Thierry Dosogne

Summary

This note serves as my initial coverage of Danaos Corporation (NYSE:DAC), and by extension, the broader marine shipping industry. My market tilt is usually bullish with a focus on stock to purchase. A surface-level view using my screening criteria and quick trend analysis indicated DAC as a potential Buy candidate. However, after hours of pouring through transcripts, financial statements, investor relations materials, and econ data – as well as the time spent to build a three-statement model, my conviction to Buy this stock is not there. However, we can glean some learnings about what makes the industry and DAC tick and perhaps wait it out for a better entry point.

Business Overview

DAC operates as an owner of dry bulk and container ships. They own some of the largest vessels in the world, including the Hyundai Ambition and Hyundai Speed. Their principal source of earnings comes from charter arrangements that employ these ships for business-related activity for hard goods manufacturers and commodity-related industries.

Hyundai Ambition (Vessel Finder)

Hyundai Ambition (AMBITION)

Hyundai Speed (Vessel Finder)

Hyundai Speed (SPEED)

DAC owns a large fleet of modern, high-capacity container ships. They don’t operate the ships themselves, instead chartering them out to liner companies. This approach brings them a steady income. DAC is heavily involved in the container shipping market, with a significant portion of its fleet dedicated to container vessels. The company has secured multiyear chartering agreements for all their vessels on order and has a substantial contracted revenue backlog. In terms of segments, there are two main operating views: container vessels, which are similar to the ones pictured above, and drybulk vessels, which are used to transport commodities. The key thing to keep in mind is container vessels remain and will remain DAC’s bread and butter for the foreseeable future. DAC is a relative newcomer to the dry bulk space, having acquired a stake in Eagle Bulk while also entering into this business organically via its own Capesize bulk carrier purchases in a multi-prong approach to build this segment out.

