koto_feja

Checkpoint Therapeutics, Inc. (NASDAQ:CKPT) focuses on targeted immunotherapies for solid tumors. The company’s flagship drug candidate is Cosibelimab, a novel anti-PD-L1 antibody currently under FDA review for treating cutaneous squamous cell carcinoma [cSCC] as a single-agent therapy. Cosibelimab could potentially have indications for metastatic cSCC and locally advanced cSCC. Additionally, it has a dual mechanism of action with NK cells that gives it a theoretical edge over other PD-L1 inhibitors. So, if Cosibelimab is approved by December 2024, CKPT could become a major player in cSCC. Despite the inherent regulatory risks and cash runway concerns, I think CKPT is a viable speculative “buy.” Yet, it’s undoubtedly a high-risk, high-reward stock, so investors should size their positions accordingly.

Cosibelimab: Business Overview

Checkpoint Therapeutics is a clinical-stage biopharmaceutical company based in Waltham, Massachusetts. Founded in 2014, the company develops innovative treatments for solid tumor cancers using immunotherapy and targeted therapies. CKPT’s main value driver is Cosibelimab. This Anti-PD-L1 antibody is designed to treat metastatic and locally advanced cutaneous squamous cell carcinoma (cSCC) as a single-agent therapy.

Source: CKPT’s Q2 2024 Corporate Presentation.

