takasuu

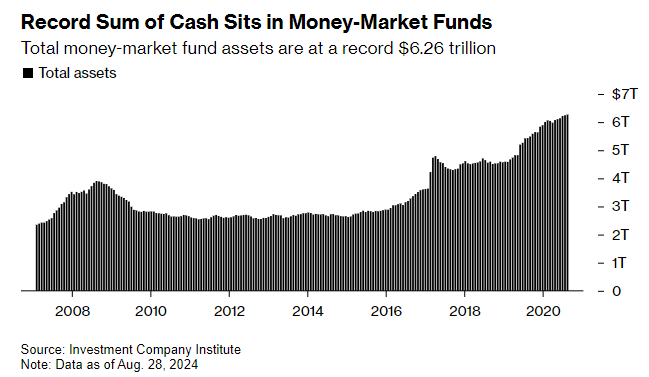

There is now over $7T sitting in US money market funds. That is up from $5 trillion at the end of the first quarter 2023. Today, these money market funds earn just over 5% and investors are t-billing and chilling, as the lower risk appeals to many investors worried about frothy markets and rising rates.

However, the peak in rates is in and fairly soon they will start seeing that money market yield bleed lower. That is why investing in high-quality intermediate-to-long-term corporate bonds is a compelling option here. Traditionally, they have performed well when the Federal Reserve starts cutting rates.

ici.org

Here are four reasons to consider moving some of your allocation towards bonds:

(1) Yields are rolling over and time is of the essence!

Remember, starting yields are a good indicator of your bond’s total return over the time period to maturity. The higher the starting yield, the better your return will be.

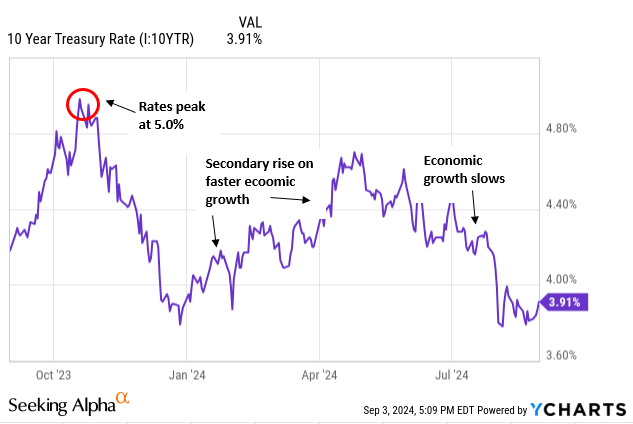

Interest rates have likely already peaked and, since Powell announced the Fed’s pivot from hiking rates, have steadily declined. They are already down more than 100 bps on the 10-year treasury since last October.

AGC, YCharts

However, the yield stated when you purchase your money market fund is NOT a good indicator of that investment return. That is because money market rates are not a fixed coupon and can change daily.

As of this writing, there are almost four 0.25% rate cuts forecasted for the Fed Funds rate for 2024 and nine through the end of 2025. Money market yields are slated to be cut drastically over the next year. Whether or not nine cuts or fewer come through, it is almost certain that money market rates will be lowered 12 months from now. And they could be substantially lower.

Investors are being handed a golden opportunity to LOCK IN these current yields and take advantage of the dislocation in the bond markets. While rates are lower and spreads are tighter, investors, especially risk-averse investors, will likely still benefit from allocating a portion of their portfolios into high-quality longer-maturity, bonds.

(2) Equity valuations are extended

At the same time, bonds are generationally cheap as measured by yields, stocks are generationally expensive. Some would say this is warranted, thanks to the advent of artificial intelligence and its fast growth. ‘This time is different’ has rarely worked out well for investors.