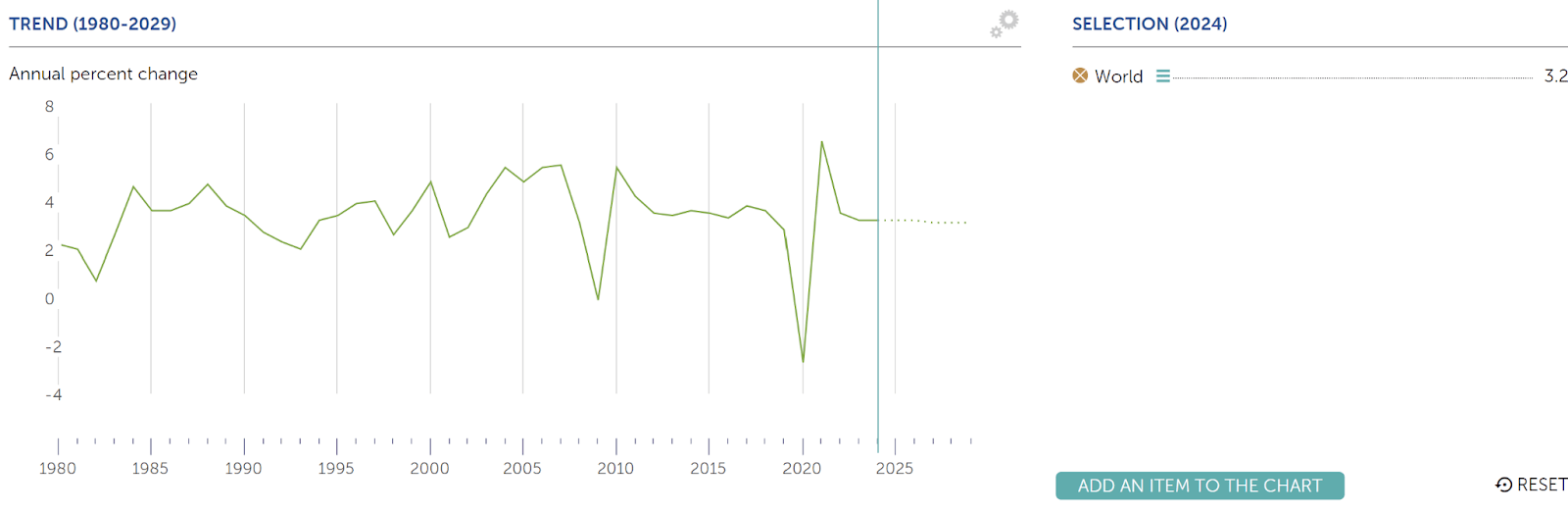

Relevant Macro Themes

Global Trade Growth: DAC relies on the overall health of global trade. An increase in international trade volume translates to higher demand for shipping capacity, potentially increasing charter rates for DACs. Anticipating the supply and demand for capacity is really the key here. The latter is relatively easier to forecast given the long lead times to build vessels, while demand is much more difficult to estimate.

Global Trade (IMF)

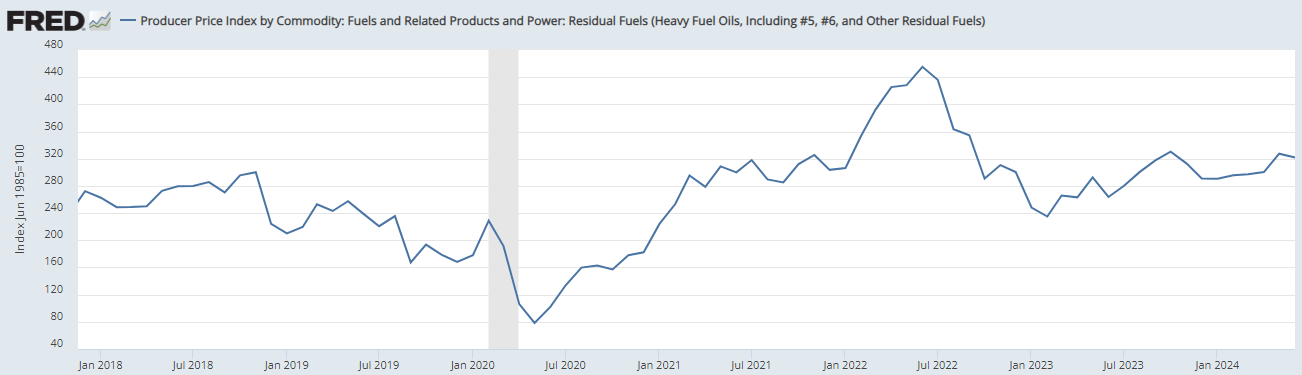

Fuel Prices: Fuel costs are a significant expense for shipping companies. Fluctuations in fuel prices, particularly spikes such as the one experienced in mid-2022 shown below, can affect Danaos’ profitability. Recent trends indicate relative price stability compared to pre-COVID levels.

Vessel Fuel Price Inflation (FRED)

What Separates DAC From The Rest?

