Ca-ssis/iStock via Getty Images

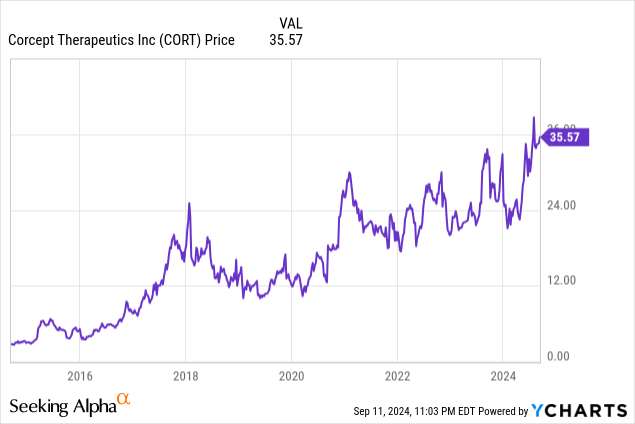

CORT has generated a 28%/year compound return the last 10 years

INTRODUCTION

Corcept Therapeutics Is the Industry Leader in Cortisol Modulation, but is Relatively Unknown and Under-followed. After a Covid impacted Slowdown, Corcept Is on the Cusp of Three Major Catalysts Which Could Reaccelerate Revenue Growth to 37%/year and EPS Growth to 56%/year in the Next 5 Years:

- Catalyst #1 — Will Benefit from What We Estimate Will be a 60 times TAM Expansion in the Cushing’s Syndrome Population.

- Catalyst #2 — Next Year Will Likely Introduce Relacorilant for Cushing’s as a Far Safer and More Efficacious Replacement Drug for Its Current Drug Korlym which Has Just Gone Generic.

- Catalyst #3 — Reports Phase 3 Data by the End of This Year for Relacorilant for Platinum-Resistant Ovarian Cancer that could Double Overall Survival Rates and Be the First of a Wave of Cortisol Modulators which Could Provide Unique New Solutions to Large Therapeutic Areas.

From its founding 25 years ago, Corcept has focused its science on the effects of the cortisol stress hormone on various diseases, a medical pathway that had proven difficult for Major Pharma to address. Initially, it successfully repurposed an old cortisol modulating compound for FDA approval of Korlym in 2012 to treat patients with Cushing’s syndrome, an unmet and rare excess cortisol disease. Recently Corcept published a study showing that the prevalence of Cushing’s syndrome is 60 times larger than the medical community has believed for decades.

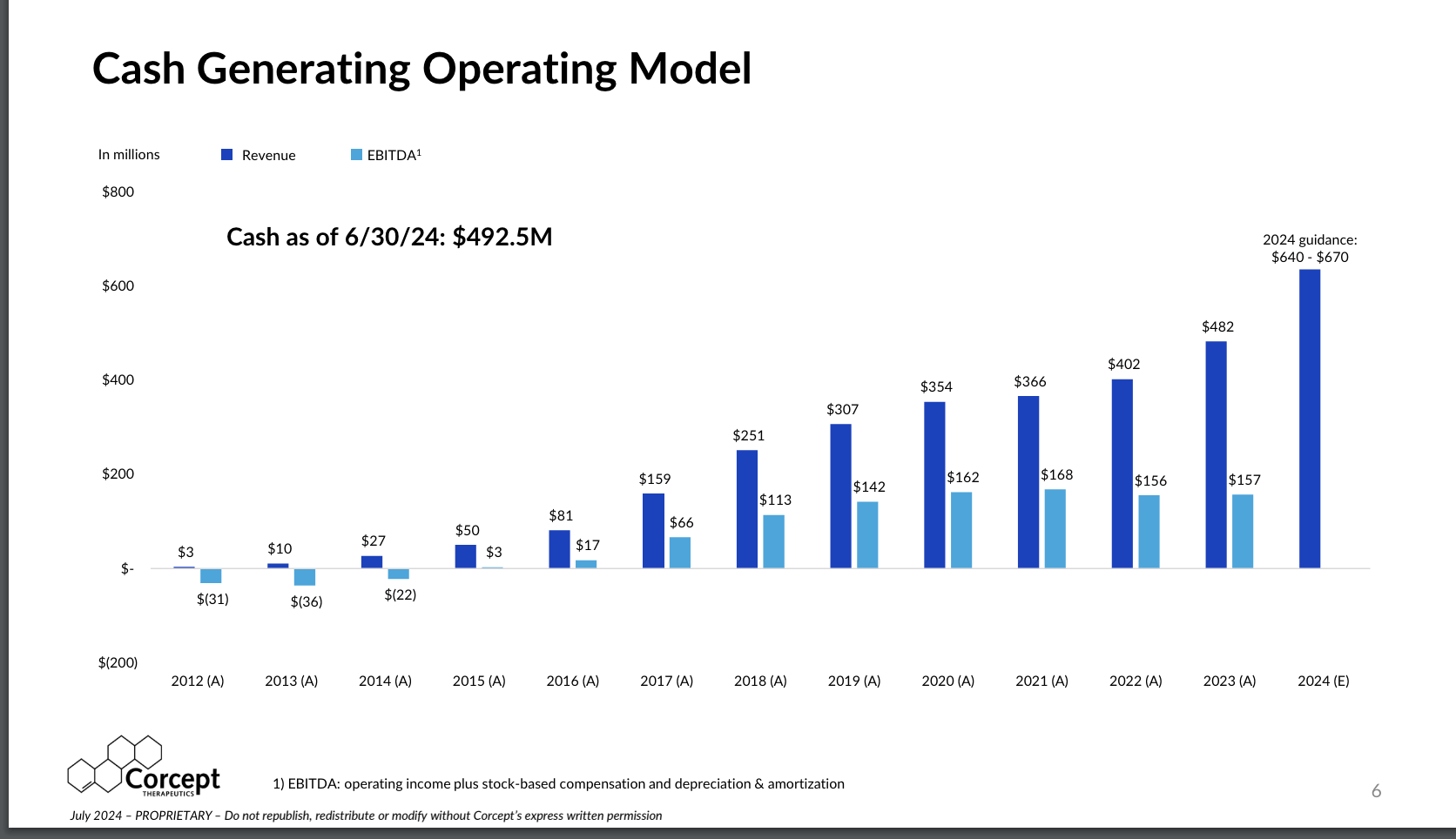

An unusual accomplishment in the biotechnology industry, Corcept has built a profitable, self-financed growth company with revenues compounding at a rate of 47%/year the last 10 years by helping patients manage their rare disorder, Cushing’s syndrome (hypercortisolism).

Cushing’s is a potentially debilitating disease causing excess production of the cortisol hormone, often called the “stress hormone,” that can lead to multiple co-morbidities (hypertension, diabetes/metabolic syndrome, weight gain and depression) and a 5-year average lifespan if left untreated.

Corcept has $492 million of cash, no debt and strong cash flow which should enable it to finance the development of several new cortisol modulating candidates in Phases 1, 2 and 3. The first, Relacorilant for Cushing’s, improves significantly on its existing Cushing’s drug Korlym, with additional compounds that address ovarian cancer, ALS, MASH, prostate cancer, adrenal cancer and an unusually wide variety of other therapeutic areas.

At $35.71/share, Corcept (NASDAQ:CORT) is selling at 28.8 and 16.9 times our EPS estimates of $1.24 and $2.11/share for 2024 and 2025. If Corcept sells at 15 times our forward 2028 estimate of $8.86/share, in three years it would reach our target of $133/share.

