Jeremy Poland

Investment thesis: Oil (CL1:COM) prices declined recently on mounting evidence of a US & global economic slowdown. Reports from the IEA as well as the EIA, both of which suggest that demand growth is tepid, while supply growth prospects are solid, are creating a market perception of a global oil supply/demand balance that justifies the bear case for oil prices. On the other hand, OPEC is forecasting continued robust oil demand growth, mostly driven by developing nations, and it is of the view that the world is already in a significant supply deficit situation. Both sides cannot be right, given the growing gap between the two opposing points of view, where already existing data for 2024 should cause a convergence in reports. In the process, we have an oil market that is increasingly trading on false assumptions, thus it may be greatly distorted, probably to the downside. The distortion cannot last for much longer, given that more and more data points are coming in that refute current estimates & forecasts being provided. I expect a great deal of oil market turmoil toward the end of the year, and resulting overall stock market volatility will come with it.

The current global oil supply situation and short-term forecasts.

- Crude oil production may have peaked in November 2018.

The EIA has useful data points on global oil supply, with some details that escape the market’s attention. For instance, monthly global crude oil production peaked in November 2018 at 84.6 mb/d. As of May of this year, global production stands at 81 mb/d. Total liquids production is also down, by a much smaller margin for the same period, from 102.3 mb/d to just under 102 mb/d. The discrepancy between falling crude oil production and flat total liquid fuel production can be attributed to a rise in NGLs and other liquid fuels.

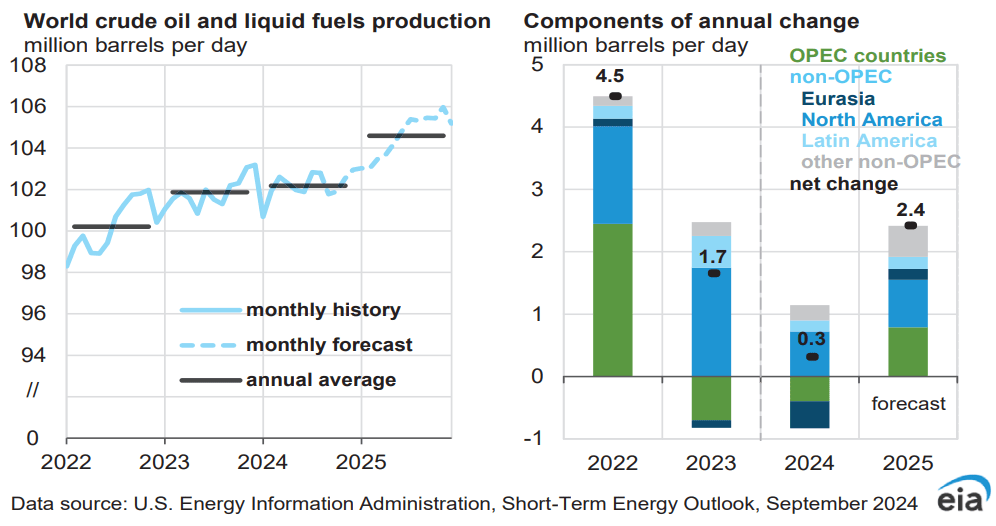

- EIA forecasts a 4 mb/d increase in global liquid fuels supply in the next 12 months from May 2024 levels.

The steep decline in global crude oil supply, which increasingly looks like it might be a permanent peak should be key to the market’s current perception of the global oil market outlook. Given that oil production failed to increase since the end of 2018, we should be concerned and cautious with embracing steep production growth forecasts going forward.

EIA

The headline 2.4 mb/d production growth forecast for next year masks a far greater number, namely a roughly 4 mb/d increase in expected global production between now and fall 2025. It should be noted that the IEA sees a smaller but still impressive 1.8 mb/d increase in global liquid fuel supplies next year.