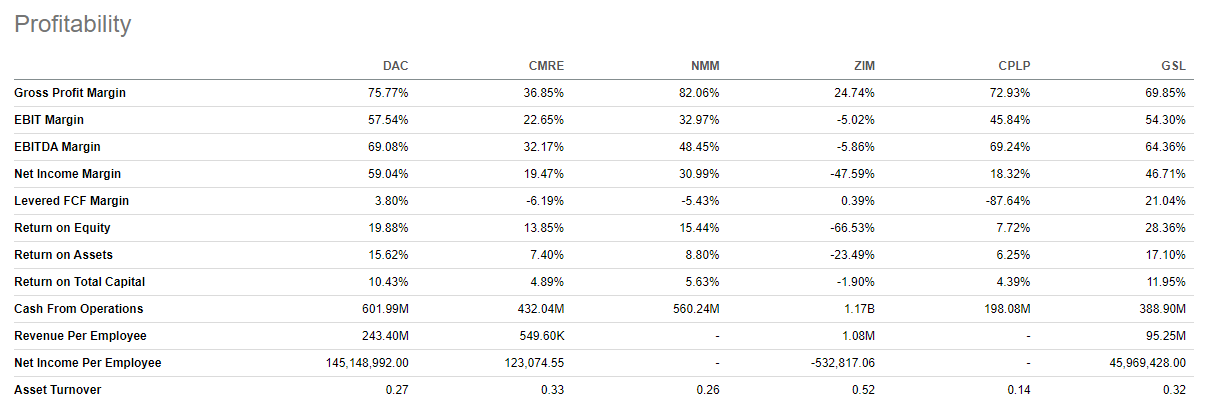

Profitability: If you look at DAC’s margins, they are quite impressive, taken at face value. The more impressive part is when you stack their operating (EBIT) margin against peers. Only GSL comes close. I attribute this to management’s careful approach to deploying capital, which I like. You can check out the table in Seeking Alpha using this link.

DAC Profitability Comparison (Seeking Alpha)

Growth: As noted earlier, DAC management decided to expand into dry bulk shipping. Their cautious optimism in expanding here is one I admire and speaks to management’s duty and care to its shareholders and capital resources. As management recently noted in DAC’s 1Q24 earnings call, profitability has some unknowns that can disrupt profitability, given the sensitivity to fuel prices in this space.

“We definitely are here to stay in drybulk. We would like to have another, let’s say, leg in the company. The only thing with drybulk is that it’s a sector which is highly sensitive to cost. And if you go and commit today into very expensive newbuildings, I’m not sure exactly how you’re going to pay back. And I’m saying that because it’s the fuel consumption on a Capesize today, the way that they are kind of slow steaming is in the region of, let’s say, around 30 tons per day, which is of course — it’s important, but it’s nothing like the 70 tons or 80 tons that a medium-sized containership is consuming. So this gives, of course, the containership a much greater sensitivity to the cost of fuel and carbon eventually.” – Evangelos Chatzis – CFO

Fleet Size and Capacity: DAC operates in key regions including Australia, Asia, Europe, and the United States. This extensive geographical reach enables the company to capitalize on global trade flows and diversify its revenue streams.