FINANCIAL HISTORY

Corcept has grown revenues at 47%/year (Corcept)

Source: Corcept July Investor Investor Presentation

Corcept Has Had a History of Rapid Growth in Revenues and Strong Margins

Corcept has grown its Korlym revenues at a rapid 47%/year compound rate in its first 10 years of commercial sales, to $482 million last year (2023), up from $10.3 million in its first full year of revenues in 2013. Net profit margins were strong at 22% in 2023.

Annual growth rates slowed during the 2020-2022 Covid years as patients and the salesforce were not able to meet with doctors, but sales returned to 20% growth in 2023 as shown below. Revenues typically grow a few percent faster than patient count as Corcept typically raises prices a few percent every year as many pharmaceutical companies do to offset inflation and fund R&D.

On July 29, 2024 Corcept reported H1 2024 revenues of $310.6 million, up 39.0% vs. H1 2023, and EPS of $0.57/share fully diluted, up 50.0% vs. $0.38/share in H1 2023, with cash on June 30, 2024 of $492 million and no debt.

Note that our financial models use company published revenues and we make estimates of average patient count based on gross price per patient, estimates of modest annual price increases, gross-to-net discounts of 15% off of posted list prices and Corcept offering free drug to approximately 15% of patients due to insurance ineligibility.

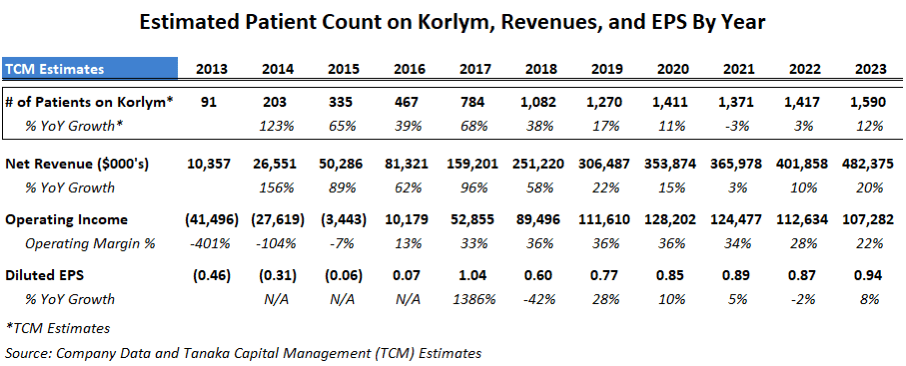

It is important to be aware that Korlym is a maintenance therapy and while it has had a low patient count due to Cushing’s ultra-rare status to date, patients tend to remain on Korlym for years to avoid the deleterious effects of hypercortisolism. This contributes to a steady recurring revenue stream, and Corcept has been successful in growing the patient count with the exception of the 2020-2022 years of Covid-restricted doctor visits:

Estimates of Korlym patient count, revenues and EPS (Tanaka Capital Managment)

CATALYST #1 – LARGE EXPANSION OF TOTAL AVAILABLE MARKET (TAM)

Corcept Prevalence Study Shows Hypercortisolism Has Been Underdiagnosed by 60 Times

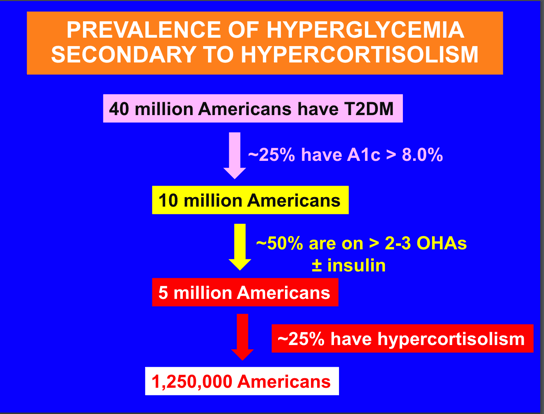

Corcept has believed for years that the Cushing’s market has been underdiagnosed and is larger than the 20,000 patient rare disease population the medical community has been estimating. Based on its experience with its actual patient base, Corcept suspected many Type 2 Diabetics that were not responding to insulin, GLP-1s and other anti-glycemic meds might actually have hypercortisolism (elevated cortisol or Cushing’s syndrome).

Last year Corcept initiated a prevalence study of 1055 “Difficult-To-Treat” (DTT) Type 2 Diabetic patients, also called “non-responsive Type 2 diabetics” since they are not responding to insulin, GLP-1s and other anti-glycemic meds. Final data from this CATALYST prevalence study were announced on June 24, 2024 at the American Diabetes Association (ADA) 84th Scientific Conference and revealed that an astounding 24% of “Difficult-To-Treat” Type 2 Diabetics had tested positive for hypercortisolism (Cushing’s syndrome), a fact which is not currently known by doctors treating diabetic patients.

Underscoring how much the medical community has been underdiagnosing hypercortisolism, the prominent endocrinologists who performed the prevalence study trial were polled before the trial and they estimated that zero to 5% of their Difficult-To-Treat Type 2 Diabetic patients tested might have hypercortisolism. The midpoint of their predictions was 2.5% and the trial’s 24% prevalence was 10 times higher than they anticipated.

The primary investigator of the prevalence trial, well-known University of Texas endocrinologist Dr. Ralph DeFronzo gave a speech on June 7, 2024 (Hypercortisolism Impact on Hypertension and Hyperglycemia and Beyond presenting this waterfall graphic below estimating 1.25 million Americans with Difficult-To-Treat Type 2 diabetes have hypercortisolism:

Prevalence of Hypercortisolism Among Difficult to Treat Type 2 Diabetics (Corcept Therapeutics)

Source: Corcept Therapeutics website June 7, 2024 “Hypercortisolism Impact on Hypertension and Hyperglycemia and Beyond” by Dr. Ralph A. DeFronzo.

Our models are based on the final data showing 24% prevalence of Difficult-To-Treat Type 2 Diabetics likely to have Cushing’s or 1.2 million Americans. Our estimate of 1.2 million Type 2 patients with Cushing’s is 60 times the 20,000 traditional Cushing’s population estimate.

Cushing’s is a potentially fatal disease and most of these Type 2 diabetics (and their doctors) don’t know they have it. In addition, rather than the Type 2 diabetes causing the Cushing’s, Corcept believes it is the opposite, that excess cortisol is actually causing the Type 2 diabetes and may be blunting the effectiveness of GLP-1s for some Type 2 patients.

Prominent Endocrinologists Discussed Prevalence of Hypercortisolism at ADA in June

For a better perspective, I attended the formal presentation of the prevalence study data at the June American Diabetes Association conference in Orlando and was fortunate to meet Dr. DeFronzo and other presenting endocrinologists as well as members of Corcept management.

Two ADA panel discussions were dedicated to hypercortisolism: “Perspectives in Hyperglycemia Secondary to Hypercortisolism – A Path to Diagnosis” which discussed the need for more testing for hypercortisolism and “Prevalence of Hypercortisolism in Difficult-to-Control Type 2 Diabetes” discussing data from the Prevalence portion of Corcept’s Phase 4 CATALYST clinical trial. Session comments from presenting doctors:

- “Hypercortisolism is a devastating disease that affects all organs of the body and takes a while to have an effect, especially for cardiovascular disease. (JUST) managing comorbidities will not work. Of 628 patients (in prior studies with patients with hypercortisolism), 6.4% had myocardial infarctions vs. 1.5% without hypercortisolism, and 5.1% had strokes vs. 1.5% without.”