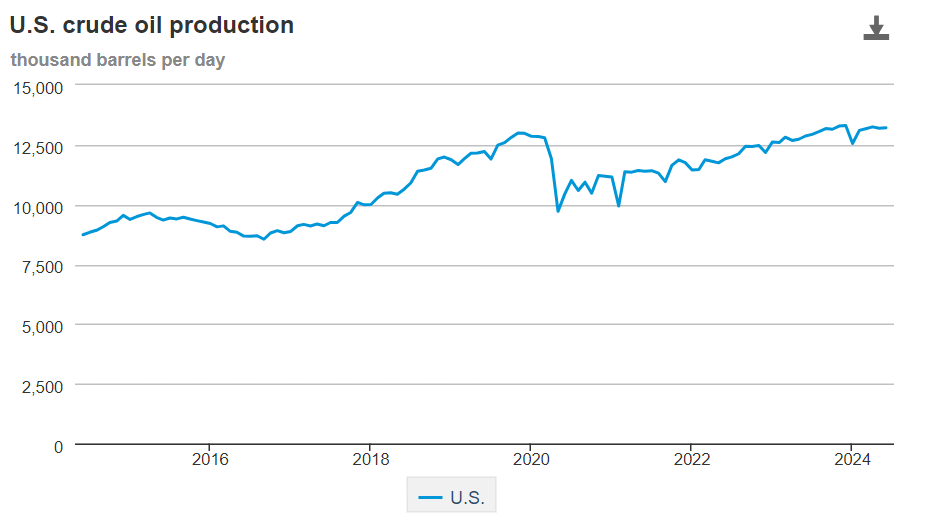

- Risk to the EIA’s US oil production growth forecast for this year and next indicates the prospect for a broader miss.

The EIA is basing its forecast for a significant increase in global liquid fuels production on some questionable assumptions. One of them is that the US is set to see an increase in crude oil supply from 13.3 mb/d this year, to 13.7 mb/d in 2025. For that to happen, US crude oil production would have to rise to about 14 mb/d toward the end of 2025.

EIA

It should be noted that US crude oil production has been averaging about 13.1 mb/d in the first half of the year, so in the second half production will have to average about 13.5 mb/d. It is not the case right now, with preliminary EIA data suggesting that we have been steadily producing about 13.3 mb/d since July.

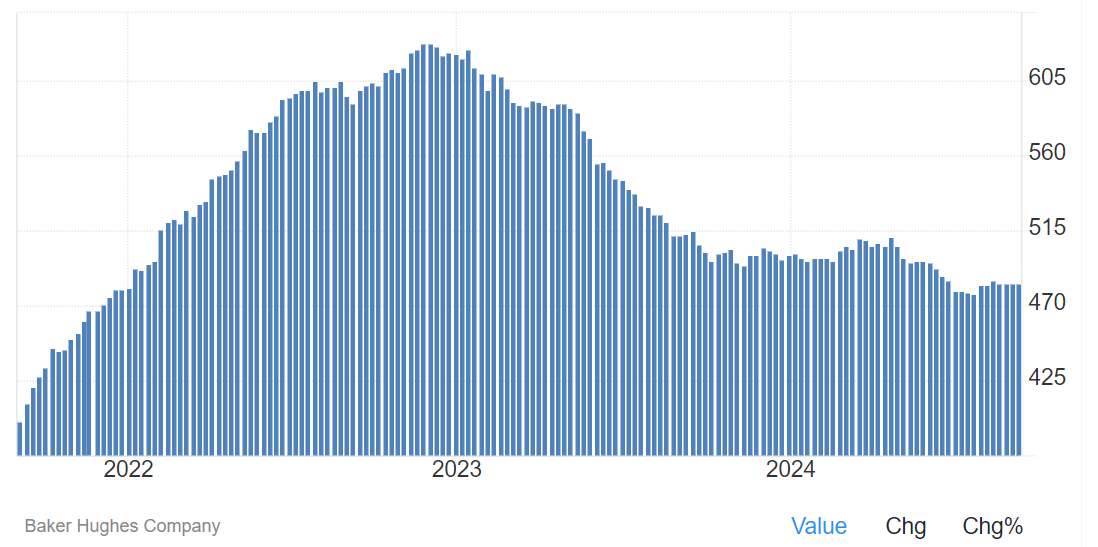

In terms of supply growth prospects in the next few months and into next year, it is hard to see where it will come from, given that the Baker Hughes (BKR) rig count suggests that US drilling activities continue to slow.

Trading Economics

Based on everything we know, the EIA will have a slight miss in its US oil production forecast for this year, by about 100,000 b/d, which will set the stage for a much steeper miss next year. Based on rig activity trends, and a few other factors, I would venture to guess that US oil production will average between 13.2-13.5 mb/d next year.

