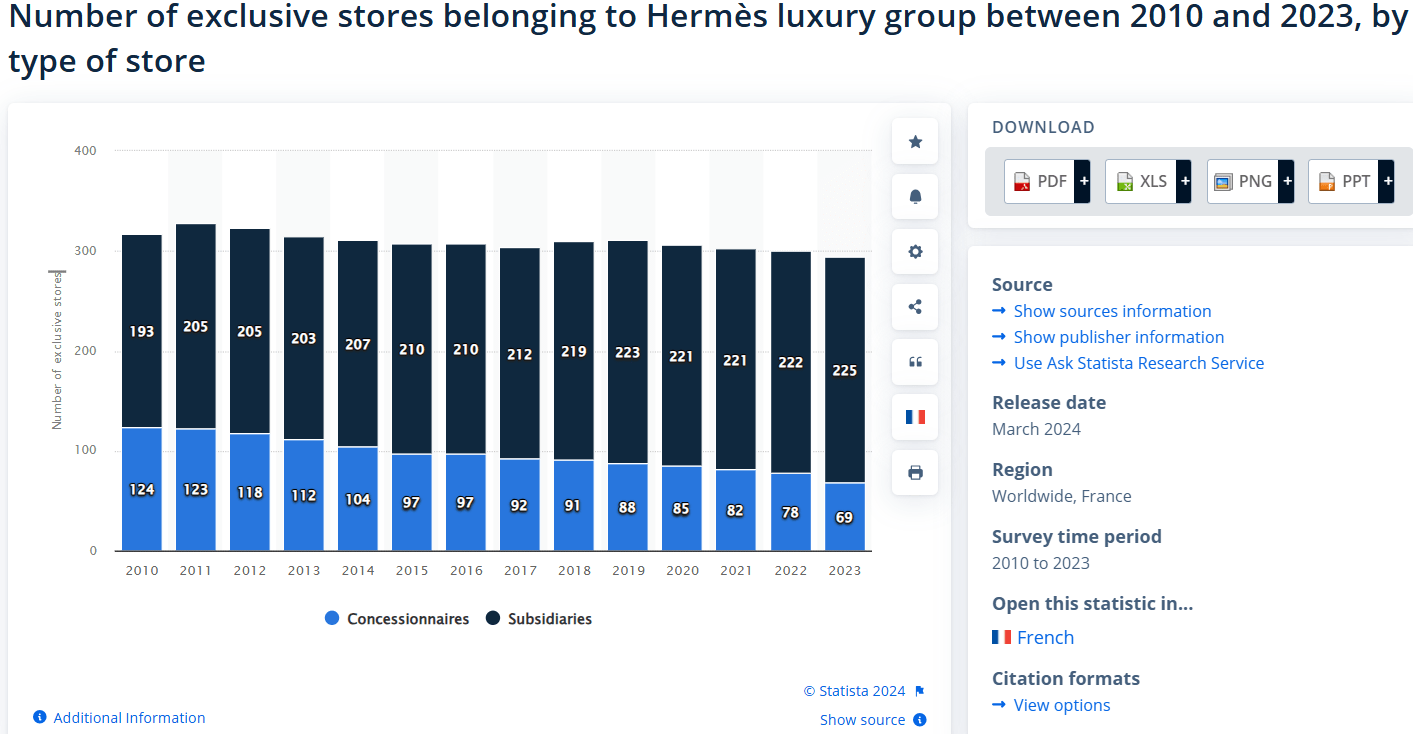

Statista

I was surprised to learn that Hermès is not growing its number of stores worldwide over the years, as we can see in the chart above; as such, a significant portion of the revenue growth is related to the company’s pricing power as the volumes are not increasing significantly. Also, in the same chart, we can see that the proportion of the concessionaires is being reduced consistently, which is a smart strategy since Hermès has way better control in their own stores of the customer’s experience while reinforcing the exclusivity and, as a result, its pricing power.

I should point out that the expansion of concessionaires was a past wrong strategy of the company, which was impacting negatively in the exclusiveness of its products. Fortunately, the management refocused his strategy to own more stores entirely controlled by the company. Therefore, I would expect that this trend of a lower number of concessionaries will continue, which will be reflected through high margins in the next few years.