- “The longer you wait to make the diagnosis, the more you will see cardiovascular events and the worse off patients will be.”

- “It has been recognized since 2008 that most patients who have hypercortisolism aren’t necessarily going to have the obvious physical conditions but will have diabetes, weight gain, hypertension, depression.”

- “If (your patients) have diabetes and hypertension is difficult to control, you should test them (for hypercortisolism).”

- “We will have a marked increase in screening for hypercortisolism.”

- “Psychological disturbances are very common for those with hypercortisolism because of the effects on the GR (glucocorticoid receptor).”

- “This new breakthrough CATALYST study shows how hypercortisolism causes hyperglycemia (diabetes).”

- “Cortisol reduces the synthesis of GLP-1s.” (i.e., reduces effectiveness of GLP-1s)

- “35% of the CATALYST trial patients who were also taking 3 or more hypertension meds had hypercortisolism.”

- “We are on the cusp of a paradigm change.”

- “This is the most important presentation at this ADA.”

Why Is Hypercortisolism So Underdiagnosed?

Corcept officers tell me that the medical community has been taught for decades that Cushing’s Syndrome (hypercortisolism) is a rare disease with visual symptoms as shown in pictures of Minnie G. the first patient documented by Dr. Harvey Cushing in 1912. NIH, the US National Institute of Health, describes the Cushing’s symptoms as “weight gain, thin arms and legs, a round face, increased fat around the base of the neck, a fatty hump between the shoulders, easy bruising, wide purple stretch marks and weak muscles.” NIH furthers states that “not everyone with Cushing’s has these symptoms, which can make it hard to detect.”

Difficult to detect and rare, it took until 1940 to discover that elevated cortisol is the cause of Cushing’s. 84 years later we now learn that hypercortisolism is 60 times more prevalent than believed.

Going forward, one challenge will be that 90% of diabetics are treated by general practitioners rather than by endocrinologists. Until now they have had little reason to test for hypercortisolism because as Dr. DeFronzo said in his presentation, “most patients with hypercortisolism present without classic phenotypic features” meaning most patients with excess cortisol do not show the visible signs of Cushing’s.

We expect that once the need for testing for Cushing’s becomes more widely known by primary care physicians, there should indeed be a “marked increase in screening for hypercortisolism.” The most common test is the dexamethasone suppression test (DST) which is not expensive and one presenter at ADA said the test is 98% sensitive (accurate positives) for the assessment of Cushing’s syndrome.

We Thought that Corcept Had Reached 16% of the Available Market for Korlym in the U.S., but After the Prevalence Study, Its Market Penetration Is Now only 0.26%

Based on last year’s revenues and estimated revenue per patient, we estimated Corcept served an average 1590 patients during the year or only 7.9% of the traditional estimated total Cushing’s population of 20,000. Note, however, that about half of Cushing’s patients eventually elect to have surgery or radiation to remove the adenoma on the adrenal or pituitary glands known to cause the excess cortisol production. This left the remaining 10,000 Cushing’s patients as potential candidates for using Korlym medication as maintenance therapy to moderate the effects of excess cortisol.

Before the prevalence study, using this old estimate of a 10,000 patient population of Cushing’s patients eligible for its cortisol modulating drug, we had assumed Corcept with about 1590 patients had increased its reach to about 15.9% of the Total Addressable Market (“TAM”) for Korlym medication.

But now with the knowledge gained from Corcept’s prevalence study for Type 2 Diabetics, the total addressable market is about 60 times larger at around 600,000 potential patients, and Corcept with 1590 patients last year has only penetrated about 0.26% of the now larger TAM, leaving Corcept considerably more room to grow.

As Corcept gets the word out to help educate the medical community to perform more testing for excess cortisol in “Difficult-To-Treat” Type 2 Diabetics, we estimate it could expand its number of served Cushing’s patients by 10 times (to over 15,000) over the next 10 years which equates to a healthy annual patient growth rate of 25% per year and reach a 2.5% penetration of the expanded TAM.

Why We Wouldn’t Expect Corcept to Multiply Revenues by 60 Times Even If the TAM Is Now 60 Times Larger

(1) Korlym is repurposed mifepristone, the abortion pill, that requires significant guidance and carefully titrated dosing. Side effects can be significant and need to be monitored and managed. New doctors may be slow to prescribe it especially for female patients which represent over half of Cushing’s sufferers and even some male patients may avoid it due to side effects as summarized in the Mayo Clinic description of mifepristone.

(2) 90% of Type 2 diabetics are treated by general practitioners (primary care physicians) so a brand new set of 268,000 physicians will need to be approached and educated on a disorder relatively new to them vs. the 3,000 endocrinologists that Corcept has marketed to for a decade.

(3) As Corcept grows the number of patients served it will eventually have to adjust its price and revenue per patient downward. Korlym has a high list price of $380,000 per year as Cushing’s has been a rare disease and can have high mortality. In the past, Corcept has been able to get insurance coverage approved because patients left untreated can increase mortality by 4-5 times and can lead to 5-7 times higher healthcare costs as quoted on Page 9 of Corcept’s July 2024 slide deck. While even 10,000 patients would be well below the Orphan Disease Act’s definition of “less than 200,000 people in the U.S.,” we understand that Corcept management will be in discussion with insurance payors well before it transitions out of “ultra-rare” and “rare” categories.

On the July 29, 2024 Q2 Conference Call, management stated “We know that each market has a price threshold, though, and the market with 2,000 patients is obviously different than one with 20,000 or 200,000. The hypercortisolism market is definitely still growing. And when we know where we’re at, our price will accurately reflect that market. And that’s our social contract.” We would estimate price reduction conversations will begin possibly as Corcept approaches a patient count of 10,000 or perhaps at 20,000, but these are very rough estimates and might begin after 2028 when we project only 5,480 Cushing’s patients in our financial models.

(4) On December 29, 2023 a New Jersey District Court ruled that Teva Pharmaceutical’s generic form of Corcept’s Korlym is not infringing on Corcept’s patents, allowing Teva to launch a generic form of Korlym, ostensibly opening the entire larger Cushing’s market to a generic manufacturer who could discount and take share. Corcept stated that they believe the “decision is based on legal and factual errors we are confident will be reversed on appeal,” so while Corcept may be able to reverse the genericization, Teva is currently in the market with its generic Korlym. In addition, on June 13, 2024, Teva also sued Corcept for anticompetitive conduct.

Given the above considerations, we are estimating that Corcept might be able to expand its served patients by about 10 times to 15,000 patients by 2033 compounding at a healthy 25% per year.

While Corcept’s Biggest Threat Is Teva’s Generic Korlym, We Believe Teva Will Find Generic Korlym Difficult to Sell and by H2 2025 Corcept’s New Cortisol Modulator Relacorilant Will Obsolete Korlym and its Generics

We believe litigation with Teva is likely to last well into next year and in the meantime it may not be so easy for Teva or any other generic manufacturers to enter the Cushing’s market. In fact, since January it appears Teva has not made much progress. Corcept said on its Q2 2024 conference call that “Teva’s generic product has been available in the channel for many months but it is having very little impact on our business.” This suggests that doctors and patients are happy with Corcept’s “high touch” field organization including clinical specialists, medical science liaisons and patient advocates, as well as a dedicated specialty pharmacy which is common for handling rare, high priced drugs that require customized fulfillment:

Commercial Capabilities Driving Korlym Business (Corcept)

Importantly, Corcept has developed a follow-on cortisol modulator Relacorilant which has been shown in a recently completed Phase 3 trial to have better efficacy and a far cleaner safety profile for Cushing’s than its current drug Korlym.

