Smederevac

When you really think about it, the food distribution market, it’s fascinating. The logistics networks that need to be built in order to facilitate the transportation of $2.39 trillion worth of food, just for the US alone, to over 330 million people, must be massive and efficient. This is especially true when you consider the short shelf life that so much of the food that we consume has. One of the companies that operates in this amazing space that is integral to the existence of the modern world is The Chefs’ Warehouse (NASDAQ:CHEF).

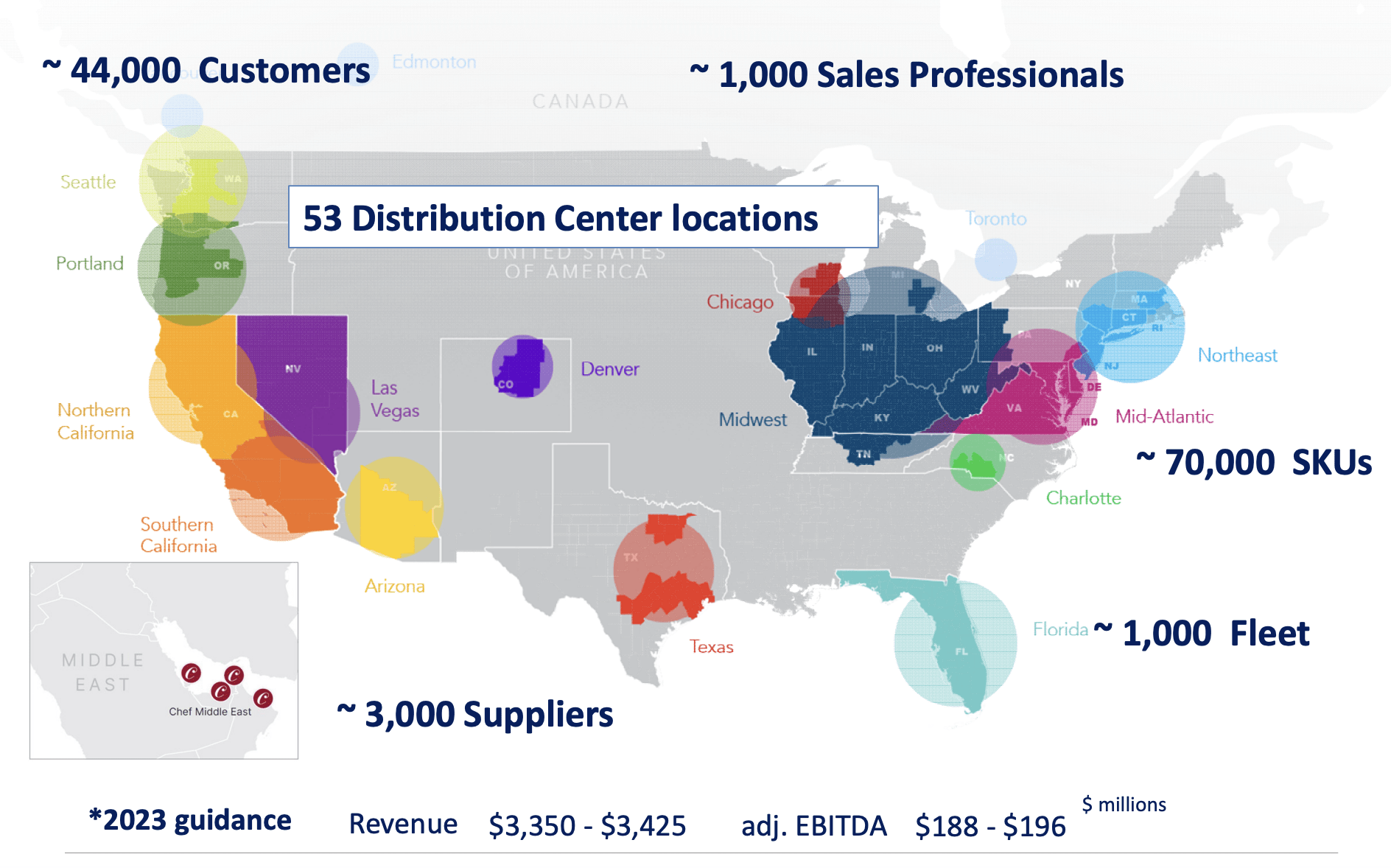

With a market capitalization right now of $1.56 billion, the company is not exactly big itself. But it does have a big reach. Using roughly 3,000 suppliers and its 53 distribution centers located across the most heavily populated portions of the country, it distributes around 70,000 SKUs worth of products to approximately 44,000 customers. These are overwhelmingly customers and the foodservice space. Examples include restaurants, country clubs, hotels, culinary schools, bakeries, chocolatiers, cruise lines, and more.