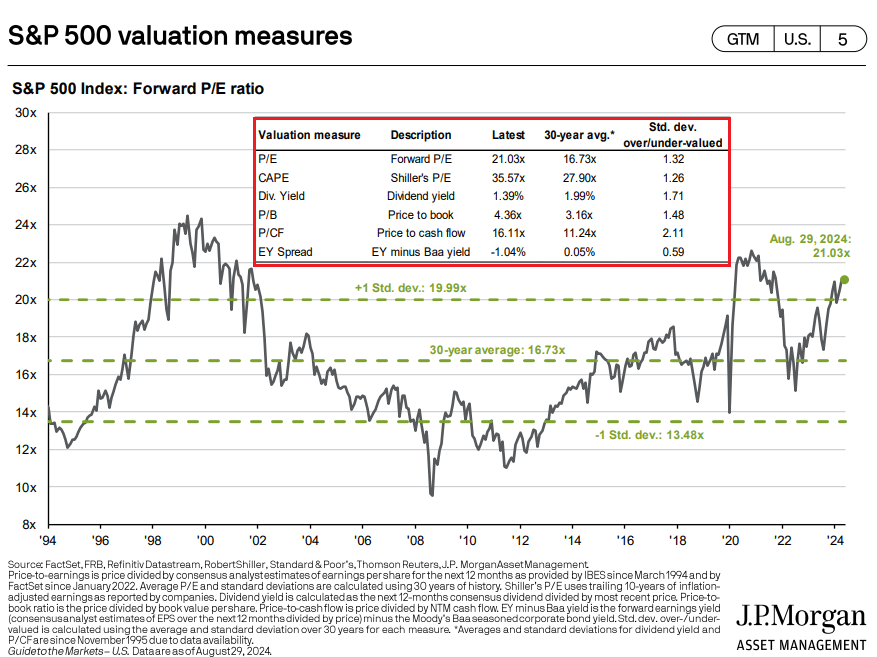

The forward price-to-earnings ratio is now at 21x. Historically speaking, that is over one standard deviation above the 30-year average of 16.7x. And that 30-year period was one of the more expensive periods in the market’s history.

JP Morgan

Outside of forward P/E, you can select one of any other measures to value the markets in the red box. Most are moderately to significantly higher than their long-term averages.

That is not to say that the market is due to correct, although it’s certainly possible. I am not going to pretend to forecast what the market will do. However, I look at history and alter my asset allocation accordingly based on return per unit of risk available to me.

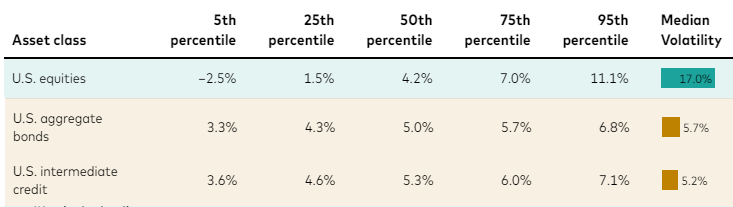

Right now, Vanguard estimates that the S&P will return just +4.2% over the next ten years. That is about half of its long-term average annualized return. Meanwhile, look where they put bonds- both the US Aggregate Bond Index (half investment grade corporate bonds and half US Treasuries) and US Intermediate Credit (5-10 year US corporate bonds).

Vanguard

In other words, you can do better over the next ten years today in intermediate to long-term corporate bonds versus stocks as judged by long-term averages. Then, factor in the volatility column at the end showing bonds are a third of the risk, and you have a VERY compelling argument to allocate something to bonds.