On its Q2 conference call Corcept indicated it will file for FDA approval for Relacorilant in the Q4 2024 and if approved as we believe, Relacorilant for Cushing’s could be on the market by late 2025, effectively rendering Korlym and any generics obsolete.

CATALYST #2 – A BETTER CORTISOL MODULATOR FOR CUSHING’S

Why Corcept’s New Drug Relacorilant Is Superior to Korlym, Is Likely to Obsolete Teva’s Generic Korlym and May Boost Corcept’s Long Term Peak Penetration of the Cushing’s TAM:

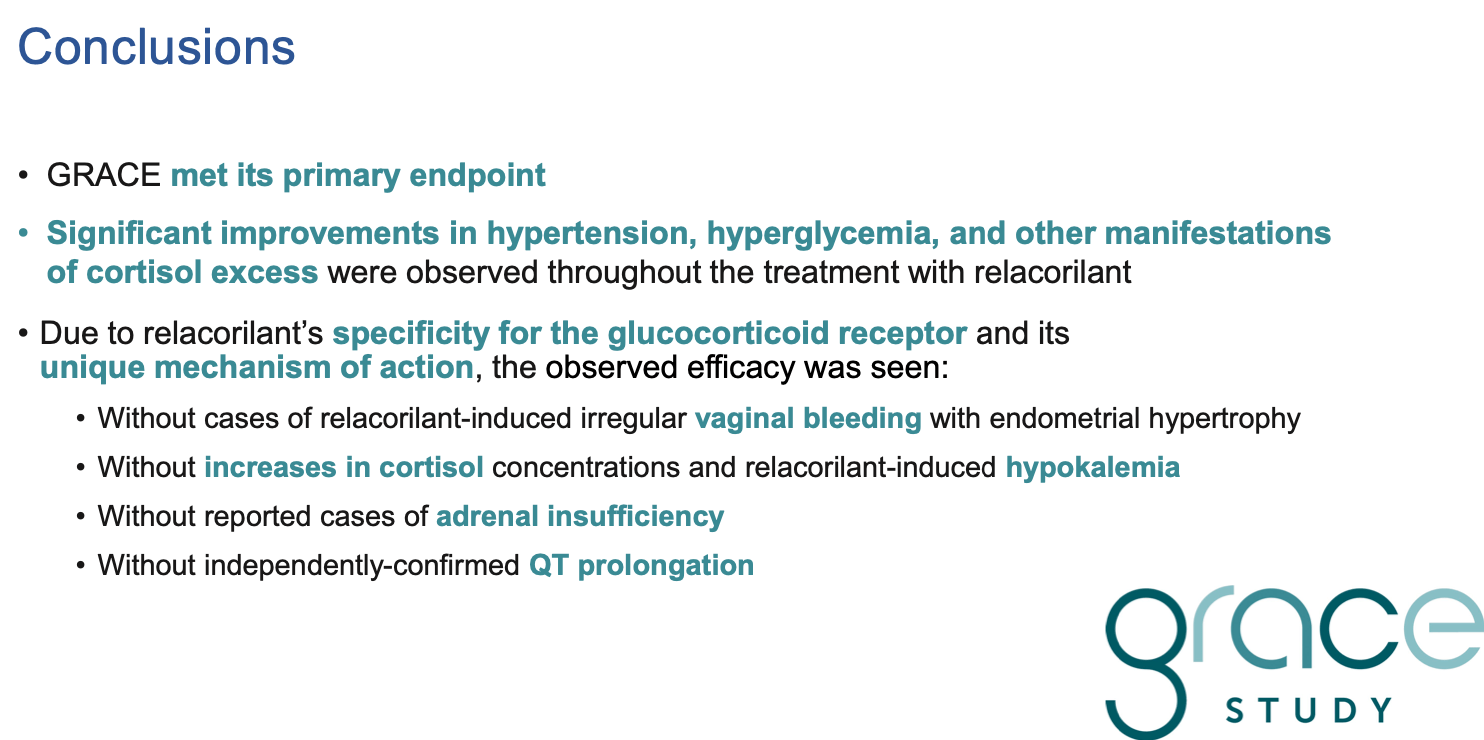

Corcept developed Relacorilant as a new cortisol modulating compound intending to replace Korlym and avoid its well-known side effects (explained earlier as the side effects of Mifepristone — vaginal bleeding, abortion, etc.). In addition to addressing Cushing’s syndrome and reducing hyperglycemia (diabetes) which Korlym can claim, Corcept hoped Relacorilant would reduce hypertension which Korlym is not able to claim. The Phase 3 trial confirmed reductions in both hyperglycemia and hypertension, as well as finding an important new safety benefit of avoiding Korlym’s hypokalemia:

- On May 28, 2024, Corcept announced Relacorilant’s “Phase 3 GRACE trial of Patients with Hypercortisolism (Cushing’s syndrome)” met its primary endpoints: “clinically meaningful and statistically significant improvements in hypertension, hyperglycemia and other symptoms experienced by patients with Cushing’s syndrome.”

- In its July 29, 2024 Q2 press release, Corcept elucidated that these “other symptoms” included improvements in “weight (loss), lean muscle mass, waist circumference (reduction), cognitive impairment and quality of life.”

- On June 7, 2024, Corcept presented its “Final Results of the Phase 3 GRACE Study” at the Heart in Diabetes Conference highlighting the superior safety benefits of Relacorilant vs. Korlym:

GRACE Trial Safety & Efficacy Superiority of Relacorilant vs. Korlym (Corcept)

Given the importance of a Relacorilant approved for Cushing’s we explain below why we believe it is superior to Korlym in both safety and efficacy which should lead to an FDA approval by H2 2025 and should obsolete Korlym and any generic Korlym thereafter:

- Relacorilant was found in the Phase 3 trial to reduce hypertension (high blood pressure), which should allow it to be placed on the label along with a claim that Relacorilant reduces hyperglycemia (diabetes). While Korlym does reduce hypertension for some people, it ironically increases hypertension for others, so the average hypertension response is not statistically significant for Korlym.

- Relacorilant fits inside and binds to the glucocorticoid receptor or GR, so it effectively blocks the effect of excess cortisol on the body’s organs, but unlike Korlym it does not fit inside the progesterone receptor so does not lead to vaginal bleeding, abortion, and other side effects of Korlym in Cushing’s patients. Over half of Cushing’s patients are female and some females and even some male patients and their doctors hesitate to use Korlym. They might well consider Relacorilant when approved.

- While Korlym succeeds in shutting off the GR cortisol receptor from the effects of excess cortisol, ironically for some patients the body can sense there is not enough cortisol and actually produces even more cortisol which can then cause hypokalemia (low potassium), arrhythmia and other side effects. However, Relacorilant was found in the clinical trials to NOT materially increase cortisol production and therefore not cause hypokalemia (N.B., lack of hypokalemia was unanticipated before the clinical trials so is a significant serendipitous benefit).