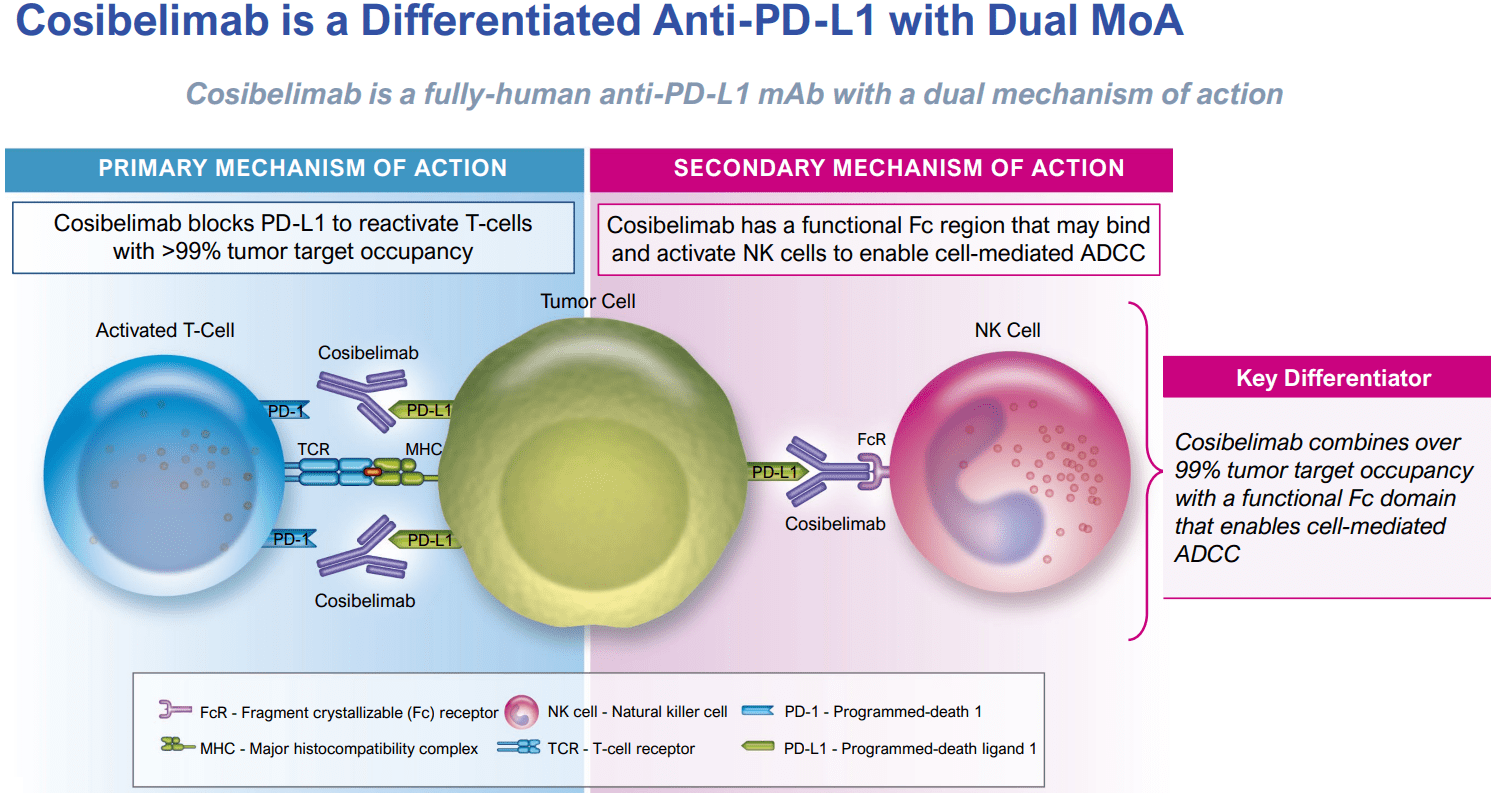

Cosibelimab binds to the PD-L1 protein in cancer cells, blocking it from attaching to the PD-1 receptor in T cells. Normally, PD-L1 allows cancer cells to evade the immune system. However, when Cosibelimab blocks it, T cells can recognize and destroy tumor cells. What sets Cosibelimab apart from other PD-L1 inhibitors is its ability to also bind to natural killer (NK) cells through its functional Fc domain. This gives Cosibelimab a dual mechanism of action because it not only reactivates T cells but also activates NK cells. Thus, this theoretically gives Cosibelimab a more comprehensive effect on cancer cells and could be a key competitive advantage.