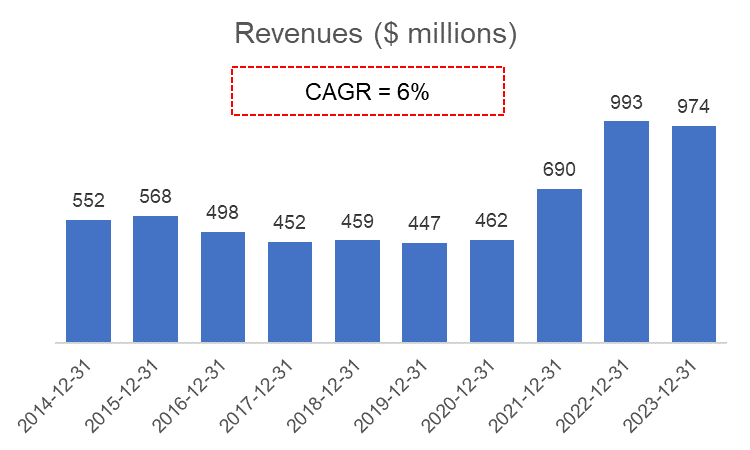

Revenue and Earnings Profile

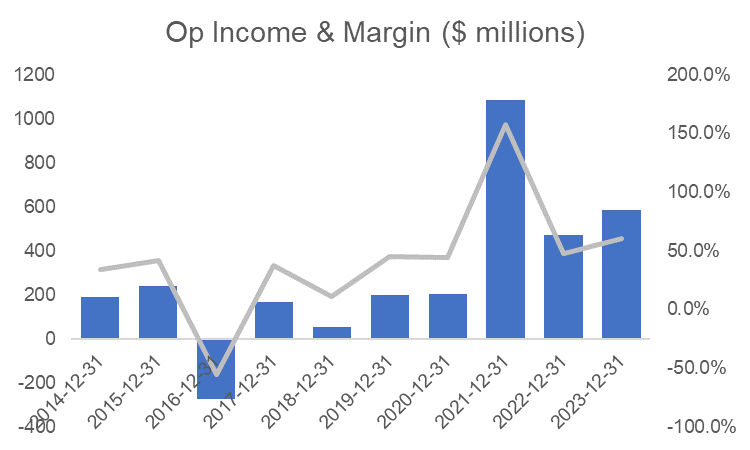

Revenue growth has been relatively healthy over the past decade at a ~6% CAGR. Margins have historically been more volatile, with a dip in 2017 and a spike in 2021. If you smooth those 2 years out, margins have been somewhat steady in the 40-50% range.

DAC Revenue Profile (Author Compiled from DAC Financials)

DAC Op Income & Margin Profile (Author Compiled from DAC Financials)

1Q24 Earnings Call Highlights

DAC reported adjusted EPS of $7.15 per share or adjusted net income of $140 million for Q1 2024. This represents a slight decrease from Q1 2023, where adjusted EPS was $7.14 per share or $145.3 million. The container market strengthened in Q1 2024, with both charter and box rates gaining momentum. The company added $423 million to its contracted revenue backlog, which now stands at $2.5 billion with an average charter duration of 2.9 years. All new-building orders are secured with multiyear chartering agreements, and certain existing vessel charters have been extended.