Commercially, we believe that with superior safety and efficacy Relacorilant will have greater receptivity by both doctors and patients, particularly females, and could result in a faster uptake, reach a higher peak penetration rate and benefit more patients than Korlym in a now much larger TAM.

CATALYST #3 – HOW CORCEPT “BROKE THE CODE” LAUNCHING A WAVE OF INNOVATIVE SOLUTIONS FOR MANY DIVERSE DISEASES

Cushing’s Syndrome Is Just the Beginning

The Corcept journey does not end with the now 60 times larger Cushing’s opportunity. A few years ago, Corcept scientists found a key to unlock the cortisol pathway that had eluded Major Pharma for decades.

It is critical to realize that the glucocorticoid receptor is in almost every cell in the body which gives the cortisol pathway very broad potential applications to many different organs of the body. Yet, despite cortisol being a major pathway Major Pharmaceutical companies were unsuccessful trying to develop cortisol modulators. Mifepristone (the abortion pill) was an early cortisol modulator and apparently 15 Major Pharmas assumed that all cortisol modulators had to be steroids which would have multiple deleterious side effects like mifepristone.

Corcept’s scientists also concluded that all steroids would interfere with other receptors beyond the intended receptor target and therefore would not be safe for drug development purposes. Instead, Corcept’s Head of Research found a ligand binder that fits in the cortisol receptor but is a little wider and does not fit into the progesterone receptor which is what causes Korlym’s side effects.

Corcept has since been able to find four different families of structures that still fit inside the cortisol receptor called the glucocorticoid receptor (“GR”) but not the progesterone receptor. Voila! Corcept found compounds that could block the GR and therefore impede the ability of the excess cortisol to access the body’s organs through the GR – but do not affect the body’s other receptors.

Since breaking the code to access the GR, Corcept has had an open field and has identified over 1000 cortisol modulators to investigate new solutions for numerous and diverse endocrine, oncologic, metabolic and neurologic disorders, many much larger than Cushing’s.

We believe that this treasure trove of over 1000 cortisol modulating compounds could become worth multiples of the value of Corcept’s Cushing’s franchise. We expect Corcept to be able to leverage its 25 years of domain expertise, leadership and extensive pipeline to transition from a one-product company into a larger, more diversified Platform Growth CompanyTM in the years ahead.

Corcept’s First Non-Cushing’s Candidates for Ovarian Cancer, ALS and MASH Will Have Key Announcements in the Next Few Months

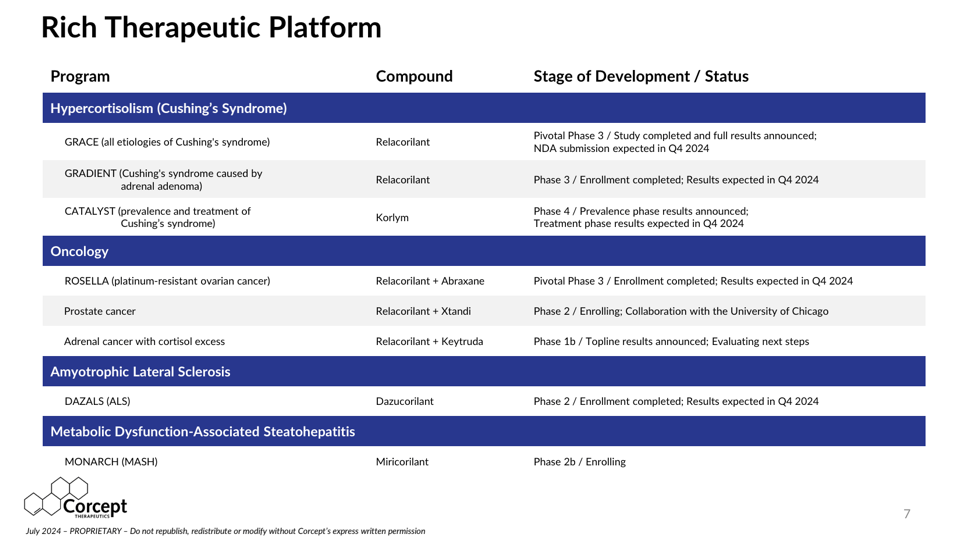

Corcept is advancing new Non-Cushing’s drug candidates for platinum-resistant ovarian cancer (Phase 3 results around the end of 2024), ALS (Phase 2 results by end of 2024), and MASH (Phase 2b enrolling), as well as 7 additional oncology, psychiatric and addiction disorders.

Below is a table from the July 2024 Corcept Investor Presentation showing their near term mid-to-late stage therapeutic platform:

Rich Therapeutic Platform (MId to Late stage Cortisol Modulating candidates)

Source: Corcept Therapeutics July 2024 Investor Presentation

By the end of this year Corcept’s announcements of data from Relacorilant’s Phase 3 trial for platinum-resistant ovarian cancer and Dazucorilant’s Phase 2 data for ALS will provide two important early indicators of the potential for Corcept’s rapidly expanding pipeline of Non-Cushing’s cortisol modulators targeting much larger markets than Cushing’s.

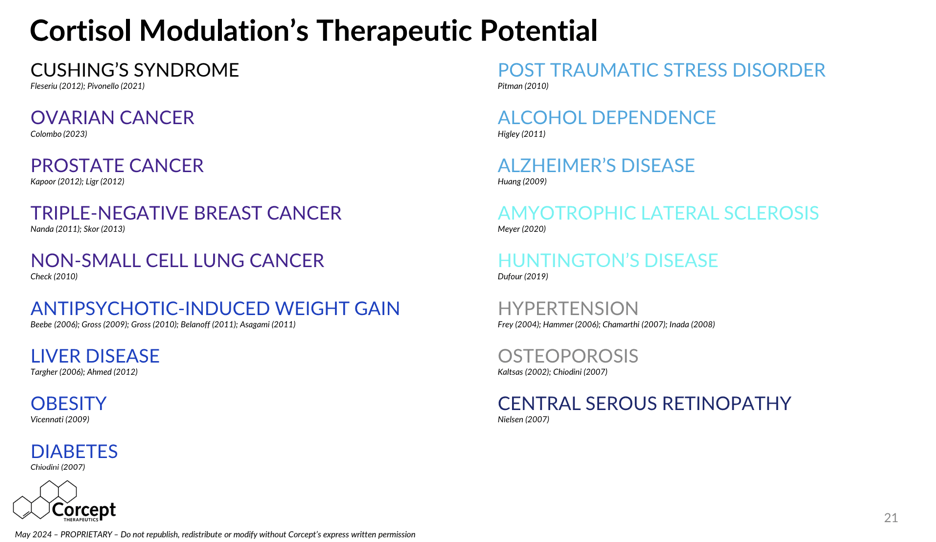

Corcept’s Therapeutic Long Term Pipeline of 1000 New Drug Candidates Is Novel and Unusually Diverse for a Midcap Biotechnology Company

Corcept’s July 2024 slide deck provides insight into the breadth and depth of therapeutic areas that Corcept believes it can address with cortisol modulators:

Therapeutic Areas for Cortisol Modulation (Corcept)

Source: Corcept Therapeutics July 2024 Investor Presentation

Corcept’s Important Phase 3 ROSELLA Trial for Platinum Resistant Ovarian Cancer Reads Out Data In Q4 2024

There are 34,000 treatable recurrent ovarian cancer patients in the U.S. with 22,000 platinum-resistant cases (resist first line therapies) and 13,000 die per year as estimated by Immunogen. On the July 29, 2024 Q2 conference call, Corcept Chief Development Officer Bill Guyer predicted that:

- “Relacorilant has the potential to become the standard of care for patients with platinum-resistant ovarian cancer. If our pivotal ROSELLA trial replicates the positive results from our large, controlled, Phase 2 study, it will constitute a major medical advance.