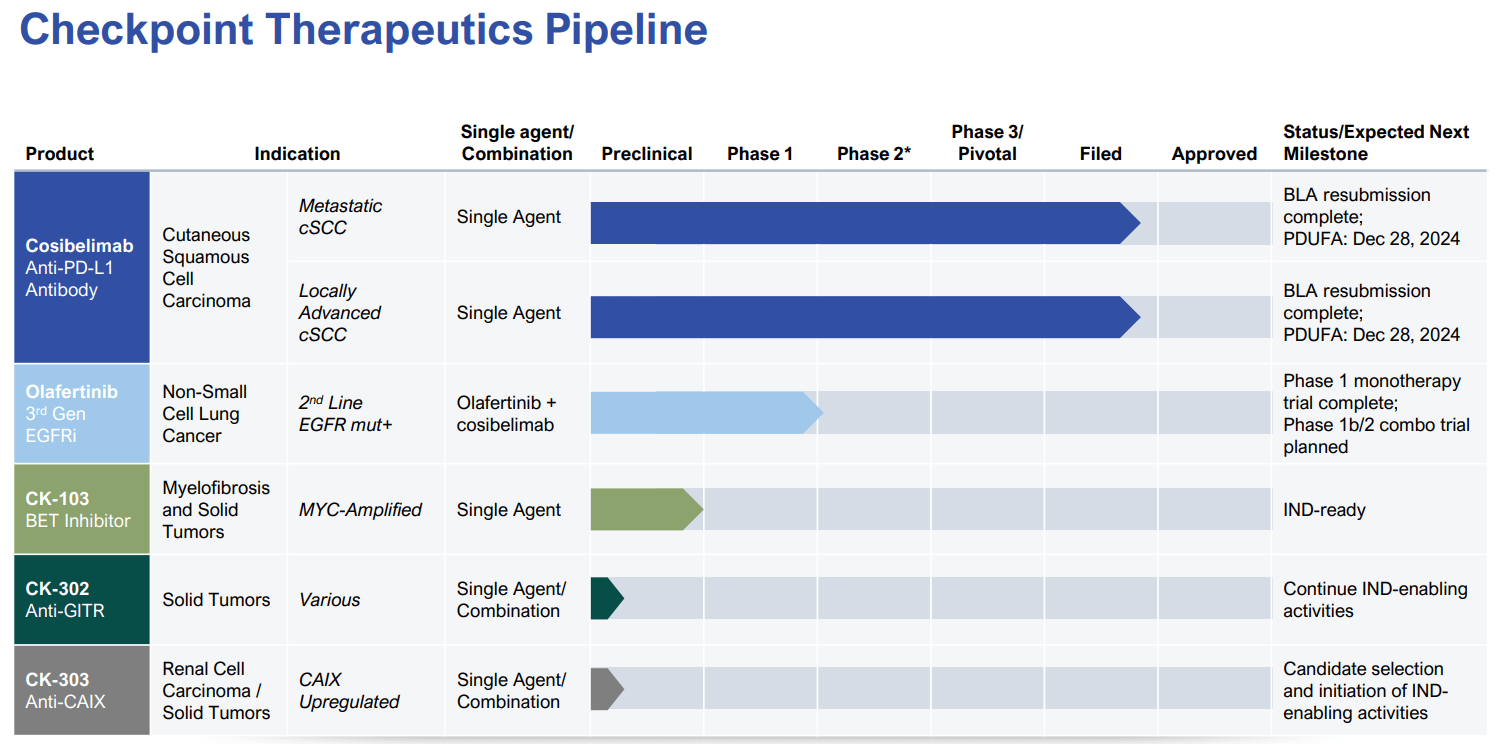

Moreover, CKPT’s pipeline also includes other early-phase candidates. For instance, Olafertinib targets non-small cell lung cancer (NSCLC) with 2nd-line EGFR mutation-positive cases. Olafertinib has so far completed its phase 1 trials as a monotherapy. CKPT is also working on a phase 1b/2 trial testing Olafertinib in combination with Cosibelimab. Additionally, CKPT has CK-103 for myelofibrosis and MYC-amplified solid tumors. However, CK-103 is still in the IND-ready stage. Lastly, the company’s CK-302 and CK-303 are preclinical drug candidates focusing on solid tumors, renal cell carcinoma, and other solid tumors.

Source: CKPT’s Q2 2024 Corporate Presentation.

More recently, on July 25, 2024, CKPT announced that the FDA accepted their Biologics License Application (BLA) resubmission for Cosibelimab. The FDA’s target decision date is December 28, 2024. If the FDA approves it, Cosibelimab could become a key treatment for cSCC in adults who aren’t candidates for surgery or radiation. It’s worth noting that the FDA initially reviewed Cosibelimab back in December 2023. Still, that submission resulted in a complete response letter [CRL] due to manufacturing issues at a third-party CMO. Since then, CKPT has focused on resolving these problems, and its CEO seems optimistic about their approval odds.

Promising Outlook: Competitive Profile

In my view, Cosibelimab’s outlook is promising, especially since the CRL didn’t raise concerns about clinical data, safety, or labeling. If the drug had safety or effectiveness issues, that would have been a significant setback. However, manufacturing problems are generally easier to address. What makes Cosibelimab particularly compelling is its impressive trial data. For metastatic cSCC, the drug achieved an overall response rate (ORR) of about 50%, with significant tumor reduction, and 13% of patients reached complete remission. In cases of locally advanced cSCC, Cosibelimab showed an ORR of 54.8%, with a complete response rate of 26%. Just as importantly, its safety profile seems more favorable compared to other anti-PD-1 drugs.

Source: Fierce Pharma.

To put this in context, Cosibelimab’s main competitors are Regeneron’s (REGN) Libtayo and Merck’s (MRK) Keytruda. Libtayo and Keytruda had 42% and 39% response rates, respectively. So, Cosibelimab appears slightly superior while maintaining a similar safety profile. It’s also worth mentioning that Regeneron purchased Libtayo’s full rights from Sanofi (SNY) for $900 million in 2022. This gives us a sense of Cosibelimab’s potential value if successfully developed and commercialized. That’s why I believe CKPT could potentially become a serious contender in the cSCC market with Cosibelimab.

