ElsvanderGun/iStock Unreleased via Getty Images

Following our update on UniCredit-Commerzbank, today we are back to comment on Deutsche Bank Aktiengesellschaft (NYSE:DB). Since our buy rating, the company has continued its restructuring progress, and combined with a favorable interest rate environment, as anticipated, DB’s stock price has returned to a satisfactory level, with a total return of 59.33% since June 2023 (Fig 1).

Mare Ev. Lab Rating Update

Fig 1

Before providing our take on the bank, reporting the latest numbers on the DB home market is vital. In addition, we provide an update on the potential Commerzbank-UniCredit merger and its significant implications for Deutsche Bank. Starting with Germany, corporate insolvencies are rising, signaling once again the crisis affecting Europe’s largest economy. According to Destatis, corporate bankruptcies increased by almost 25% to 10,702 reported cases compared to H1 2023. Even in August, the number of declared ordinary insolvencies increased by 10.7%. In total, we are talking about €32.4 billion in claims vs. last year, which was around €13.9 billion. In detail, looking at the sector, transport, storage, and construction were the divisions mainly impacted.

Related to the Commerzbank-UniCredit deal, the combined entity could become the first direct lending player in the German banking market. This could pressure Deutsche Bank’s margins due to higher price competition. Aside from the lending space, asset management could also be at risk. In addition, regulators may compare Deutsche’s capital adequacy against this new entity, leading to additional capital requirements. This might be decremental for shareholders’ expected remuneration. Additionally, Deutsche Bank might need to reconsider its restructuring strategy, potentially accelerating its cost-cutting plan. If the UniCredit-Commerzbank deal goes ahead, this might consolidate the EU banking assets and set a precedent for other mergers. Deutsche Bank might be pressured to explore similar consolidation opportunities. All in all, in our forecasted numbers, we anticipate a limited impact of this potential merger deal. Here at the Lab, we are more worried about the German economic challenges rather than the potential pressure of higher competition. That said, this deal could force the company to increase efficiency and reconsider its market positioning.