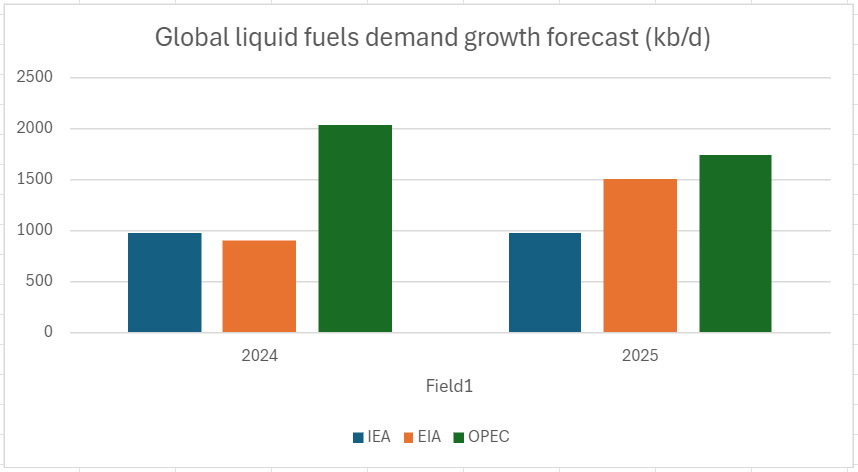

The growing gap in demand forecasts.

- EIA & IEA in growing disagreement with OPEC on global demand.

Given that we are already almost three-quarters of the way through the current year, and fast approaching next year, I find the massive discrepancy in global liquid fuels demand growth forecasts to be puzzling and worrying at the same time.

Data source: IEA, EIA, OPEC

The fact that there is such a wide discrepancy in demand forecasts for the current year is perhaps the clearest indication that at least one or all of the main institutions guiding the market are no longer data-driven. Perhaps if this discrepancy were for a future forecast, with no actual data available for the period in question, it would be somewhat understandable, but we are currently in the ninth month of 2024.

As for who might be right, it is hard for us mere spectators to decipher it. At the moment, based on my surface-level analysis, I’d say that the EIA & IEA might be closer to reality on demand than OPEC. As those who followed my past oil market analysis may already know, I am using a formula to describe the relationship between global GDP growth and oil demand growth.

1.5% yearly efficiency growth + (% increase in oil supply x2) = Potential GDP growth.