Financial Statements – Notable Items

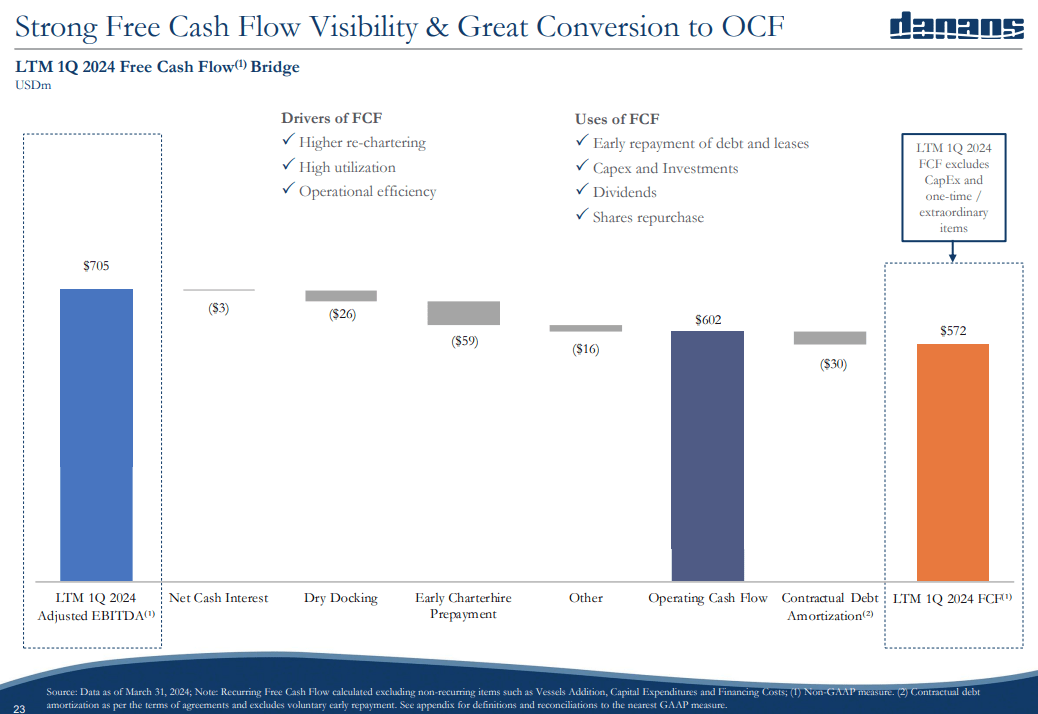

Financial Performance: DAC reported a significant increase in net income compared to the same period last year, driven by higher charter rates and the addition of new vessels to their fleet. The company’s revenue also saw a substantial increase. The nice part of analyzing this company is the predictability of DAC’s earnings stream in future periods. As noted in the earnings section above, management is very transparent with capacity additions and its revenue backlog. This makes forecasting much easier, despite the lack of forward-looking guidance. The last, but not least, important point here is its FCF flow profile, which is part of my stock screen. Positive cash flow is almost a necessity as a value investor, especially for those companies that aren’t new start-ups or in a turnaround situation.

DAC Free Cash Flow (DAC Investor Relations)

Fleet Expansion: DAC is expanding its fleet to bring more efficient capacity online in the coming years, which should bring the total ship count up to 80-ish range, depending on the retirement schedule. Longer term, DAC management appears to be going all in on using “green fuel” vessels. The value proposition for this is tough since we’re talking 10 years out, so it is not something I’m factoring into my valuation but should be on our radar in the coming years.

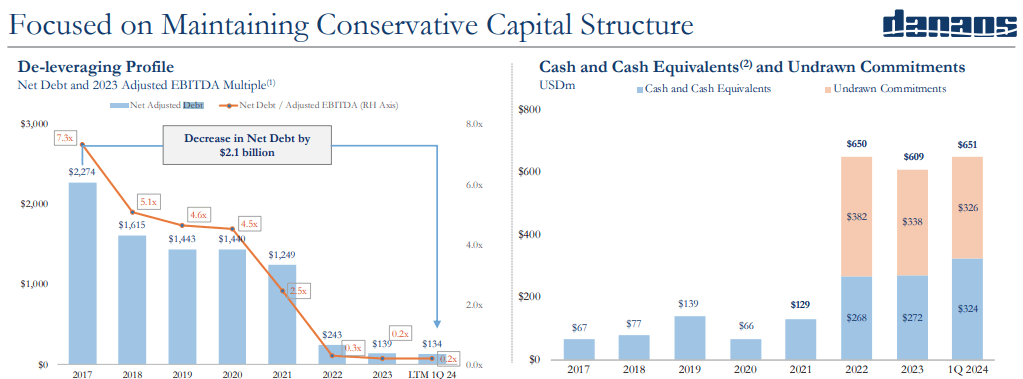

Debt Management: The company has been actively managing its debt, with efforts to refinance existing loans at more favorable terms. This strategy aims to reduce interest expenses and improve financial flexibility.

DAC Deleveraging (DAC Investor Relations)

Shareholder Returns: DAC continues to focus on returning value to shareholders through dividends and share repurchase programs. This reflects the company’s strong cash flow and commitment to enhancing shareholder value.

Dividends & Share Count Considerations

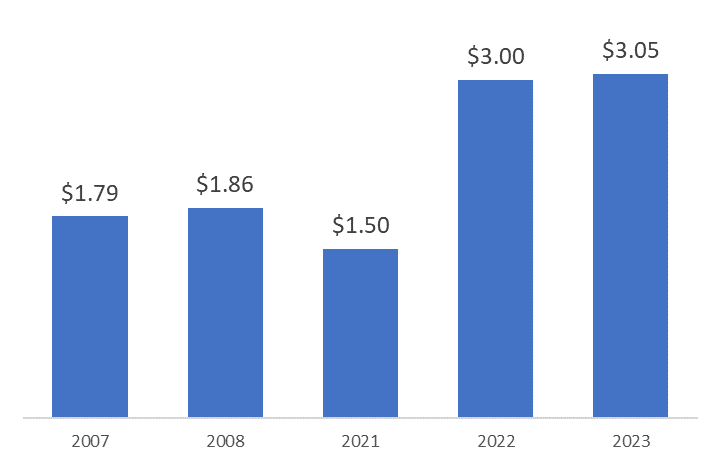

From a dividend perspective, DAC has been a steady quarterly payer, with increasing distributions in recent years. DAC had a 10+ year gap of not paying a dividend, which heightens the risk of the dividend being eliminated altogether in the future. However, given DAC’s track record of quarterly free cash flow generation, I don’t see any serious risk to any dividend cut or elimination at this point in time.