Q2 Results and Our Positive Take

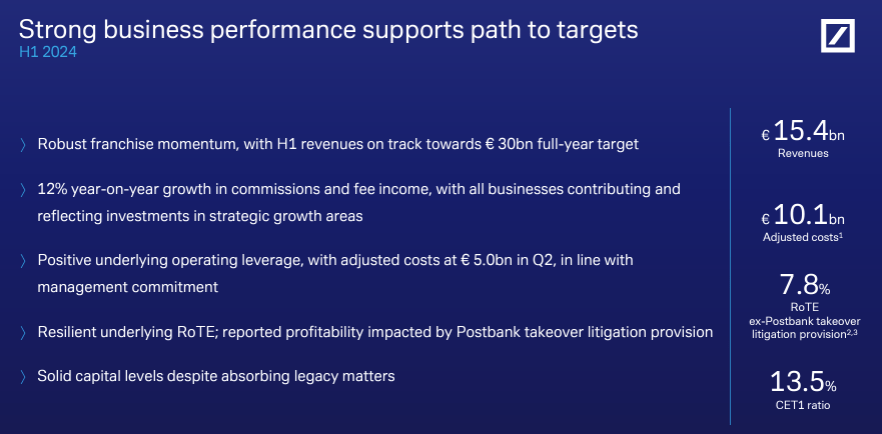

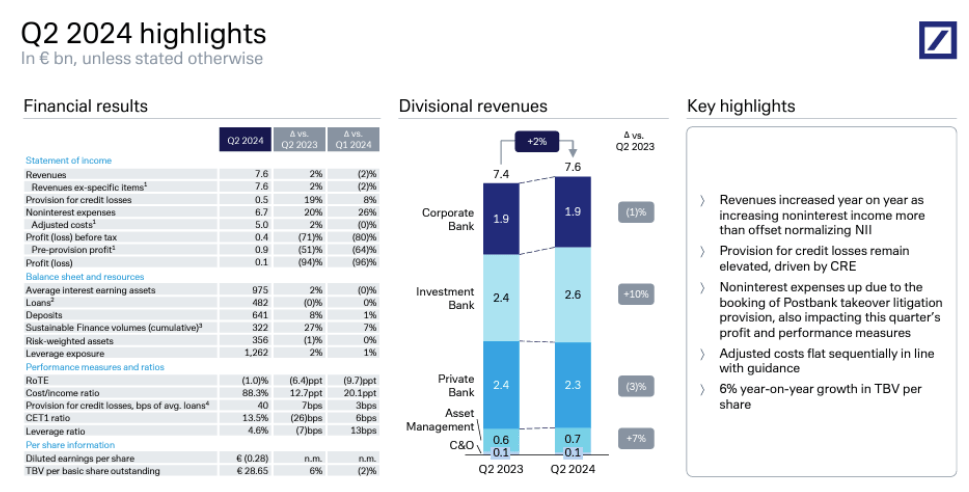

In the quarter, the bank made €7.6 billion in sales, which was a plus 2% ahead of the company’s compiled consensus. Looking at the H1 results, the company reached €15.4 billion in revenue print, putting DB’s €30 billion turnover target well in reach. In addition, the CEO expressed confidence that H2 2024 would be more robust than H1, supported by the CIB market win. In Q2, excluding the Postbank litigation provision, DB’s PBT reached €1.7 billion vs. a €1.4 billion performance achieved in Q2 2023. After commissions & fee income up by 12%, the company still expects better development in Private Bank and Asset Management. Additionally, as reported in the analyst call, this is due not to higher AuM but to higher fees. In H1, the company reported adj. costs down by 2% to €10.1 billion. In Q2, DB’s adj. costs reached €5.04 billion and were aligned with consensus estimates but up 2% on a yearly basis. This was due to wage growth and higher compensation, partially offset by the CIB division’s efficiency measures. The leading German bank reported a CET 1 ratio of 13.5%.

DB H1 Financials in a Snap

Source: DB Q2 results presentation – Fig 1

Here at the Lab, we are still positive for the following reasons:

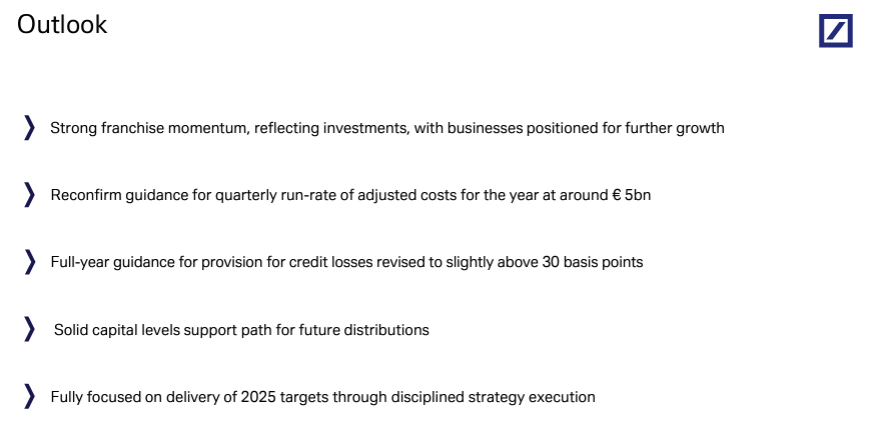

- Aside from the 2% better sales and in-line costs, pre-tax profit was only 4% above consensus. This was due to a miss in loan loss provisions; still, we believe this is temporary. Going into the Fiscal Year 2025, the CEO is confident in a sustained growth generation. For this reason, and despite a non-favorable interest rate environment, we still forecast sales growth of 4% to reach €31 billion. Compared to most other EU banks, the company gets less than 50% of its sales from NII, and with the ECB cuts, we believe Wall Street will favor less NII-reliant banks and more diversified groups. We should also report that fee income generation, including the ECM and M&A divisions, could accelerate with rate cuts. In addition, in our estimates, we aligned DB cost of risk at 40 basis points (as our EU banking coverage); this is slightly above the 30 basis points of the company’s internal guidance;