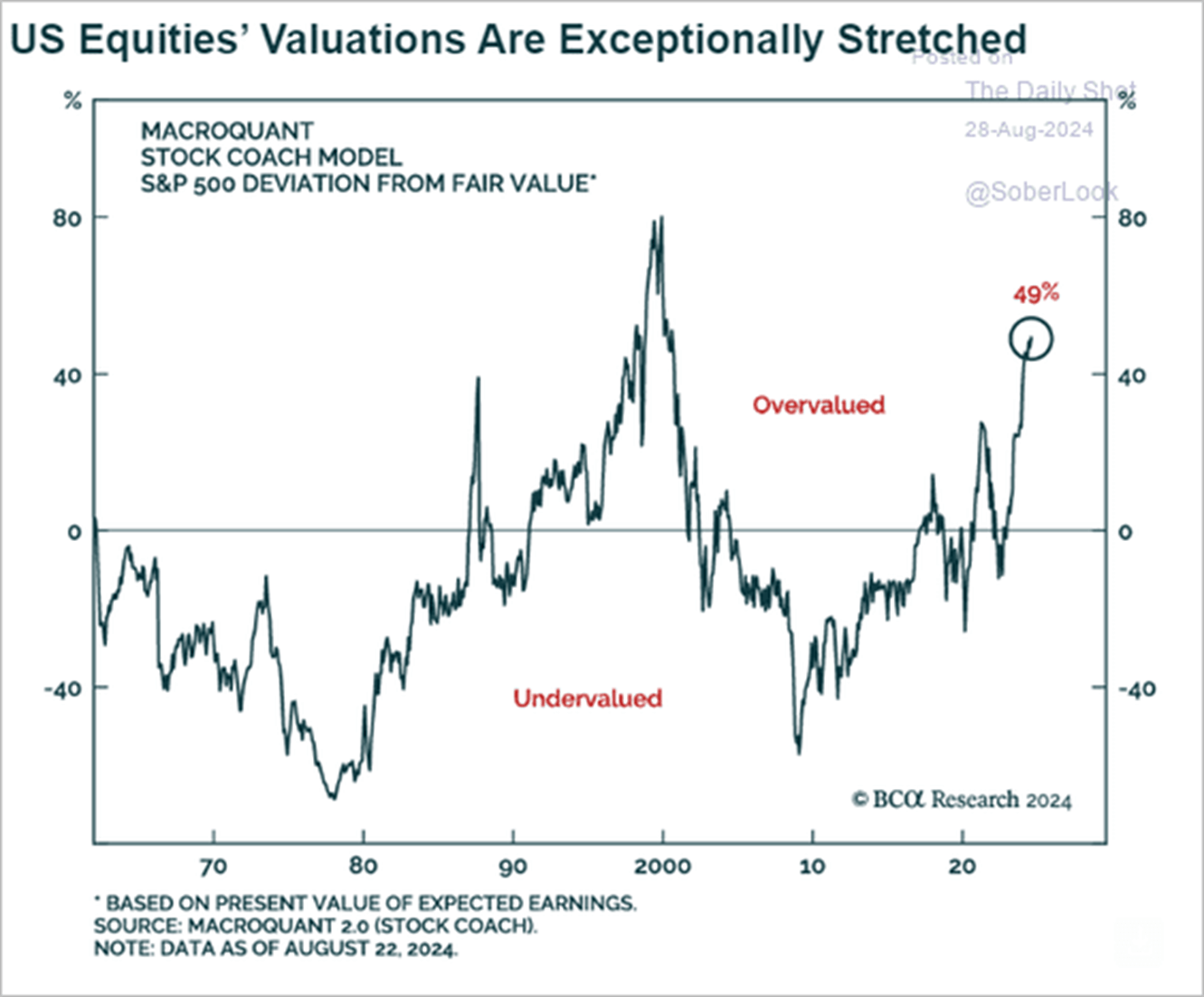

BCA shows that the US stock market is a bit rich….