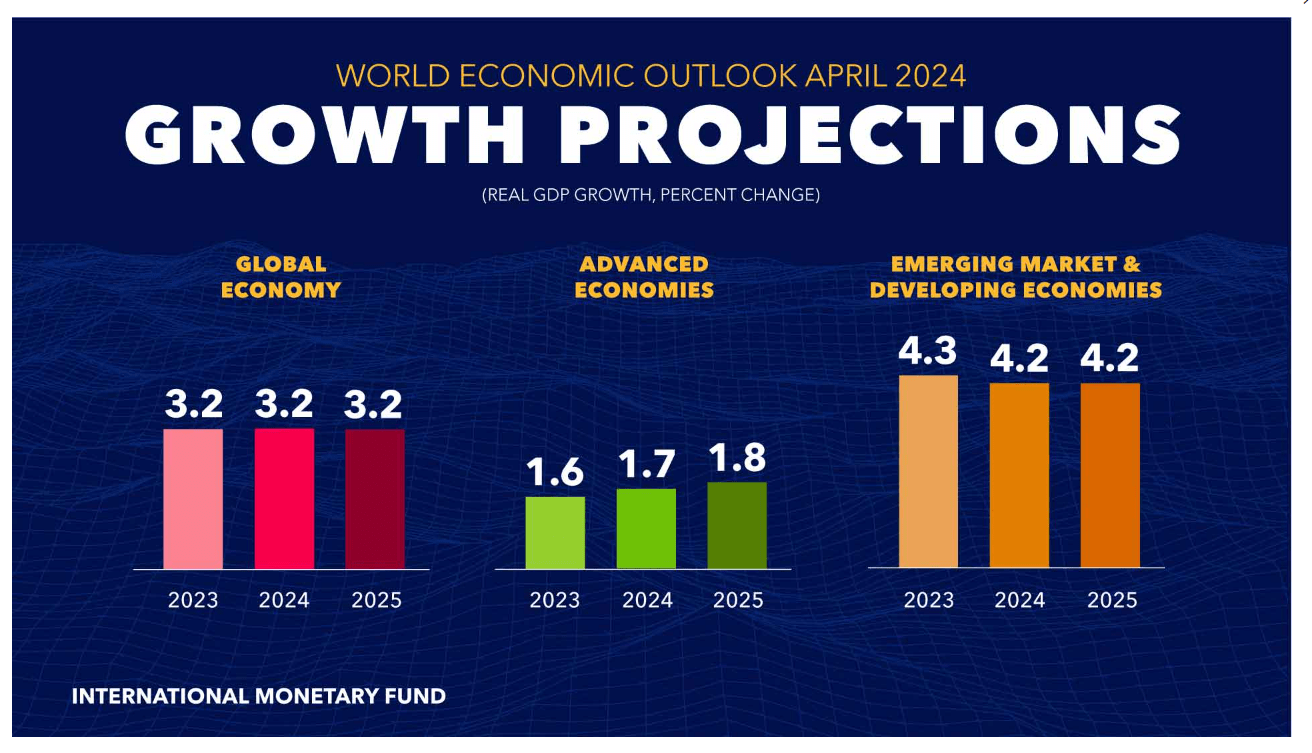

Turning to expected and forecast global GDP growth for this year and next, a roughly 1%/year increase in oil demand seems to fit.

IMF

The one detail that perhaps may skew the thesis in OPEC’s favor is the fact that most of the economic growth is coming from emerging economies, where far more energy is needed to produce economic growth. Based on OPEC’s demand data, non-OECD countries account for about 58% of total global liquid fuel demand. Industrializing economies may experience parity in terms of the percentage change in oil demand versus the percentage increase in real economic output.

The global supply/demand balance.

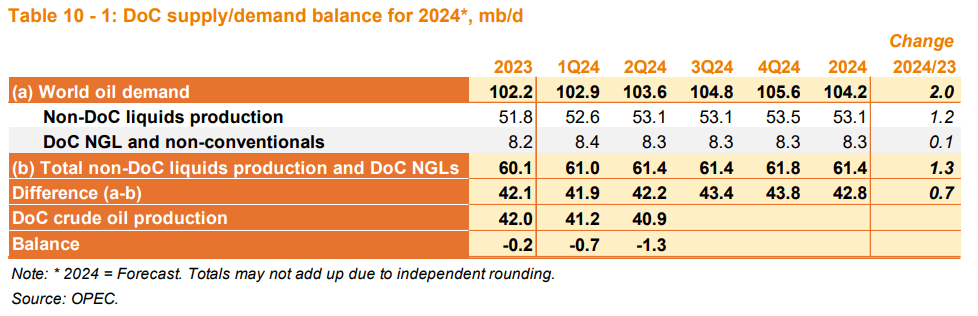

OPEC does not provide a supply/demand forecast. It does provide backward-looking estimates on past quarters.

OPEC

The 1.3 mb/d shortfall in supply for Q2 is a downward revision from the 1.5 mb/d that OPEC reported in its previous report. It might be the only sign that OPEC is backtracking somewhat on its rather bullish outlook for the oil market.

The OPEC supply/demand balance estimate for the first half of the year more or less comes into agreement with the EIA’s supply/demand estimates for this year.

EIA

The EIA sees a global supply shortfall averaging about .9 mb/d this year, and a return to a slight surplus in 2025.

My take is that the .9 mb/d shortfall for this year will be slightly higher once actual data comes in, partly due to a slight supply growth shortfall, but also partly because demand may be slightly more robust this year than the EIA & IEA currently estimate. As for next year’s supply/demand balance situation, the way I see it, it will take a significant increase in OPEC+ production, just to maintain the current level of supply deficit near the 1 mb/d mark.

The global spare capacity assumption.

None of the facts I laid out may matter much if the spare capacity estimates that institutions are estimating and forecasting are close to accurate. The employment of the significant spare capacity that OPEC and others have would easily ameliorate the situation.