- We expect progression-free survival data, ROSELLA’s primary endpoint, by the end of the year.”

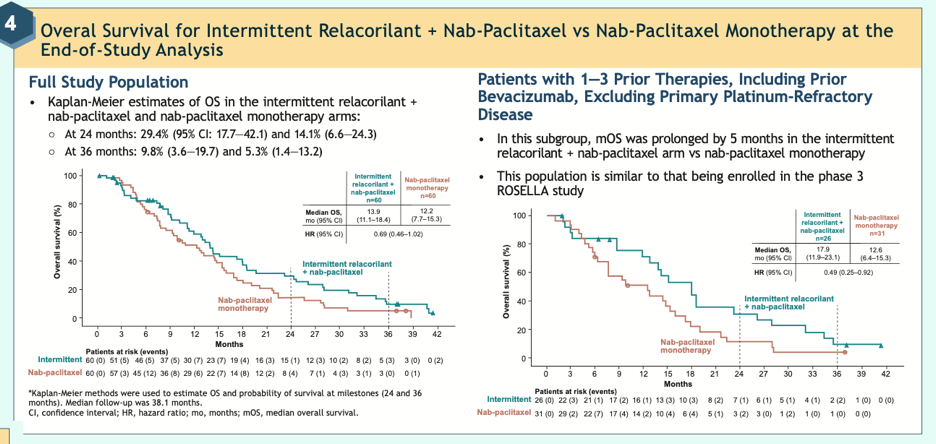

The results from the Phase 2 trial speak for themselves. As shown in the graphs below from a March 2024 poster presentation of the Final Overall Survival Data at the Society of Gynecological Oncology 2024 Congress, 29% of platinum-resistant ovarian cancer patients who took Relacorilant with Nab-Paclitaxel were alive after 24 months versus only 14% who took Nab-Paclitaxel alone. A doubling of Overall Survival rates would be material:

Overall Survival Rates for Relacorilant for Ovarian Cancer (Corcept)

Source: Corcept Website from poster: Final Overall Survival Data

Our financial model reflects a contribution to revenues from platinum-resistant ovarian cancer beginning with $11 million of revenue in late 2025. This assumes favorable confirmatory Phase 3 data by the end of this year, an NDA filing early in 2025 and an approval by Q4 2025.

While we still need to see favorable Phase 3 data by around yearend, given the severity of late stage ovarian cancer and the favorable Phase 2 data, we are projecting strong revenue contributions of $162 million in 2026 and $348 million in 2027. While we believe Relacorilant could be beneficial for boosting standard chemotherapies in earlier stages of ovarian cancer therapy, FDA approvals for use in earlier lines of treatment might take 1-2 years so we will have to wait to embed them in our forecasts.

Corcept’s Phase 2 DAZALS Trial for Dazucorilant for ALS Reads Out Data In Q4 2024,

- In an April 15, 2024 press release Corcept stated “Dazucorilant animal studies for ALS showed great promise in an animal model of ALS – improving motor performance and reducing neuroinflammation and muscular atrophy…There is increasing evidence that patients with ALS exhibit elevated or abnormal cortisol levels, particularly those with rapid disease progression.”

ALS affects 25,000 in the U.S. and we are looking forward to seeing Phase 2 data on 249 ALS patients in Q4 2024. If Dazucorilant’s Phase 2 results are favorable, Corcept could get accelerated approval and be on the market in late 2025. However, given the risky clinical leap from animal studies to human Phase 2 data, it is best to wait for trial results before we make any financial estimates.

Corcept’s Phase 2b MONARCH Study for Miricorilant for MASH Is Currently Enrolling

On the July 29, 2024 Q2 conference call, Corcept stated during its Phase 1b trial of Miricorilant for MASH (“fatty liver disease”) that:

- “Liver fat was reduced by 30% and there were improvements in metabolic and lipid measures. MASH is a serious liver disease that affects millions of patients in the U.S…Cortisol activity has been implicated in the development and progression of the disease.” MASH (Metabolic Dysfunction-Associated Steatohepatitis) was formerly called NASH.

We could make upside additions to our Corcept Revenue and Earnings Model for Dazucorilant for ALS and/or Miricorilant for MASH based on results from their Phase 2 trials in the next few months.

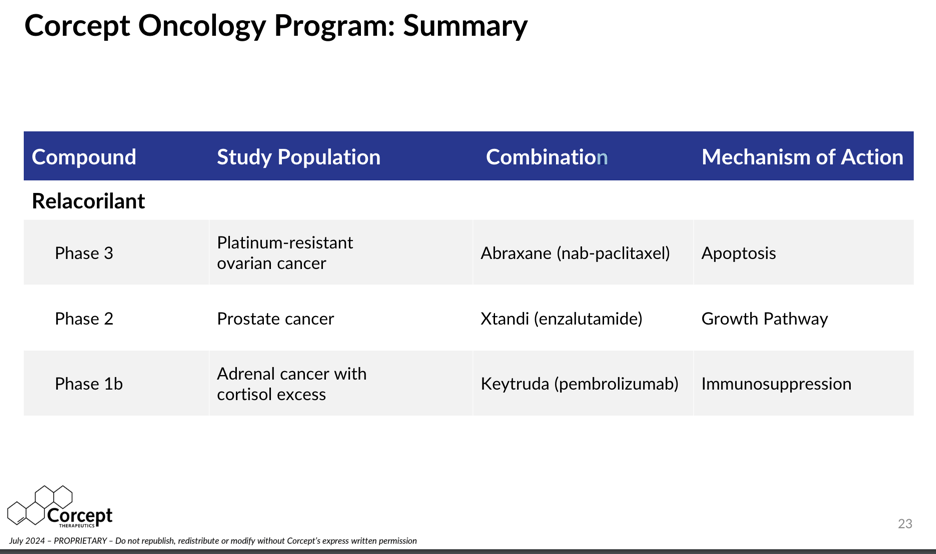

Combo Therapy to “Make Chemo Better” – Corcept’s Cortisol Modulators Can Boost the Effectiveness of Many Existing Anti-Cancer Therapies Using 3 Different “Mechanisms of Action” Providing New Opportunities to Treat Many Different Cancers

While it is financially appealing to begin to understand that cortisol modulators can take on a surprisingly oversized role in defeating cancer, what is intriguing is “why.” Over many years studying the stress hormone cortisol, Corcept has learned how cortisol can actually protect cancer cells.

So far, Corcept has discovered three different ”mechanisms of action” by which cortisol can protect cancer cells and make it more difficult for anti-cancer agents to maintain effectiveness in fighting and killing cancer cells. As listed in the right column of the table below, these three mechanisms are:

- “Apoptosis” – Cortisol is anti-apoptotic (prevents cancer cell death);

- “Growth pathway” – Cortisol provides a pathway for tumors to grow following anti-androgen therapy;

- “Immunosuppression” – Cortisol suppresses the body’s natural immune system that is trying to kill the cancer cells.

Corcept Oncology Program (Corcept)

Source: Corcept Therapeutics July 2024 Investor Presentation

As shown in the table above, Corcept is using Relacorilant in combination with 3 different existing already approved multi-billion dollar cancer therapies expecting to boost their overall efficacy by reducing the protective effects of cortisol on cancer cells.