BCA research

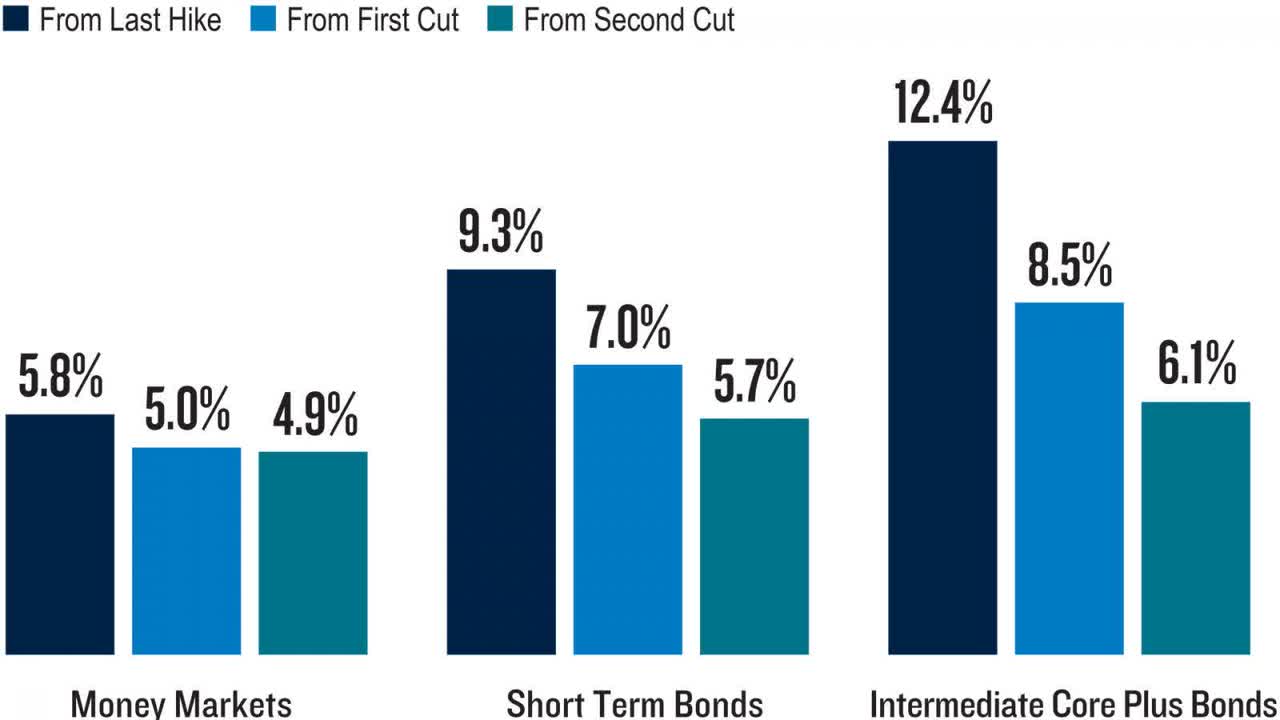

(3) Duration has traditionally been your friend when the Fed starts cutting rates

Extending the duration ahead of the Federal Reserve starts to cut rates during a cycle shift tends to create significant outperformance. As the chart below shows, intermediate core plus bonds (this is industry speak for a multisector fund that is mostly investment grade but juices returns/yields with some junk bonds mixed in) can produce strong returns over the subsequent 12 months.

PGIM

Cash and money markets may seem safe, but they come with hidden risks. In 2024, duration is no longer a four-letter word. A heavy allocation in cash and/or equivalents will likely miss out on substantial capital appreciation opportunities.

The risks of sitting on the sidelines are significant. Personally, I think the largest risk many investors face, especially income investors reliant on their portfolios like retirees, is reinvestment risk.

Reinvestment risk is the chance that cash flows received from an investment will earn less when put to use in a new investment.

Instead, you could purchase a long-term, high-quality bond that LOCKS YOU IN TO CURRENT RATES. I cannot stress this enough.

Many individual investors have never purchased an individual bond themselves, and anything new can be a bit scary. However, recent technological advances at the major brokerages make it as easy as buying a stock or ETF.

One example of a good bond option would be a new issue from JPMorgan (JPM). This is the JPMorgan 5.25% 2044 (48130CRK3), A-, YTW: 5.30%. The bond is call protected until 2029. With a yield-to-worst of 5.30%, you’ve essentially locked in slightly better than money market rates for the next five years (at the worst), and up to 20 years. The bond is very low risk.