EIA

The problem with these spare capacity estimates is that they mostly rely on OPEC members self-reporting their production potential. For instance, Saudi Arabia currently produces about 9 mb/d and it claims to have a production capacity of 12.5 mb/d. However, it never produced that much oil for a sustained period. The maximum yearly average it produced this century was 10.6 mb/d in 2022. I believe that several other OPEC countries and some non-OPEC countries are assumed to have the ability to produce more oil than they can. In the absence of another severe global demand destruction event in the next year or so we will likely find out just how much of that spare capacity exists.

Investment implications:

- An oil price spike in the next 12 months is likely to happen in the absence of an intervening demand destruction event.

The roughly 4 mb/d surge in global liquid fuels supplies between now and next fall that the EIA forecasts that we need to balance the market, is supposed to be starting now, in the second half of this year. I see very little evidence that it is going to happen. If OPEC is closer to being correct on demand growth, we will need closer to 5 mb/d in extra supplies by the fourth quarter of next year. Either way, it is a wide gap that needs to be filled. It is currently assumed that OPEC will play a major role in filling that gap. I do believe they will, but it will not be nearly enough by itself. As for non-OPEC producers, such as the US, as I pointed out, there are already signs that production may come up short of expectations. Not sure how we can expect production to surge, even as drilling activity is in decline. Rig productivity gains may not be enough to make it happen.

My portfolio is currently calibrated for my overall longer-term view that we will have an oil price spike followed by a demand destruction event. As such, I am heavy on cash, sitting at around 30%. I have been taking profits for over a year now, which led to my sizable cash position. I am also heavily invested in oil producers, including Suncor (SU) which makes up about 12% of my overall stock portfolio. I recently sold a small amount of Suncor stock once its share price went over $40. My other major oil producer stock is CNQ (CNQ), which makes up about 6% of my overall portfolio. I recently added some CNQ stock as oil prices declined to the mid-$ $60/barrel range.

- Risks to my portfolio strategy.

While the probability of this outcome is low, there is a scenario that will make my current asset allocation plan inadequate for the outcome. Interest rates may decline this year and next, preventing an economic slowdown. If I am wrong about a global liquids supply shortfall, keeping oil prices low, my significant oil exposure will mostly benefit me in terms of a buy & hold for dividend assets for the longer term, but otherwise, there will be no appreciation in my principal. The economy will probably perform relatively well, on the back of low oil prices and declining interest rates, which can provide the stock markets with a significant boost. My large cash position will amount to an opportunity missed in this scenario.

I am hedging for the possibility that I am wrong on my overall thesis. I have been buying the dip on some stocks. I recently bought shares in AMD (AMD), Intel (INTC), Cameco (CCJ) Energy Fuels (UUUU), Ur-Energy (URG), Ford (F) as well as Albemarle (ALB).

- The Institutional downplaying of what is already a global supply deficit situation this year helps to keep a lid on oil prices, but it cannot last and it may trigger a more severe market reaction later.

This late in the year, there should be enough data available for whichever institutional side is further from reality to have reasonable cause for revisions. For instance, the EIA should by now consider revising the US oil production average for this year slightly down. Even for next year, the current drilling activity data suggests that at least for the first few months of 2025, we are unlikely to see US oil production rising much above current levels. Similarly, OPEC should have enough demand-side data points available to revise its current year forecast, if it may be warranted. Institutional oil forecasts seem to be less data-driven currently than they used to be.

If I am correct and there will be a reckoning in the next few months, it will probably lead to a severe market reaction, rather than a more measured one that would occur if institutional guidance were more in line with emerging data points. A sharp realization of an ongoing and perhaps widening global oil supply-demand imbalance has the potential to call into question further interest rate cuts since higher oil prices can be inflationary. It can call into question economic growth prospects for next year. Perhaps, it may even lead to a market-wide decline in faith in institutional economic data, estimates, and forecasts, if these discrepancies are allowed to continue and perhaps further stray from actual data. We should keep in mind that just recently we had a massive jobs data revision, that raised some eyebrows. We probably will see a return to institutional guidance on the oil market returning to being data-driven by the end of the year, at which point the resulting revisions will trigger a great deal of oil market volatility and stock market volatility. If my thesis is correct, we should brace for an interesting ending to the current trading year.