The first example is the use of Relacorilant for platinum-resistant ovarian cancer which we have already highlighted as reporting key Phase 3 data by yearend. In essence, by modulating the effects of cortisol, Relacorilant is reducing the cancer cells’ increasing resistance to Abraxane resulting from the presence of cortisol.

If Corcept is successful in establishing the efficacy of Relacorilant in preserving and boosting the performance of anti-cancer agents for ovarian cancer, prostate cancer or adrenal cancer with cortisol excess, we believe it will create many more opportunities for Corcept to pair some of its other cortisol modulators with many other anti-cancer agents.

FINANCIAL FORECASTS

With the compounding of 3 dynamic growth catalysts, the forecasting “degree of difficulty” is challenging.

With a 60 times expansion of the TAM (Total Available Market) for the treatable Cushing’s population, it is very difficult to predict the ramp of patient count, revenue growth rates and the long term maximum penetration rate, particularly for entering a newly discovered market.

The degree of difficulty is compounded by an expected introduction next year of Relacorilant, a new replacement product that is far safer than its current product and we believe could multiply revenues even without an increase in the TAM.

At the same time, it is also difficult to accurately time and size the layering on of revenues and earnings from Corcept’s cortisol modulators for ovarian cancer and other serious Non-Cushing’sdiseases. Success in any of these first candidates could add very significant revenues and earnings for a company that reported $482 million in revenues last year. The first Non-Cushing’s revenues could start in the 4th quarter of 2025 for platinum-resistant ovarian cancer.

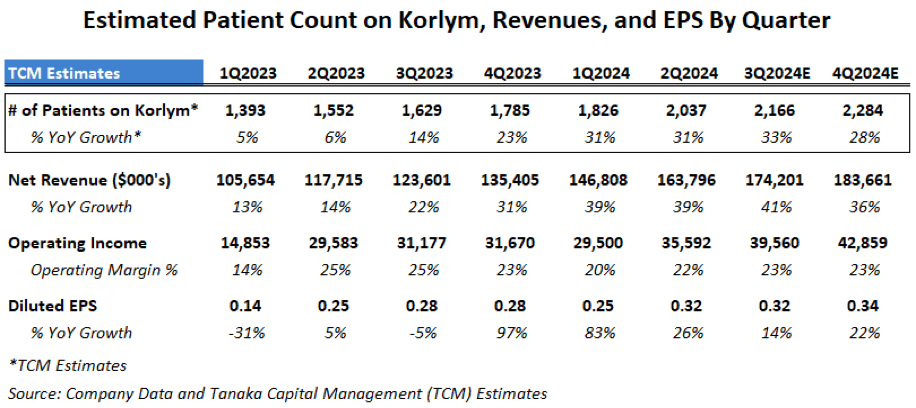

Q3 and Q4 2024 Could Well Maintain Recent Reacceleration of Growth

Even before the landmark DTT Type 2 Prevalence Study was published in February 2024, Corcept’s Korlym year-to-year patient count had already began to reaccelerate starting in Q3 and Q4 2023:

Estimated Cushing’s Patient Count, Revenues and EPS by Quarter (Tanaka Capital Management)

As mentioned previously, revenue growth was suppressed in 2020-2022 due to Covid preventing doctor visits by patients and sales reps, so we were not surprised to see some rebound in 2023 off depressed levels. However, during its February 15, 2024 Q4 2023 conference call management attributed much of the acceleration to investments Corcept had made in its salesforce, education and from improving doctor prescription trends:

- “The biggest factor is that we have more physicians prescribing Korlym and more patients prescribed per physician, driven by improving field execution and early returns we have made on disease education. We are currently at 70 specialists and we are continuing to add. The target is around 100 and unlikely to stop there. More doctors are prescribing and more patients from each doctor.

- This trend got really strong towards the end of last year and we are seeing that continue.”

On July 29, 2024, Corcept reported Q2 earnings of $0.32/share, up 28% vs. $0.25 last year and beat Wall Street estimates of $0.23/share by a surprising 39%. Q2 revenues came in at $163 million, up 39% versus a year ago and Corcept raised its 2024 full year revenue guidance by $20 million to $640-670 million (up 32-39% vs. 2023). Cash and investments rose in the First Half by $67 million to $492 million.

On the Q2 conference call, management stated that they have not yet begun to see much effect on sales from the February announcement of the Prevalence Study which was frankly a little surprising to us:

- “The reality is that there has been little to no impact from CATALYST (the Prevalence Study) in our results and we don’t embed much of an impact in guidance.

- I do think the results that we presented will be more meaningful over time and we could see more patients than initially expected in the second half.”

We believe this suggests potential for our already optimistic estimates for 2024 patient count, revenue and earnings to be met or exceeded.

We will be watching to see if Corcept can indeed “see more patients than initially expected in the second half” as the salesforce will be using the results of the Prevalence Study to encourage doctors to do more testing for hypercortisolism.

WE EXPECT CONTINUED RAPID GROWTH IN THE NEXT 5 YEARS:

From 2023 to 2028 Corcept Could Grow Revenues 37%/year and EPS 56%/year

Early in this article we showed how Corcept’s revenues grew at a 47%/year compound growth rate in the last 10 years but that growth had slowed dramatically in the 2020-2022 Covid years when the salesforce and patients couldn’t visit their doctors.

We believe that Corcept revenues can return to strong 37%/year compound annual growth rate in the next 5 years as it benefits from a much larger Cushing’s TAM, it delivers a much safer and more effective Relacorilant cortisol modulator for Cushing’s and it begins to introduce novel cortisol modulators to new Non-Cushing’s therapeutic areas.

Our 5-year 2023-2028 projections assume 25-30%/year growth in number of Cushing’s patients treated even though it is quite conceivable that Corcept can grow at a faster rate as it rolls out into the under-penetrated Difficult-To-Treat Type 2 diabetes candidate population. At the same time Corcept could be layering on potentially large revenue and earnings contributions from additional Non-Cushing’s cortisol modulators should they have successful clinical trials, but we have only included our estimates for platinum-resistant ovarian cancer.

Over the Next 5 Years, We Estimate Operating Margins Will Recover and Expand Significantly as Revenues Grow Faster than Operating Expenses

Operating margins declined during the Covid-impacted years from 28% in 2022 to 22% in 2024 as Corcept opted to continue investing heavily in clinical trials and sales force expansion.

In 2025 and 2026, we expect Corcept should begin to see a return on those heavy investments, with revenues growing faster than expenses and operating margins rebounding from 22% in 2024 to approximately 31% in 2025, moving even higher in 2026, 2027 and to an estimated record high of 55% in 2028:

Corcept 5-Year EPS Model (Tanaka Capital Management)

Note that our EPS estimates of $1.23 and $2.11 for 2024 and 2025 are more optimistic than the Wall Street Sell Side estimates of $1.11 and $1.69 on revenue estimates averaging $658 million (+36.5%) and $778 million (+18.2%) for 2024 and 2025 according to Yahoo Finance. We believe that the 5 Sell Side analysts are being understandably cautious given Teva’s generic entry and waiting to see if Corcept can penetrate the new Difficult-To-Treat Type 2 diabetes market.