Statista

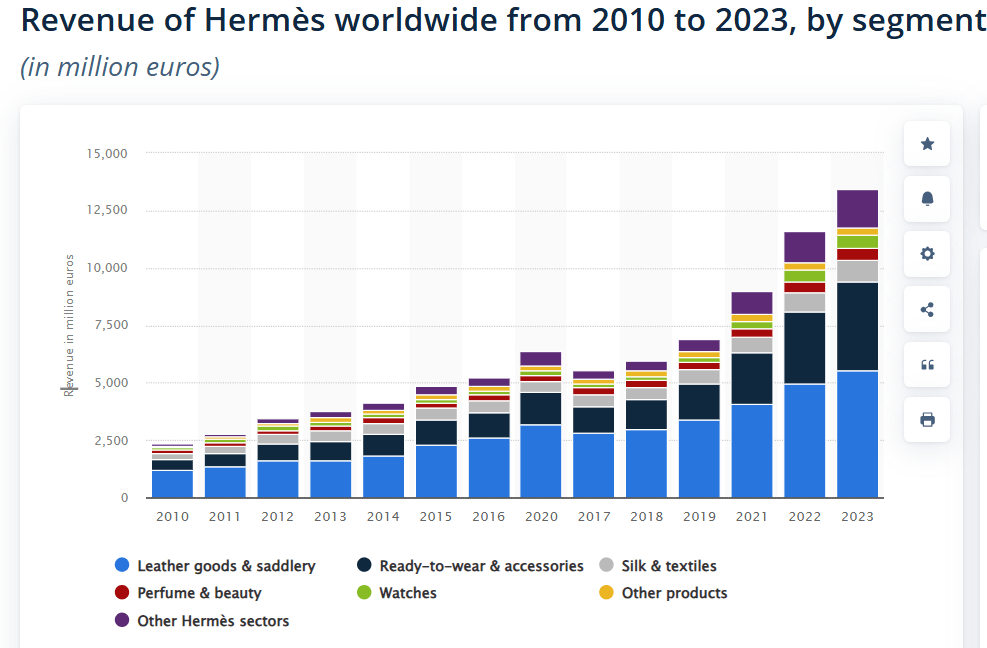

It’s interesting to see in the chart above that despite the company not increasing its number of stores, the revenues have been growing consistently, 12.7% CAGR from 2010, which means that the strategy of reducing the proportion of concessionaires while increasing its own subsidiaries is working in the long haul. Also, I like to see how the leather goods and saddlery were growing consistently, as it represents more than 40% of the total revenues, but there are other business segments that are growing healthy, such as ready-to-wear and accessories.