DAC Dividends (Author Compiled from DAC Financials)

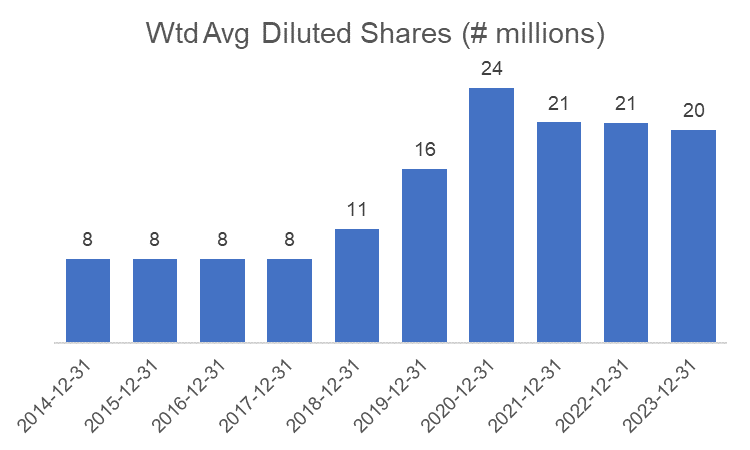

Normally, I would shy away from a company that had an increasing share count, but there’s nuance to everything, right? It’s pretty obvious when you look at DAC’s composition over the years that management has changed its capital stack so that it is less levered via debt. On a 10-year timeline, diluted shares outstanding have increased ~2.5x from 8 million shares to 20 million shares. But at the same time, debt to equity has significantly declined. Since this was done right in the early days of COVID, management got lucky and avoided potential cash flow issues from having to pay interest at rates 5% higher than they were just a few years ago.

DAC Share Count (Author Compiled from DAC Financials)

Valuation

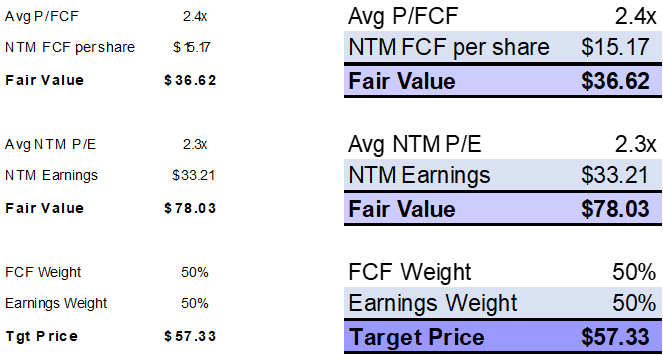

My blended valuation of DAC is ~$57 / share, based on a 1-year forward look of earnings and free cash flow. If I strictly valued this company on an earnings basis, that would bring it closer towards current trading levels but still implies that DAC is trading a bit rich. Management does not provide any forward-looking guidance from what I have read so far, so I’m somewhat in the dark in terms of how to project top lines and margins going forward. Currently, I’ve baked in some very low topline growth while margins remain the same.