The Chefs’ Warehouse

Back in February of this year, I decided to revisit the company after having previously rated it a ‘buy’. At that time, the company had just announced strong results covering the final quarter of its 2023 fiscal year. And because of that strong performance, combined with expectations for the future and how shares were priced, I maintained that the ‘buy’ rating for the stock should still hold. Since then, shares have underperformed the market, climbing by only 6.3% while the S&P 500 is up 11.8%. While this is disappointing, I would make the case that this just means that investors have had an extended period during which they can snatch shares up.

Still a logical play

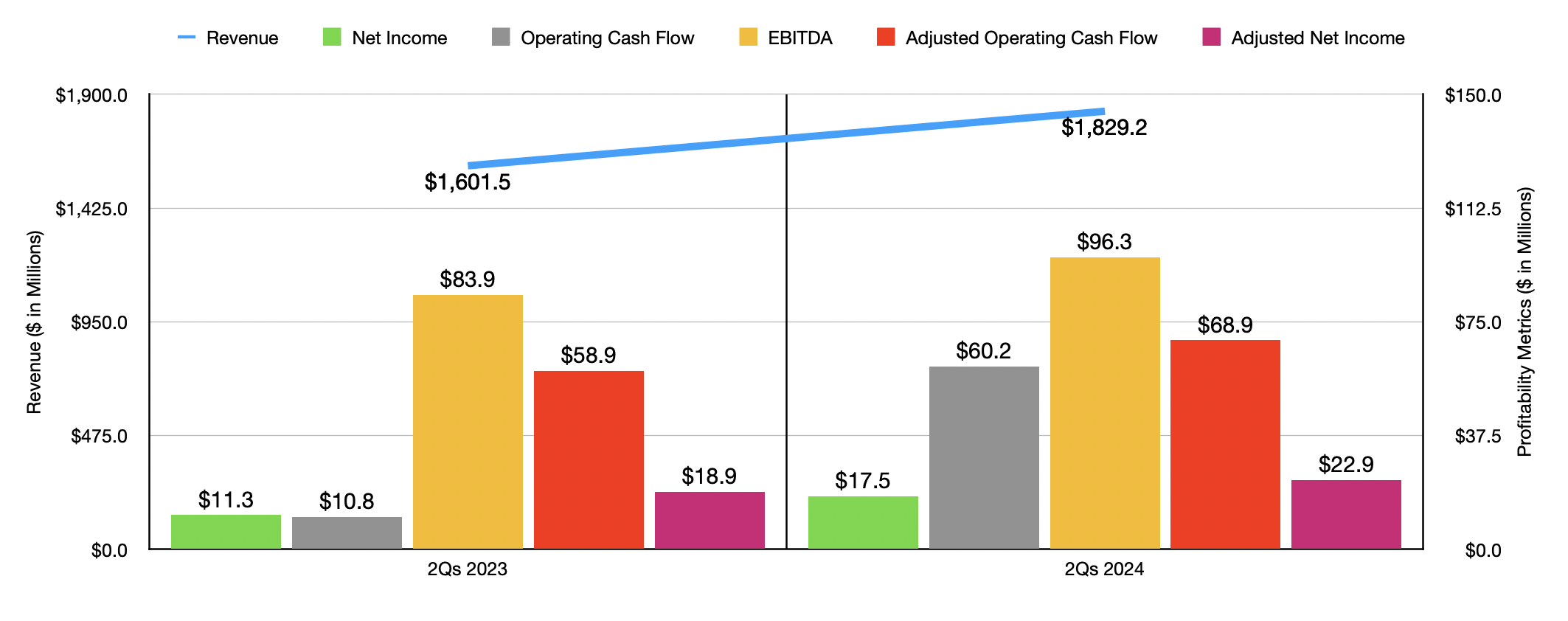

Since I last wrote about The Chefs’ Warehouse earlier this year, management has come out with results covering two additional fiscal quarters. During that time, revenue totaled $1.83 billion. This represents an increase of 14.2% compared to the $1.60 billion the company generated just one year earlier. Organic growth was a heavy lifter during this time, adding $126.2 million, or 7.9%, to the company’s top line. The other 6.3% improvement was attributable to acquisitions that the company had made. Organically, case count jumped 4.7% in its specialty category of products. The company also benefited from a 9.1% rise in specialty unique customers and an 11.6% surge in placements. For its center-of-the-plate category, organic pounds that the company sold rose by 4.5%. And when it comes to product price inflation, the company benefited to the tune of 2.1% in the specialty category and 4.5% in its center-of-the-plate category.

Author – SEC EDGAR Data

With revenue rising, profitability for the company improved also. Net income leaped from $11.3 million to $17.5 million. Obviously, the rising sales helped the company. But there were other contributors as well. Most notably, the firm’s gross profit margin expanded from 23.6% to 24%. Higher volume, combined with price increases, ended up being responsible for this. Other profitability metrics followed a very similar path. Adjusted net income grew from $18.9 million to $22.9 million. Operating cash flow skyrocketed from $10.8 million to $60.2 million. However, if we adjust for changes in working capital, we get a more modest, but still impressive, improvement from $58.9 million to $68.9 million. And finally, EBITDA for the company increased from $83.9 million to $96.3 million.