Statista

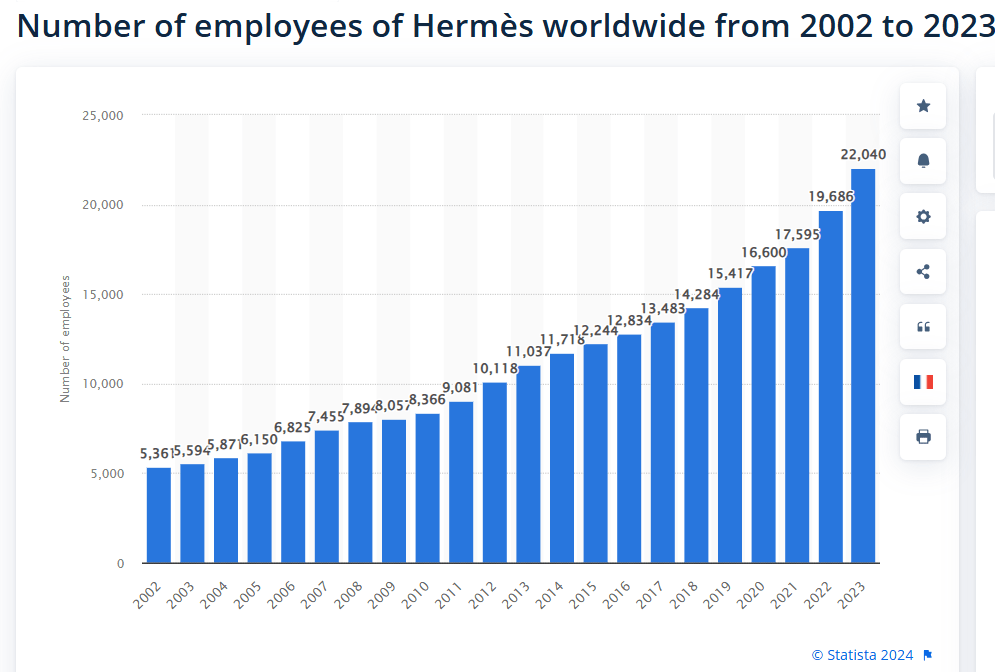

Another interesting point about Hermès is that the number of employees is increasing over the years, which reflects an increase in capacity; however, this combined with a restricted number of stores seems contradictory. However, Hermès is expanding its type of products over the years, which requires more specialized artisans to produce different products. It takes two years to become a craftsman at Hermès.

The retail stores are built and designed to show its exclusive image, focusing on creating a luxurious and memorable shopping experience for customers. The main goal is not to expand its production massively, as you’ve seen in the charts above, but to offer unique products in terms of quality and design at higher prices.

This is the kind of competitive advantage that I like to see in a company, but it’s rare; those companies whose moats are based on the brand are relatively few in number. I’ve written several articles about Apple, which has a similar moat to Hermès, but I’ve written an article about Apple (AAPL) in 2023 where I explained why the moat associated with the brand is the most powerful that you can find.

Birkin and Kelly handbags: symbols of status and engines for other Hermes’s products

As part of the leather goods and saddlery business segment, the famous handbags Birkin and Kelly have received the names of both celebrities. These handbags are works of art since there are some factors that make them special. Each of these bags is made by artisans, more specifically, “one craftman, one bag,” so these handbags are made by one artisan from start to finish, taking 40 hours to finish each.

Now, customers can not directly ask for these handbags in any Hermès store as that customer needs to wait for a call from Hermès offering her a new Birkin or Kelly handbag recently made and distributed ready to be sold; if the customer does not accept that offering, Hermès will no longer call that customer for any other Birkin or Kelly released in the future, so it’s “imperative” for the customer to buy as soon as she receives that call.

To be called by Hermès to sell a handbag, a customer needs to show a long-term relationship with the brand, showing a history of buying many other Hermès’ products; some people claimed that they waited for one or two years to be called by the company. In addition, each customer is not offered more than two handbags in one year, so by restricting the production of these objects while selecting the customers who will buy them, Hermès is creating this aura of exclusivity that enables it to raise prices given the huge desire instilled in its customers.

In case a customer needs to restore her handbag, Hermès sends the handbag to the artisan who produced it; in case that artisan is already dead, the handbag is sent to an artisan who truly knew about the work of the artisan that is gone. CEO Axel Dumas said in an interview in 2022:

We try not to have more than 250 people in each centre because above 250 people no one knows each other and then it becomes a factory

That’s how the company, through its brand, takes control of its distribution channels, mainly selling its products through its own stores, which are carefully located in selected cities worldwide.

In the end, by restricting the number of stores and their strategic placement, Hermès has managed to keep a sense of prestige and exclusivity, ensuring that customers always see Hermès as a high-end and exclusive brand, driving up demand for its products.

Secondhand market

Not only customers who end up being the end customers are the only ones interested in these handbags, but also collectors and investors take advantage of this very active secondary market where rare designs of these handbags are traded:

loveluxury.ae/

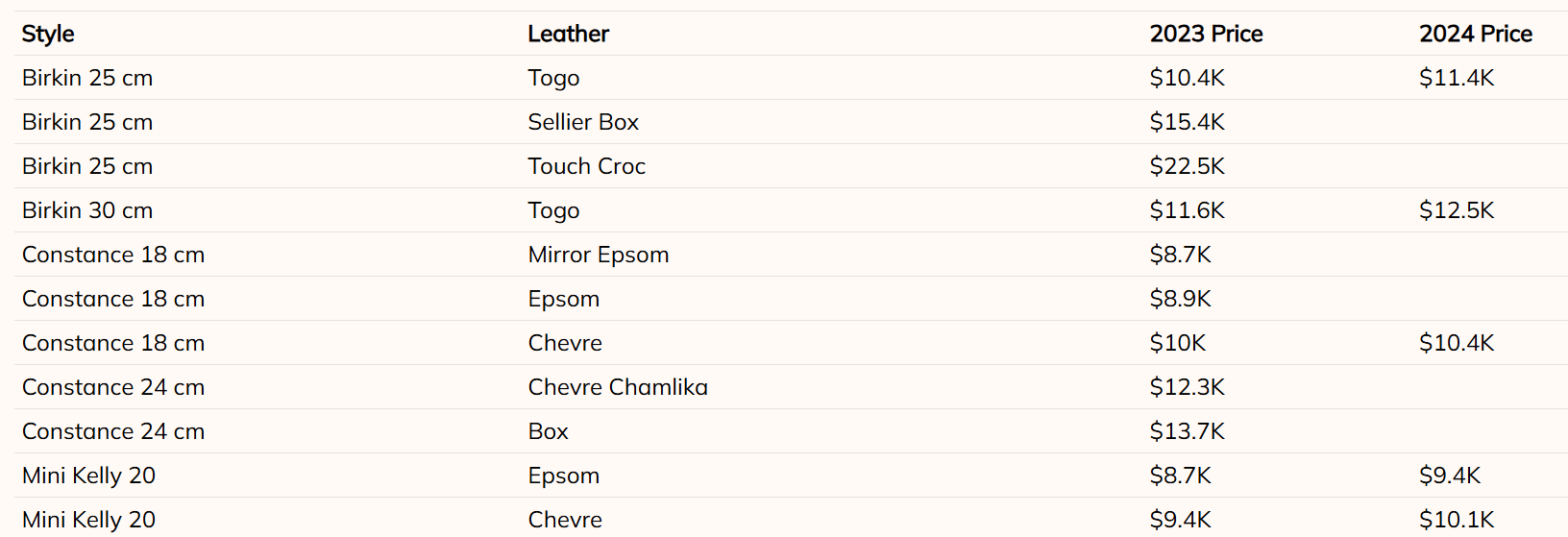

In the table above, we can see different prices for each type of handbag for 2023, and some of them that keep being in that market experienced price increases of more than 7% YoY. Given the fact that these handbags are strongly desired, there is a very active secondary market where lots of collectors and investors are willing to pay even higher prices than those set by Hermès when they are released for the first time.

As such, the secondary market is another strong driver for a consistent demand for these handbags. So, we can picture how the system set by the company actually works: more and more people are interested in those handbags who might be collectors, investors, or end users; thus, under any circumstances, all of them need to buy more and more of other Hermès’ products in order to keep building up history that enables them to be considered future customers of the new handbags.

Metrics reflect the very strong moat compared to its main peer: Louis Vuitton

As you would expect, Hermès’ competitive advantages can be seen through outstanding metrics that I should say are very difficult to see in any other company worldwide.

author, annual reports

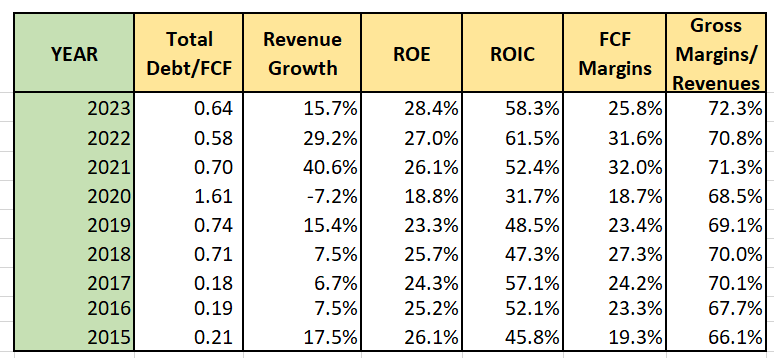

In the table above, we can see consistent revenue growth in the last 9 years, which has delivered consistent and high returns of capital without using much debt. Those debt levels indicate that the company is able to pay its total debt in less than 1 year with its own free cash flow generated each year.