DAC Valuation (Author)

Estimates vs. Consensus Ests

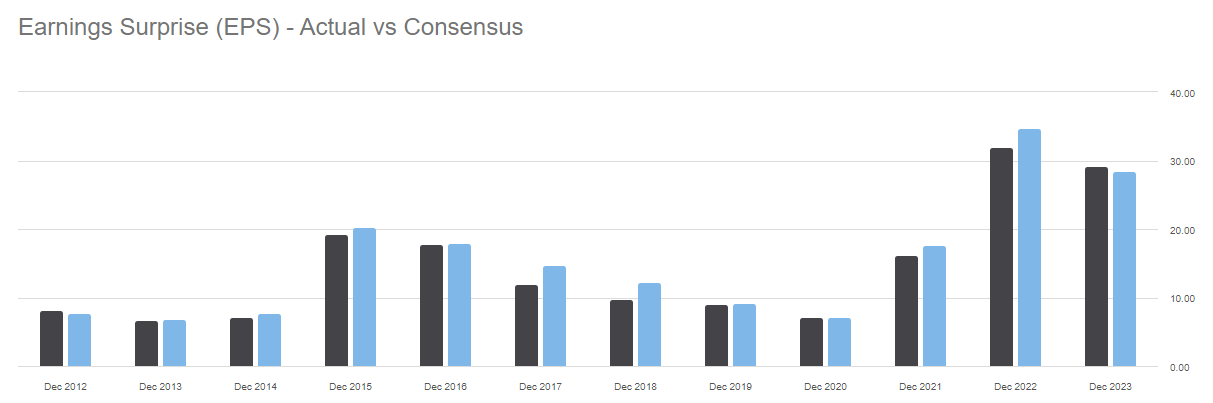

My FY 2024 top line and EPS estimates are higher than the street, and FY 2025 is looking to be a lot more optimistic. Yet, the consensus rating on the sell side is a Buy, and I’m initiating with a Hold. Funny how that works, right? Given the absence of guidance, I’m largely assuming what will go down in future quarters will closely resemble what happened in recent quarters, with some minor tweaking here and there. I’m willing to give management some credit here since DAC has a history of beating consensus estimates in prior periods.

DAC Estimates – Author vs. Street (Author Compiled) DAC Earnings Surprise (Seeking Alpha)

Catalysts / Risks

Strengthening Container Market: The container market continued to strengthen in the first quarter of 2024, with both charter and box rates gaining momentum

Secured Chartering Agreements: DAC has secured multiyear chartering agreements for all their vessels on order and extended charters of certain existing vessels, adding $423 million to their contracted revenue backlog.

Methanol-Ready Newbuildings: All of DAC’s newbuilding order book vessels are methanol-ready, future-proofing a portion of their fleet for green fuel usage.

Expansion in Drybulk Fleet: As mentioned earlier, DAC has made a push to enter the dry bulk market, which should boost and diversify revenues going forward.

Trade Hurdles: The biggest risk to their market outlook comes from trade hurdles that various countries are putting in place in the form of tariffs and trade restrictions, which could result in trade contraction in the longer term.

Availability of Green Methanol: The availability of green methanol, which is important for their methanol-ready newbuildings, is not expected to be available before 2030, which is the time horizon of their charters.

High Interest Rates and Capital Costs: High interest rates and capital costs make it difficult to justify investing in new, expensive drybulk newbuildings.

Conclusion

DAC initially appeared promising as a potential investment. However, a deeper dive into its financials and market dynamics reveals a more complex picture.

The company boasts strong financial performance, characterized by increasing revenue, net income, and healthy margins. Its decision to reduce debt and return capital to shareholders through dividends and share repurchases is seen as a positive. Additionally, the company’s strategic expansion of its fleet, including investments in environmentally friendly methanol-ready vessels, positions it for future growth.

Nevertheless, the company’s valuation is currently stretched, and the absence of concrete forward-looking guidance introduces uncertainty. Moreover, the shipping industry is subject to external factors like trade restrictions and fluctuating interest rates, which could impact profitability. The company’s foray into the dry bulk market, while strategic, carries risks due to its sensitivity to fuel prices and the uncertain profitability outlook.

While DAC presents a compelling financial profile and exhibits a strategic approach to growth, its current valuation, coupled with industry-wide challenges and the lack of clear future prospects, warrants a cautious stance. Investors may want to consider waiting for a more opportune entry point or for the company to provide more concrete guidance about its future trajectory.