Author – SEC EDGAR Data

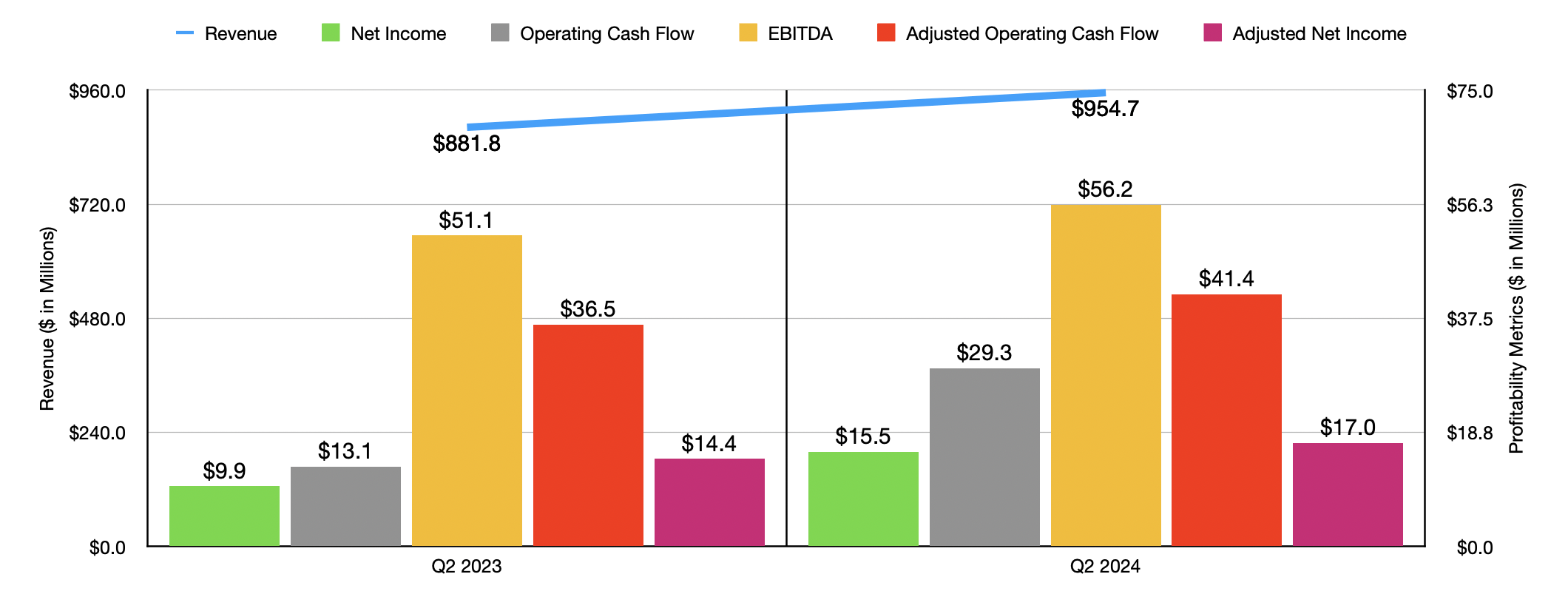

Given the economic uncertainty that we are dealing with at this point in time, it would be understandable for investors to be worried about potential changes in fundamentals. Because of this, looking at just the most recent quarter on its own is probably important. In the chart above, you can see those results. It is true that growth has slowed, with sales up only 8.3% on a year-over-year basis. However, organic growth was still a very strong 7.2%. This is not as impressive as the 7.9% seen for the first half of this year as a whole. But it is nice to see that it was the acquisition side of things, adding only 1.1% to the top line, that was responsible for this slowdown. Naturally, profits and cash flows are up year over year without exception. So that is also excellent to see.

For the rest of this year, management seems quite optimistic. Their most recent guidance calls for revenue of between $3.665 billion and $3.785 billion this year. At the midpoint, this would be 8.5% above what the company saw last year. It’s also higher than the previous expected midpoint by 0.3%. It’s always great to see management increase guidance instead of lower it. The company also expects EBITDA of between $208 million and $219 million. We don’t have estimates when it comes to other profitability metrics. But if we assume that they will increase at the same rate that EBITDA it’s expected to at the midpoint, we would expect adjusted net profits of $57.9 million and adjusted operating cash flow of $151.2 million.

Author – SEC EDGAR Data

Using these figures, I was able to value the company in the chart above. The chart values the company based on forward estimates for this year and historical figures from last year. On a price to earnings basis, I would say that shares are quite lofty. But they are marginally attractively priced when it comes to the other profitability metrics. Relative to similar firms, this is not exactly the case. In the table below, I compared it to five comparable businesses. On a price to earnings basis, three of the five companies ended up being cheaper than it. This number rises to four of the five on a price to operating cash flow basis, but drops to two of the five on an EV to EBITDA basis. So in this regard, The Chefs’ Warehouse is more or less in the middle of the pack.

| Company | Price / Earnings | Price / Operating Cash Flow | EV / EBITDA |

| The Chefs’ Warehouse | 26.9 | 10.3 | 10.5 |

| The Andersons (ANDE) | 16.4 | 2.1 | 5.5 |

| SpartanNash Company (SPTN) | 16.2 | 4.3 | 6.2 |

| United Natural Foods (UNFI) | 40.6 | 2.8 | 11.6 |

| US Foods Holding Corp. (USFD) | 27.4 | 12.9 | 13.1 |

| Performance Food Group Company (PFGC) | 26.2 | 9.8 | 10.6 |

Even though management seems optimistic about this year, I can understand any hesitancy that investors might have. After all, there has been a lot in the news recently about the pushback from consumers regarding higher prices at restaurants. 82% of US restaurant operators increased their menu prices in 2023. And even though inflation is down to multi-year lows, inflation still means price increases will occur moving forward. This should prove particularly painful for the customers that The Chefs’ Warehouse has, since its emphasis is on catering to independent operators. And by definition, independent restaurant operators will have lower margins already than large conglomerates.