As a result of the higher prices charged by the company given its strong competitive advantages, we can also see a growing gross margin of more than 70% in the last years. I found it very hard to find another company with such metrics not only in the luxury sector but also in many other sectors. That’s why I felt very curious to examine this company to add to my portfolio.

Having seen all of these very interesting characteristics of the company and how profitable it is, it’s not a surprise that its closest competitor, LVMH Moët Hennessy – Louis Vuitton (OTCPK:LVMHF), the largest company in the luxury sector, wanted to purchase Hermès as a coveted target, so its owner, Bernard Arnault, started buying shares since 2001 until getting 4.9% of a stake in Hermès.

In France, companies are required to disclose when the stakes are more than 5% of a target if that target is listed in the stock markets; nevertheless, equity swaps are excluded from that rule, and that’s how Arnault accumulated shares gradually in a decade until owning 23% of a stake in Hermès. However, there were lots of legal battles between the two companies, and Arnault finally distributed most of his shares to shareholders and institutional investors, owning in the end less than 10% of the stake.

I read in an interview with the CEO, Axel Dumas, that he convinced the Hermès’ family, which has around 100 members, to pool their shares in a holding company in the middle of the battle with LVMH to reduce the chance of a hostile takeover.

author, annual reports

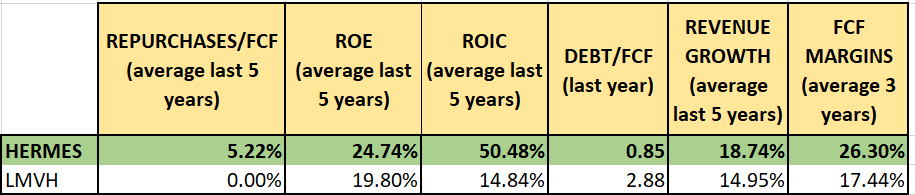

Looking at the average metrics compared with LVMH, we can see why Bernard Arnault was so interested in Hermès, as the latter is able to grow at higher rates with better returns of capital using way fewer debt levels, all of these due to the superior exclusivity developed by the company in the last century.

Valuation

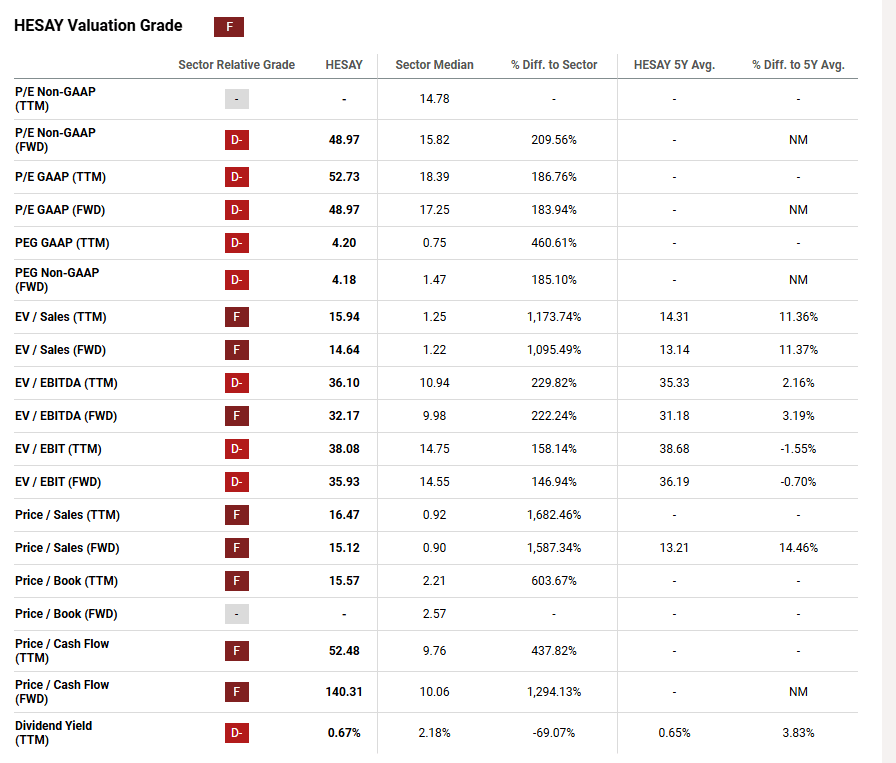

According to SA, the company seems expensive in terms of the different valuation multiples compared to competitors in the sector:

SA

As you may see in the table above, it seems like Hermès is way expensive compared to other companies in the sector. However, as I’ve shown previously, Hermès is a high-quality company whose moat is very hard to replicate even for companies like LVMH, so it’s not a surprise that the market is willing to pay higher multiples than its peers.

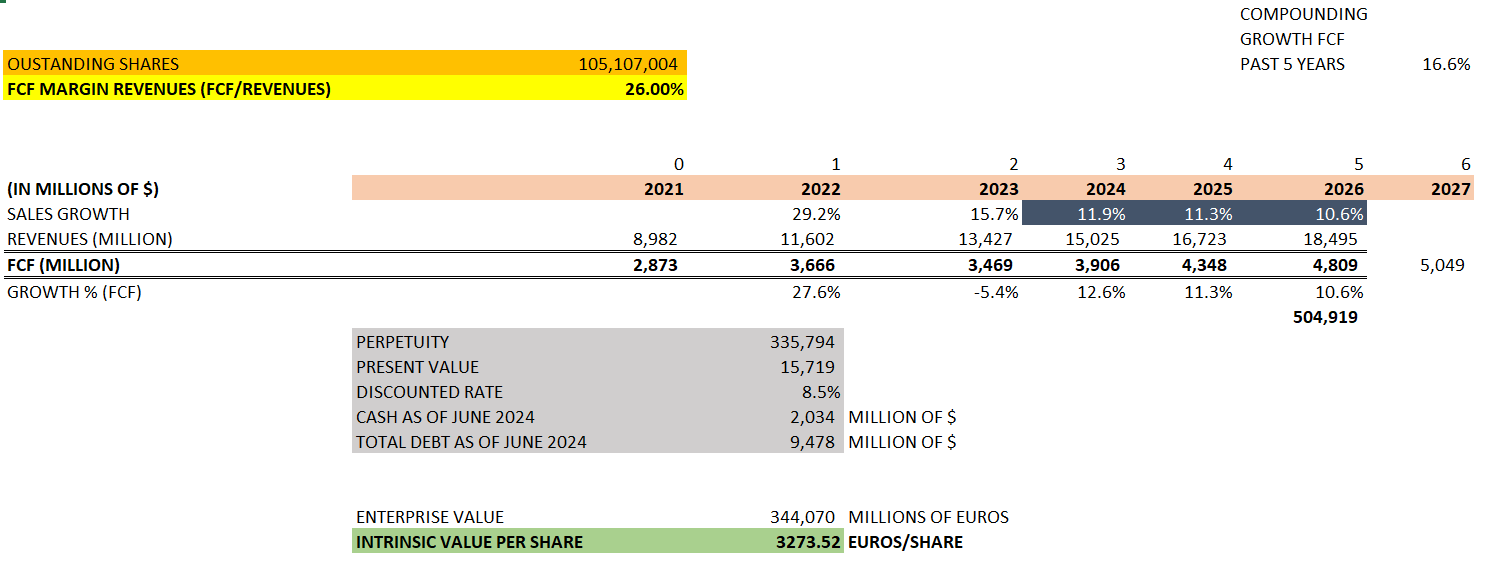

I want to use a DCF approach to complement the valuation system given by Seeking Alpha in order to see if there is an upside in terms of the free cash flows future, as Hermès’ business model is very predictable. I will start with the assumptions:

- Outstanding shares: 105,107,004.

- FCF margins: 26% (the average of the last 5 years)

- Revenue growth: 11.9% for 2024, 11.3% for 2025, and 10.6% for 2026 (consensus).