The Rising Importance of Non-Cushing’s Revenues and Earnings

As shown in the bottom line in our 5-Year Earnings Model above, we expect Non-Cushing’s activities (ovarian cancer) to act as a drag of ($0.10)/share on EPS in 2025 due to start-up costs but transition to contribute $0.49 to EPS in 2026, $1.29 in 2027 and $2.08 EPS of our estimate of $8.86 EPS in 2028.

This underscores how important it will be that Corcept reports favorable confirmatory results for its Phase 3 trial for Relacorilant for platinum-resistant ovarian cancer at the end of this year, is approved by the FDA and begins to generate revenues in H2 2025.

Beyond 2028, we expect that Non-Cushing’s cortisol modulators could become a multi-billion dollar business segment complementing what we expect to be a multi-billion dollar Cushing’s business segment in years 2028-2033. However, we believe it is too early to put numbers on the 2028-2033 period with so many moving parts to Corcept’s rapidly evolving business model.

VALUATION AND $133 PRICE TARGET

We Believe Corcept Is Significantly Undervalued Given Its 3 Catalysts and What Could Be Decades of Strong Growth in Both Cushing’s and for Non-Cushing’s Cortisol Modulators for Many Diseases.

At $35.71/share, Corcept (CORT) is valued at 28.8 and 16.9 times our EPS estimates of $1.24 in 2024 and $2.11/share in 2025 on revenues estimates of $668 million and $905 million, respectively.

Beyond 2025, we project annual EPS growth rates of 40%+ to 2028 with the potential for continued strong double digit growth beyond 2028 powered by its 3 growth catalysts:

- Catalyst #1: From 2023-2028, with the expansion of the TAM for Cushing’s syndrome, to 600,000 patients we estimate that Corcept has the potential to grow its served Cushing’s patients about 28%/year from an average of 1590 in 2023 to approximately 5480 patients in 2028. This would grow Cushing’s revenues by 31%/year from $482 million in 2023 to about $1.9 billion in 2028. With operating leverage and rising margins, we estimate GAAP EPS from Cushing’s alone could grow 48%/year from $0.94 in 2023 to $6.78/share in 2028.

- Catalyst #2: Relacorilant for Cushing’s with its much more favorable safety profile has the potential to continue to fuel strong double digit growth in Cushing’s revenues as it replaces Korlym and enables Corcept to reach our projection of a 10 times increase in Cushing’s revenues over the next 10 years to 2033. We believe Relacorilant is capable of elevating Corcept’s long term maximum penetration rate of the Cushing’s market to multiples of what it would have been with Korlym. Near term, we need to see if doctors increase testing for hypercortisolism and if doctor and patient responses become more positive with a safer drug and extend Corcept’s runway to 10,000s or more patients out of the 600,000 TAM.

- Catalyst #3: We estimate the addition of Relacorilant for ovarian cancer could boost Corcept’s total company revenues to $2.39 billion in 2028 for a 5-year revenue growth rate of 37%/year and boost EPS to $8.86 in 2028 for a 5-year total company EPS growth rate of 56%/year. While these include our current estimates for ovarian cancer, we wouldn’t be surprised if we have to raise our long term total company EPS forecasts for additional Non-Cushing’s cortisol modulators should Corcept report favorable results in its trails for ALS, MASH or other diseases beginning in the next few quarters.

With these growth rates and the potential for continued strong double digit growth beyond 2028, we believe that in 3 years (2027) Corcept could conservatively command a P/E ratio of 15 times our forward 2028 EPS of $8.86/share for a target price of $133 which would deliver a compound return of 55%/year.

RISKS

1. Generic competition from Teva or others: We discussed the difficulty for Teva to enter the high touch Cushing’s syndrome market. In addition, with the TAM 60 times larger, there will be significant opportunity for Corcept to grow with or without competition, and then Corcept should have a commanding position if Relacorilant is approved for Cushing’s as we believe in 2025.

2. If Relacorilant for Cushing’s is not approved or is delayed by the FDA: We believe Relacorilant will be approved for Cushing’s given that the primary endpoints for efficacy and safety were met in the Phase 3 GRACE trial reported in May. In addition, Corcept has been in communication with the FDA and in July volunteered to delay its NDA filing from Q3 to Q4 of 2024 as the FDA suggested waiting to see the results of Corcept’s 2nd Phase 3 trial called GRADIENT focusing on Relacorilant for patients with adrenal adenomas known to be a primary cause of Cushing’s. Corcept is confident that the results of this additional Phase 3 GRADIENT trial will bolster its NDA package for Relacorilant for Cushing’s, which we assume would broaden and strengthen the label on what Corcept can claim for efficacy and safety.

3. If results from the ROSELLA Phase 3 trial for Relacorilant for platinum-resistant ovarian cancer do not replicate the results from the Phase 2 study which showed a doubling of overall survival at 24 months. We are confident that efficacy will be replicated.

4. Management could decide to accelerate spending in 2025 and 2026 and hire even more sales people for Cushing’s if it sees a greater than expected market opportunity. It could also accelerate spending on hiring for a bigger than expected launch of Relacorilant for platinum-resistant ovarian cancer and could also boost R&D and SG&A to develop and launch more new drugs from its pipeline which could temporarily impact profitability. We would regard these as timing differences that would lead to faster revenue and earnings growth in 2027 and 2028.

5. It may be more difficult than expected to educate and persuade the 268,000 primary care doctors in the U.S. to test their non-responding Type 2 diabetic patients for hypercortisolism (Cushing’s) than the smaller group of endocrinologists that Corcept has been contacting for years. However, given Corcept’s success with endocrinologists, we anticipate Corcept to be able to leverage its prevalence data to persuade endocrinologists to test more of their patients and encourage primary care physicians to begin testing.

6. Corcept may be forced to implement greater price cuts to Korlym and Relacorilant for Cushing’s earlier than expected if it evolves to be considered in a larger class than a rare orphan disease. Every insurer has approved Korlym in the past and we expect management to remain on good terms with insurers.

7. A competing cortisol modulator or reducer could be developed for Cushing’s. Corcept has spent over a decade accumulating intellectual property and identifying over 1000 cortisol modulators making it difficult for a competitor to develop another that is safe and more effective. Sparrow Pharmaceuticals has released interim Phase 2 results from small trials seeking intracellular reduction of cortisol but will need larger trials. It took Corcept almost 6 years to prepare and run Phase 3 trails for Relacorilant and in a few years we believe Corcept will have established Relacorilant as the standard therapy for non-surgical treatment of Cushing’s.

Corcept Can Become a Generational “Platform Growth CompanyTM”

Over the years we have endeavored to find companies building proprietary platforms upon which they can add a series of new products and services to grow year after year. Our philosophy is to do a lot of original research early to be able to find an undiscovered Platform Growth Company,TM benefit from the addition of each new product or service and realize attractive compound returns over many years.

I was the first Buy Side analyst to visit Tesla in 2013 and believe that Corcept today might have the same potential to transform great science into making the world a better place while providing multiple years of upside for investors. We first bought Corcept in 2016 when it had only one dominant product but had the domain expertise and scientific potential for introducing other cortisol modulators to address many different disorders.

We are now more confident that Corcept could become one of the next great Platform Growth CompaniesTM with years or possibly decades of potential growth from multiple new products ahead. If you are interested in our individual portfolio management services or our award winning mutual fund, please go to Tanaka Capital Management.

—————————————————————————————-

I wish to thank my partner, Benjamin Bratt, for his advice and for constructing the financial models.

Disclosure: I am/we are long CORT. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.