Author – USDA Data

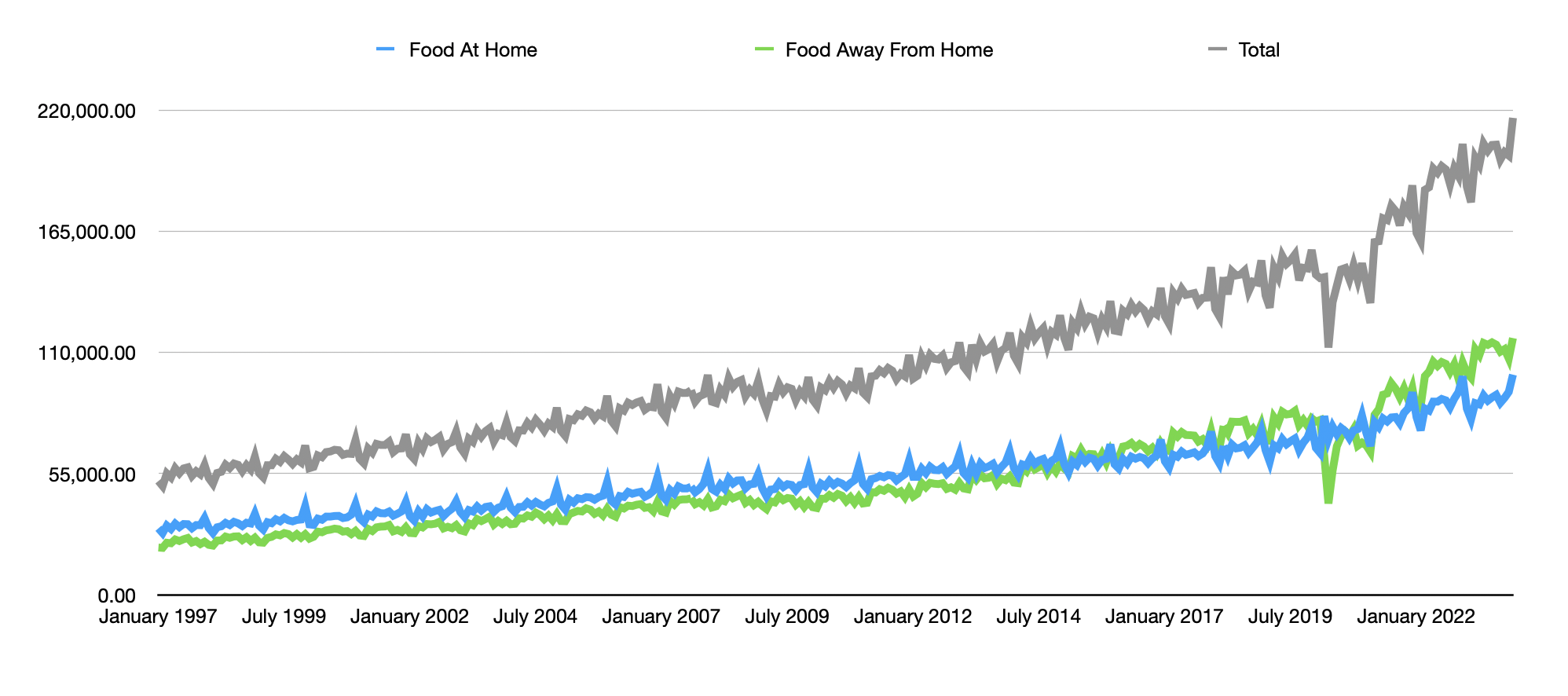

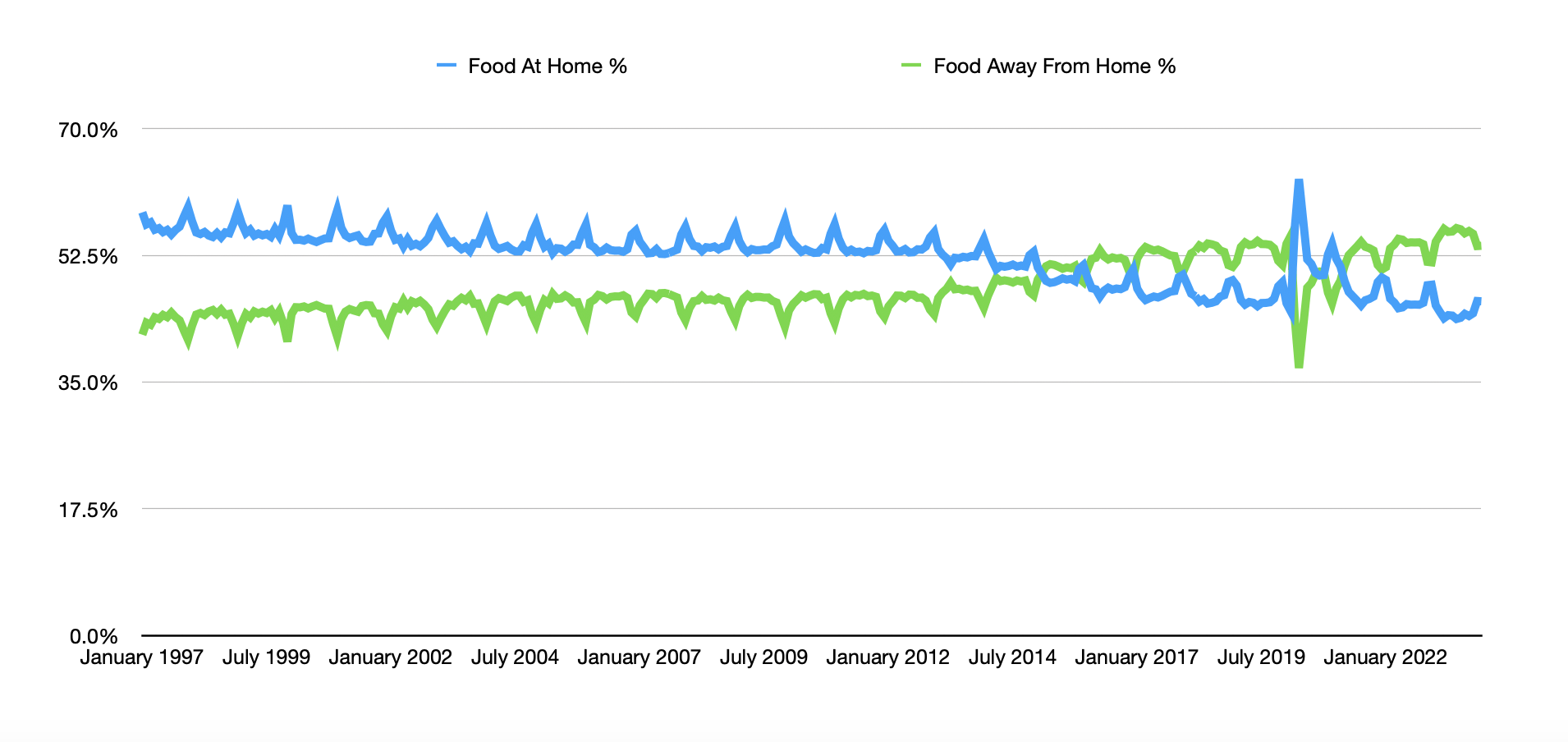

I don’t deny that there could be some short-term impact. But the good news, as the chart above illustrates and as the chart below also illustrates, is that there has been a consistent shift over the past couple of decades away from people spending money for food at home and toward them spending money for food away from home. Food away from home might be more expensive, but it is fast and convenient. And in a fast-moving world, this trade off makes a lot of sense for a lot of people. I know, in many cases, it does for me. So while the company might see some pushback at some point, I firmly believe that the long-term picture will be favorable for it.