- The cost-income ratio reached 69% vs. a 73% output in the prior year. Deutsche Bank anticipates operational efficiencies to get closer to a quarterly run-rate of around €5 billion. In our view, this target is achievable, and the company should limit exceptional items to regain investor confidence. That said, the CFO confirmed being able to start with a clean 2025. Therefore, we might expect additional restructuring charges in H2;

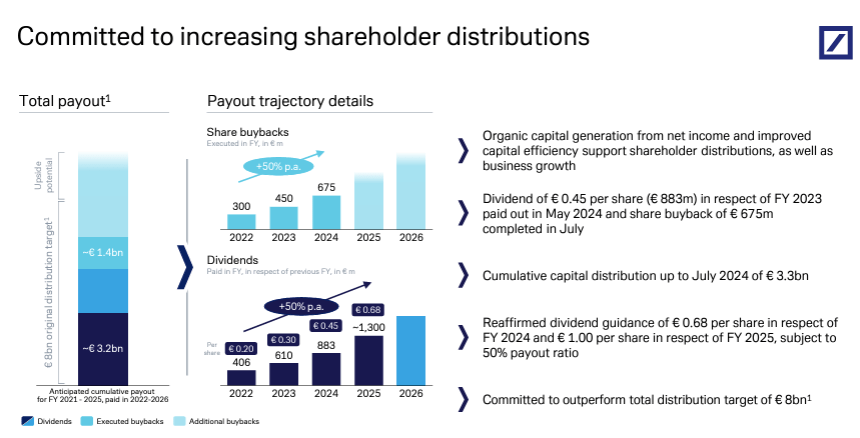

- Considering the company guidance (Fig 3), from the 2024-2026 capital distribution perspective, we are above the target of €8 billion. In numbers, including the buyback and considering a DPS of €0.68/1.00/1.25 in 2024/2025/2026, DB is likely to distribute €9 billion. This implied that DB would return >30% of its market capitalization. This scenario is backed by €4 billion RWA optimization, and the DB’s CET1 ratio might exceed 13% in the cycle.

DB Ongoing Upside

Fig 2

DB shareholders’ remuneration

Fig 3

Earnings Changes and Valuation

Our forecasts are slightly short of DB’s outlook for 2024 as we incorporate the higher cost of risks and potential additional costs into the company’s restructuring process (Fig 5). We view DB’s 2024 sales of €30 billion achievable, and our 2024 pre-tax profit reached €5.9 billion. This includes a yearly total provision projection of €1.6 billion (Q2 credit losses reached €476 million). We arrive at €3 billion in earnings, with an EPS of €2.4. Still, the attractive business MIX offers significant re-rating potential. In our estimates, DB is still cheap. In detail, its P/TBV is still at 0.5x, and looking at the 2025 valuation, DB trades at a P/E of 4.5x with a P/TBV of 0.45x. This bank has an achievable ROTE near 10% and a 30% potential market cap distribution in the next three years. The EU banking sector trades at a higher multiple (P/E of 7.0x and P/TBV of 0.9x). With a 20% discount to peers and applying a blended valuation methodology with a P/E of 6x and a P/TBV of 0.7x, we value the company with a €17 target price. Therefore, we confirmed our buy rating.

DB TBV

Fig 4

DB 2024 Outlook

Fig 5

Risks

DB is exposed to the German and the US markets, given its activity in the CIB division. The company’s profit generation is also subject to credit quality deterioration. That said, even if the home country is not performing well, 70% of DB’s exposure is related to mortgages. This limits the company’s credit risks. Still, a slowdown in the German savings industry might lead to lower net commission fees. In commercial RE, the company has limited exposure. Additionally, DB has a CET 1 ratio above 13%. The Group downside is also related to interest rate evolution, operational risk (cybersecurity), exchange rate fluctuations, and regulatory changes (such as the new Basel 4 requirements). As reported above, a merger between UniCredit and Commerzbank might pressure DB’s margins.

Conclusion

There is a combination of supportive fundamentals and higher remuneration for shareholders. In addition, despite a positive trajectory in CET 1, cost/income ratio, and less NII reliability, the company still trades at the lowest quartile compared to its EU peers. For this reason, our overweight status holds.