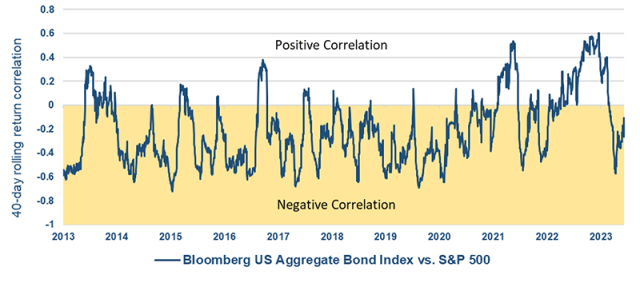

(4) Negative Correlation Creates a Natural Hedge

One of the better and most stealth positive features of owning these high-quality bonds is the natural hedge to your equity positions. This hasn’t been the case for a number of years, but we have finally moved back to a negative correlation between stocks and bonds.

CFAinstitute.org

We are back to an environment where bad news is bad news, sending stocks lower and a ‘flight to safety’ towards bonds. That pushes up bond prices and lowers bond yields. In other words, stocks down, bonds up.

A lot of investors are constantly looking for how to ‘hedge’ their portfolios when one of the easiest ways, and non-costly ways, is right in front of them. I say ‘non-costly’ because you are being paid to own these bonds, whereas in most other hedging mechanisms you have to pay in order to own them. And if they are unused, you lose that capital, a la’ insurance.

A good example is on September 3rd, markets were down more than 1% on a clear ‘risk off’ day in the markets. However, rates fell materially as investors rushed into the safety of bonds. That helped our portfolios be UP on the day.

Concluding Thoughts

Now is the time to get into bonds for the best risk-adjusted returns you are likely to earn in your portfolio in some time. You will not earn Nvidia-like returns, but you will be able to sleep well at night knowing that you are being paid 5.5% or more with a minimal degree of risk.

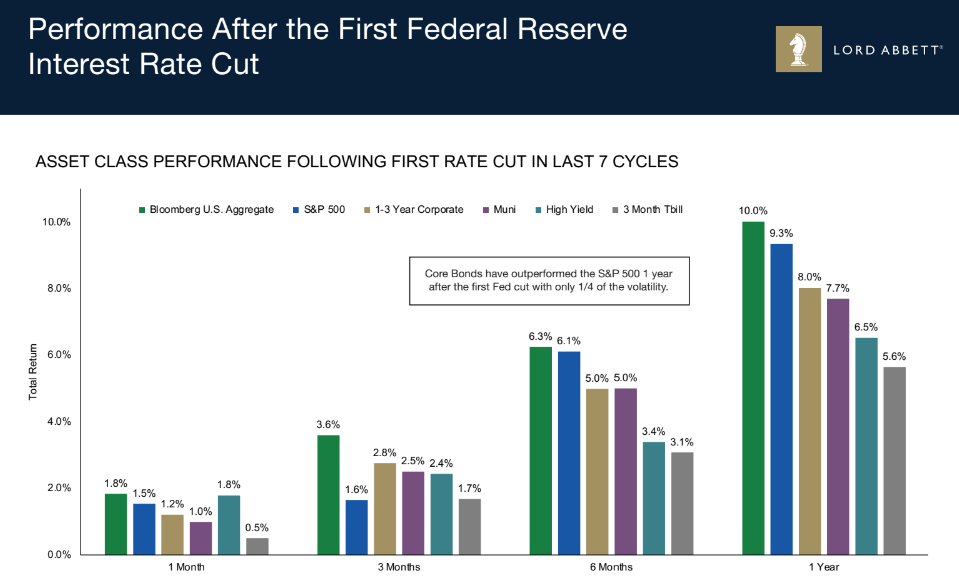

I will leave you with the following chart from Lord Abbett. It shows in the last seven cutting cycles that after one year, the bond index actually returns MORE THAN the S&P 500. Given the current valuations of stocks, I think that could be the case again, one year from today.

Lord Abbett