Author – USDA Data

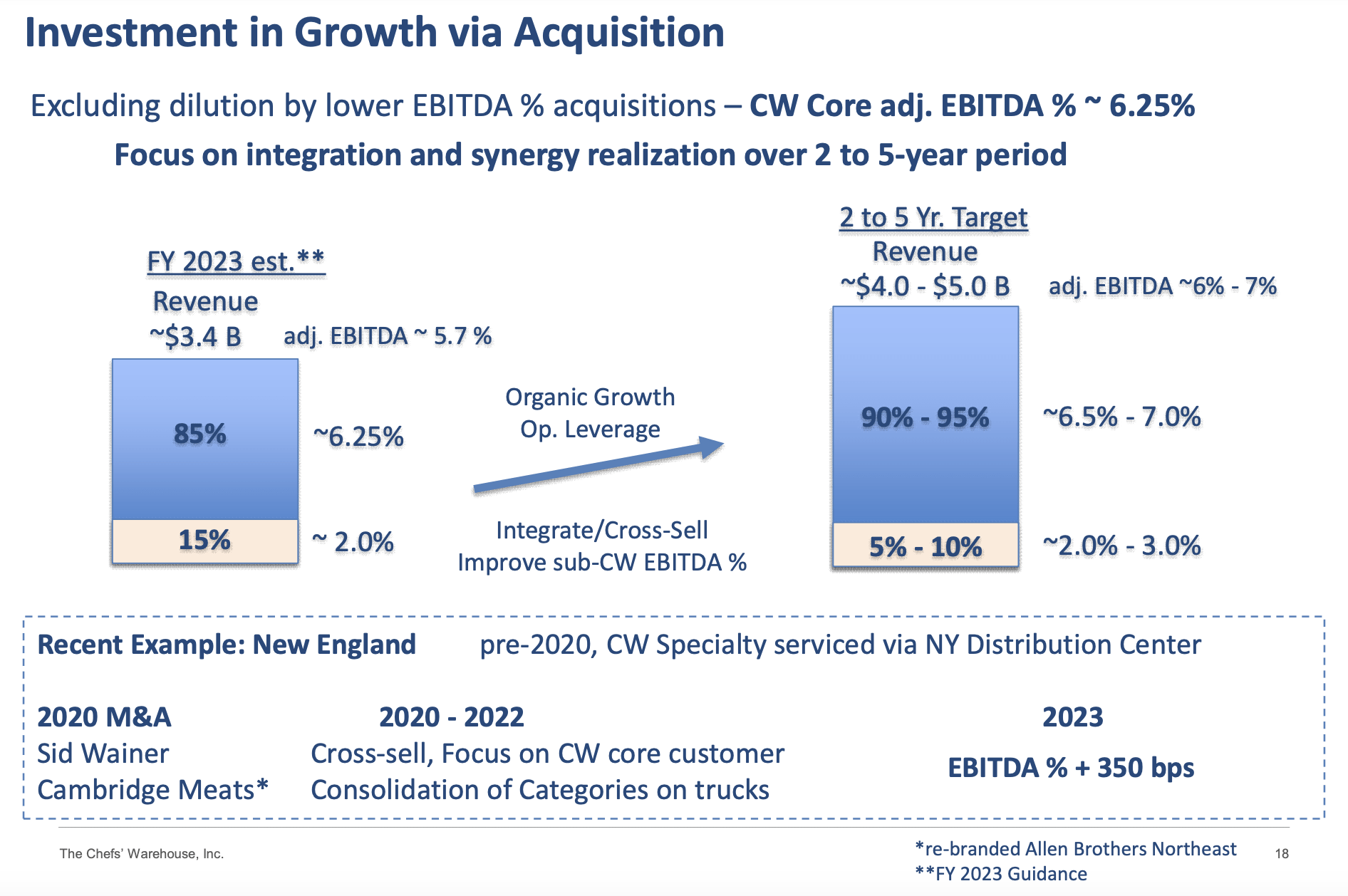

Speaking of the long run, management continues to make investments in order to achieve their objectives. In addition to making acquisitions, the company continues to invest in expanding its physical footprint from an organic perspective. The current plan is for the company to grow its physical capacity by about 490,000 square feet between this year and the end of 2026. This, combined with additional acquisitions that the company will doubtlessly make, will help to push it toward its target of between $4 billion and $5 billion in revenue between 2025 and 2028. And as the company scales revenue higher, margins are also expected to improve.

We are talking about a low margin space, so investors should not anticipate anything crazy. In 2023, the company’s EBITDA margin ended up being 5.63%. By the time the company hits between $4 billion and $5 billion in revenue, it expects this number to grow to between 6% and 7%. Even hitting the midpoint here with revenue of $4.5 billion and an EBITDA margin of 6.5%, would mean an extra $39.2 million in annual profit compared to if the firm hits that revenue target but keeps its EBITDA margin unchanged from what was seen in 2023.

The Chefs’ Warehouse

Obviously, management has provided us with a wide range of options here. But I did do a little experimentation. If the firm hits the low end of its targets, we would be looking at annual EBITDA of $240 million. The high end would give us $350 million. At the midpoint, we are looking at $295 million. If the company hits this midpoint of guidance, and it trades at the same EV to EBITDA multiple that it trades at today, that would translate to an upside of 55%. That would be about 10.2% on an annualized basis if the company takes five years to achieve that goal. This is roughly in line with what the broader market achieves over the long run. At the higher end, we would be looking at 15.6% annually, or 92.1% total, during this window of time. And again, this assumes that the company takes a full five years from the end of 2023 in order to hit the subjective. With revenue already nearing the $4 billion mark by the end of this year, I would be surprised if the firm doesn’t hit $4 billion next year.

Takeaway

Fundamentally speaking, The Chefs’ Warehouse is doing quite well for itself. The company is growing nicely, both on its top and bottom lines. Shares aren’t the cheapest, but a view of the future, even a conservative one, indicates that some attractive upside can be captured by investors. Given all of this, and the trends that work in the company’s favor in the long run, I have no problem keeping it rated a soft ‘buy’ for now.