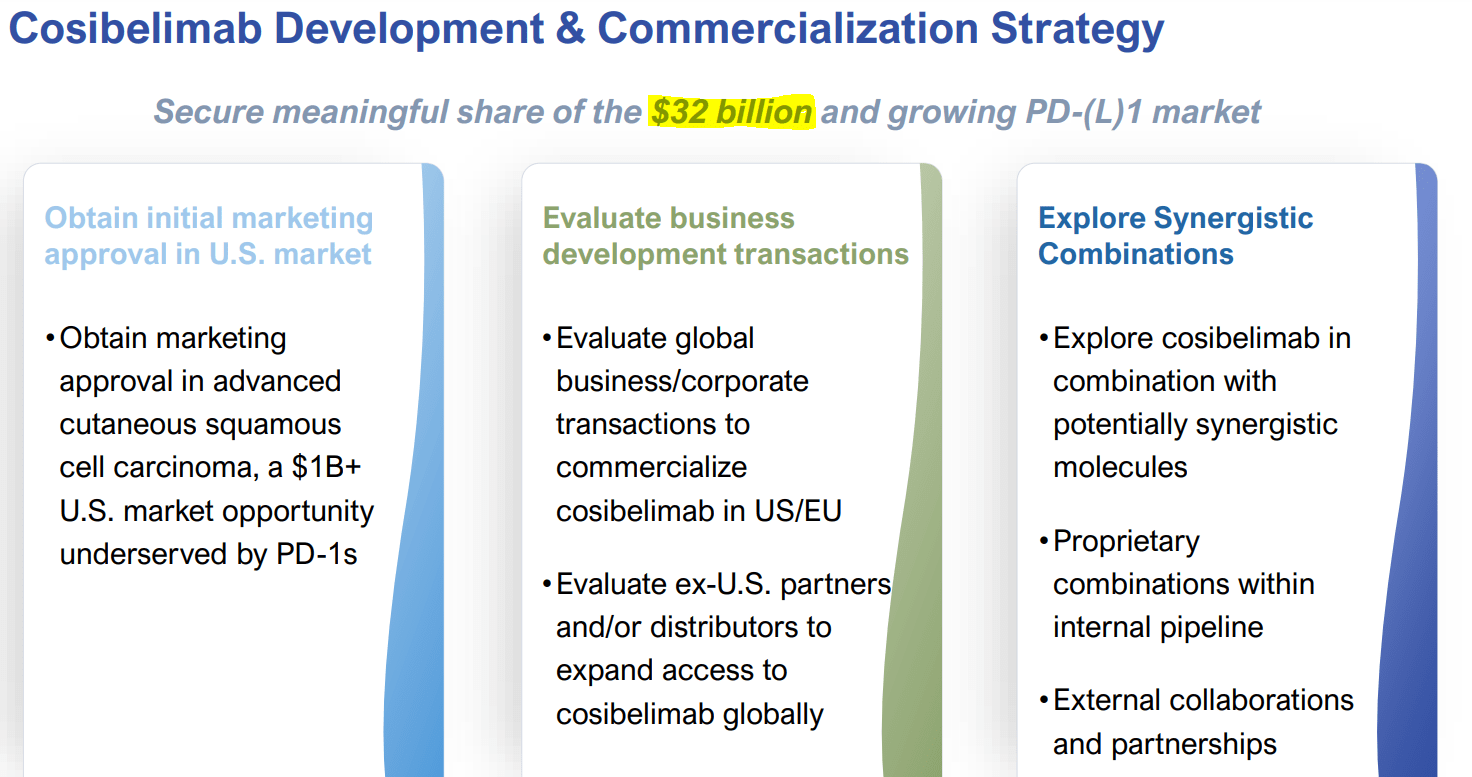

Furthermore, CKPT estimates the market opportunity for Cosibelimab in cSCC treatment to be over $1 billion in the US alone. The drug could potentially treat around 60% of cSCC patients who have unmet needs with current PD-1 inhibitors. I also believe Cosibelimab’s ability to engage NK cells is another key differentiator. This feature makes Cosibelimab particularly beneficial for immunosuppressed patients, such as those with chronic lymphocytic leukemia (CLL), transplant recipients, and others on immunosuppressive treatments.

Source: CKPT’s Q2 2024 Corporate Presentation.

It’s also important to highlight that CKPT owns Cosibelimab’s US rights until at least 2038. So, this would easily position Cosibelimab as CKPT’s core oncology revenue source for the next decade. Additionally, after the FDA accepted Cosibelimab’s resubmission, CKPT’s stock price spiked. So, this reinforces the idea that the market is also optimistic about Cosibelimab’s potential approval. As long as CKPT’s newly submitted BLA aligns well with the FDA’s criteria, Cosibelimab could eventually capture a significant share of the cSCC market.

Binary Outcome: Valuation Analysis

From a valuation perspective, CKPT currently trades at a market cap of $101.3 million. This places it firmly in the microcap category within its sector. This valuation seems particularly low because Cosibelimab is positioned as a similar drug to REGN’s Libtayo. Libtayo was purchased for $900 million, so I believe the notable valuation disparity is likely due to CKPT’s relatively low cash reserves. This adds a considerable risk layer to its investment thesis.

Source: Seeking Alpha.