- Cash as of June 2024: 2,034 million euros

- Debt as of June 2024: 9,478 million euros

- Discount rate: 8.5%.

- FCF growth in perpetuity: 7.5% annual (FCF growth from 2019 to 2023: 16.6% CAGR).

author

To find the perpetuity, we used the formula:

Perpetuity = FCF 2026/(discounted rate – g).

where g = FCF growth in perpetuity, which was assumed to be 7.5% annually.

With perpetuity, we calculate the present value of all the FCFs beyond 2026. Then, we calculate the enterprise value using the following:

Enterprise Value = Present Value of FCF (from 2024 to 2026) + Perpetuity + Cash – Total Debt.

Finally, the intrinsic value is calculated by taking the enterprise value and dividing it by the outstanding number of shares. In this way, we could get 3,273 euros per share under the assumptions presented, which represents an upside of more than 50%.

The DCF approach implies that the investor will hold the stock for the next few years; in the short term, the stock price could move up or down according to different catalysts that might come from the industry, the company itself, the macroeconomy, news, etc., so if the investor is oriented to the long haul, he could buy gradually as the stock price declines eventually.

If I raise the discounted rate from 8.5% to 9%, the intrinsic value declines from 3,273 euros to 2,158 euros per share. Given the context where the Fed is planning to cut interest rates coupled with a rock-solid business model like Hermès, I feel very comfortable with a discounted rate of 8.5%, assuming that you are interested in putting money in this company for the long haul.

I was buying shares at an average price of 2,099 euros per share with a 14% weight in my portfolio. Any meaningful drop in the price would be appreciated to keep adding more shares of this excellent company.

Risks

As every other company, Hermès might face some risks that we need to consider. For instance, a new CEO in the future who might be another member of the family who does not have the skills to lead a company like Hermès. Nevertheless, it’s in the best interest of the family to appoint a CEO who protects their interests in the company, so that risk might be mitigated.

Other risk would be more related to the macroeconomy and how that could impact the consumption. For instance, a recession might impact the demand for the Hermès’ products, reducing revenue growth and margins. However, even when I think that under a recession scenario, the market could reduce the relatively high valuation multiples of the Hermès stock, we should not forget that the Hermès’ target is the wealthier people, so they might not reduce the demand for Hermès’ products because they can afford them and, in general, these people like to enjoy about exclusivity and luxury even in bad times.

Maybe, some investors might consider the country risk as another important risk to invest in the company as most of the company’s operations are in France, particularly when in the recent elections the extreme left wing has won more participation in the congress. For instance, extreme left wings might rise substantially taxes for large companies, which could impact their long-term profitability.

However, there is no majority of any of the parties to govern alone in France, so most likely, there should be negotiations among all the parties which would reduce the most extreme programs. In addition, Hermès is perceived strongly as part of the French culture, and the company has shown a strong commitment with the social corporate responsibility in the country, as CEO Axel Dumas said in the last call for the Q2 2024 results:

Hermès continues to act responsibly when it comes to climate change to protecting biodiversity and natural resources. Our real estate charter is particularly stringent, and is applied from the design stage and the construction stage of our new sites, which allow us to reduce significantly our CO2 emissions.

In this sense, if the stock markets are declining for the economy, or a pessimistic view by investors in general, that would be a good opportunity to buy more shares of Hermès; of course, it would be very conservative to follow up the company to see if the management holds his long-term strategy without material changes that might cause potential risks in the future.

Conclusion

While exploring Louis Vuitton within the luxury industry, I found a company even better with higher margins, lower debt levels, higher returns of capital, and clear competitive advantages. Bernard Arnault was so keen to acquire shares patiently of Hermès for over a decade, which gives us an idea about how good this company really is.

Even Charlie Munger said in 2023 that he was not interested in fashion stocks, with the exception of Hermès at a compelling price. As such, this is a really special company, and to be honest, I have a hard time finding companies like this one in the last years. If you want to diversify your portfolio from the AI hype, maybe you should consider this stock as part of a healthy diversification with an outstanding quality to hold for the next years.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.