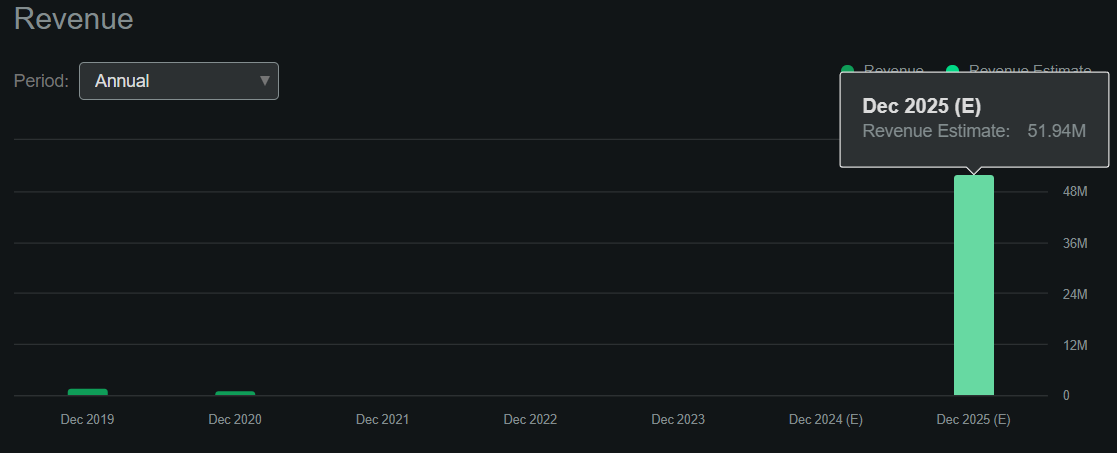

As of June 30, 2024, CKPT’s balance sheet had $5.0 million in cash and equivalents with no financial debt. However, the company’s negative book value of $15.7 million makes it difficult to value through traditional P/B multiples. However, according to Seeking Alpha’s dashboard on CKPT, the company is projected to generate $52.0 million in revenues by 2025. This would price CKPT at a forward P/S multiple of 1.9. For comparison, its sector’s median forward P/S is 3.9, so the stock also seems relatively undervalued.

Moreover, I estimate CKPT’s latest quarterly cash burn was $6.2 million by adding its CFOs and Net CAPEX. This highlights the company’s immediate need for additional funds to sustain operations until the FDA decides on Cosibelimab’s BLA. As previously noted, such a decision’s target date is December 28, 2024. Unsurprisingly, CKPT has announced two equity offerings to address its immediate financing needs. One is for $12.0 million, and another is for up to $5.9 million. These equity offerings would raise $17.9 million combined, bringing CKPT’s cash reserves to approximately $22.9 million. Based on my cash burn estimate, this would provide a cash runway of about 3.7 quarters. I believe this should be sufficient to cover operations until the FDA’s decision.

Investment Caveats: Risk Analysis

While this funding should carry CKPT through the FDA’s decision, it likely won’t be enough to finance Cosibelimab’s commercialization. So, I think investors will probably face some dilution in every scenario. However, if the FDA approves Cosibelimab, it could be a major turning point for CKPT. This could potentially lead to significant upside, especially given the low current valuation relative to the Libtayo sale. Conversely, if the FDA rejects the BLA or issues another CRL, CKPT could face serious challenges. The company might need to raise additional funds under unfavorable terms or even potentially consider bankruptcy. This binary outcome creates substantial risks for investors.

Source: TradingView.

Nevertheless, the outcome of CKPT’s bull case will probably be resolved in the near term. Given the relatively short timeline for the FDA’s decision, CKPT could be a speculative “buy” for investors who understand the inherent regulatory risks and cash runway challenges. I believe Cosibelimab’s promising trial data and favorable valuation compared to Libtayo make CKPT a compelling investment case. Thus, while the risks are significant, CKPT’s upside potential justifies a speculative bullish stance, especially due to its near-term catalyst.

Highly Speculative “Buy”: Conclusion

Overall, I think CKPT’s Cosibelimab has a reasonable chance of being approved by the FDA soon. If that happens, it will have a solid competitive profile in its market and could become a major revenue source for CKPT in the long run. However, we can’t ignore the fact that Cosibelimab has faced FDA setbacks before. This adds a layer of uncertainty, coupled with CKPT’s low cash reserves, making the stock highly speculative. Therefore, I think CKPT is a binary outcome likely to be resolved by yearend or early 2025. But, on balance, I think the upside potential for CKPT is far greater than its downside. Also, I estimate its approval odds are favorable based on the data available today. Consequently, I rate CKPT a viable speculative “buy” for investors who understand the inherent uncertainties in this stock.