Olga Seifutdinova/iStock via Getty Images

It has been nearly 11 months since our last look at Certara, Inc. (NASDAQ:CERT). This small-cap concern has somewhat of a unique niche in drug development. We concluded our last article on this name saying it is a stock to avoid, although the firm is an interesting story. The stock has lost just over 25% of its value since then. Certara has posted several quarterly earnings reports since then and recently made some small acquisitions as well. Therefore, it seems a good time to circle back to Certara. An updated analysis follows below.

Seeking Alpha

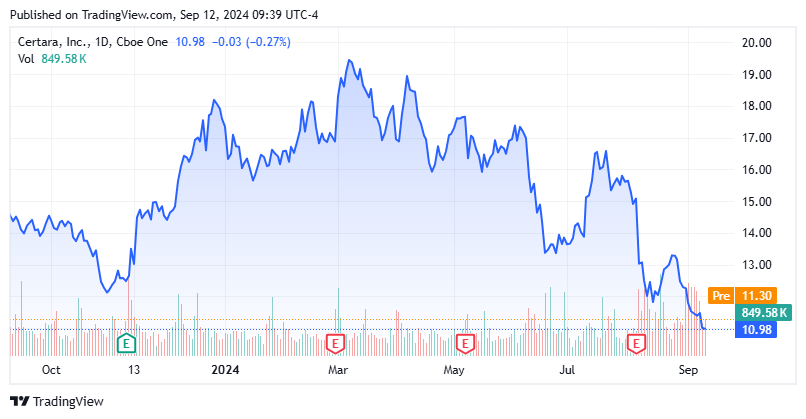

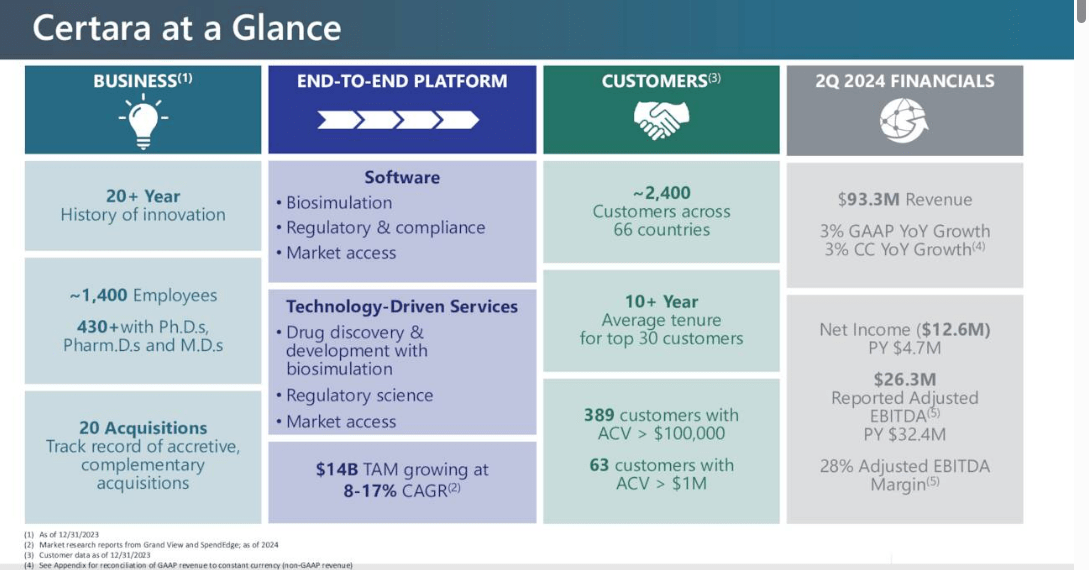

Certara, Inc. is headquartered in New Jersey. The company provides and operates a software platform that allows biosimulation. This is an emerging area that should continue to cut developmental costs and provide better targets for the biotech/biopharma industry. Certara gets both software and services revenue. The stock currently trades at around $11.00 a share and sports an approximate market capitalization of just under $1.8 billion.

August 2024 Company Presentation

Certara is a key leader in the biosimulation space with its Simcyp Mechanistic Modeling suite and Phoenix PK/PD Platform. These provide advanced pharmacokinetic and pharmacodynamic modeling as well as simulation to clients. This in turn helps greatly in generating key insights into drug development and dosing. These software capabilities help streamline drug development, resulting in better optimization and lower developmental costs. Certara has two main revenue streams: Software & Services.

Recent Results:

Soon after the close of the second quarter, Certera signed an agreement to purchase Chemaxon. This is a provider of cheminformatics software and should have roughly $20 million in software revenue in FY2024. In late 2023, Certara made another small acquisition when it purchased Applied Biomath. This company was billed as “an industry leader in providing model-informed drug discovery and development“.

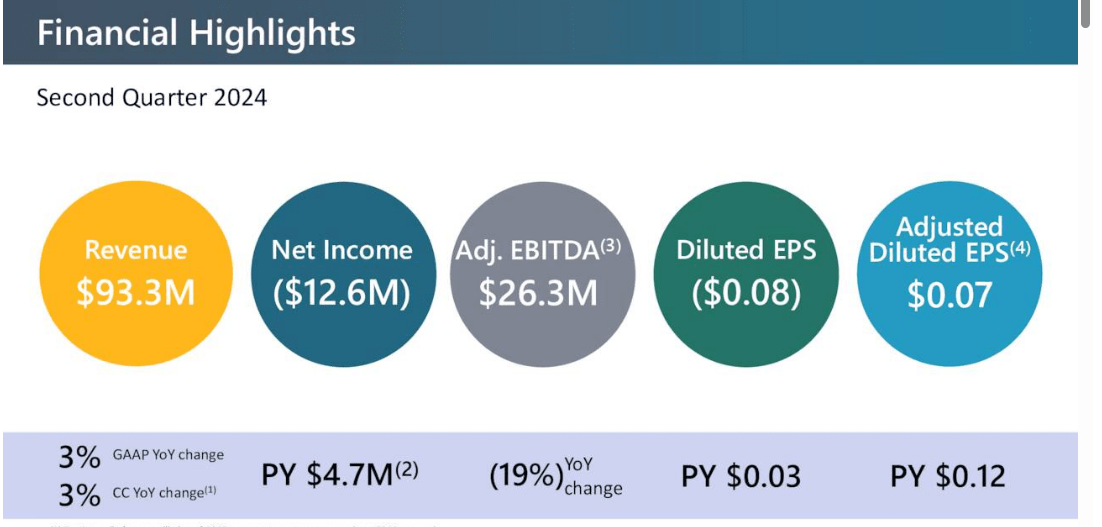

The company posted its Q2 numbers on August 6th. Certara missed both top and bottom-line estimates from analysts. This follows a first quarter report on May 7th that had mixed results. On a GAAP basis, Certara had a net loss of $12.6 million. This compares to net income of $4.7 million in the second quarter of 2023. Higher operating expenses were the reason for the deterioration. Management defined these as:

“primarily due to planned investments to support innovation and growth, and M&A, resulting in higher employee-related expenses, stock-based compensation, and transaction-related expenses.”

August 2024 Company Presentation

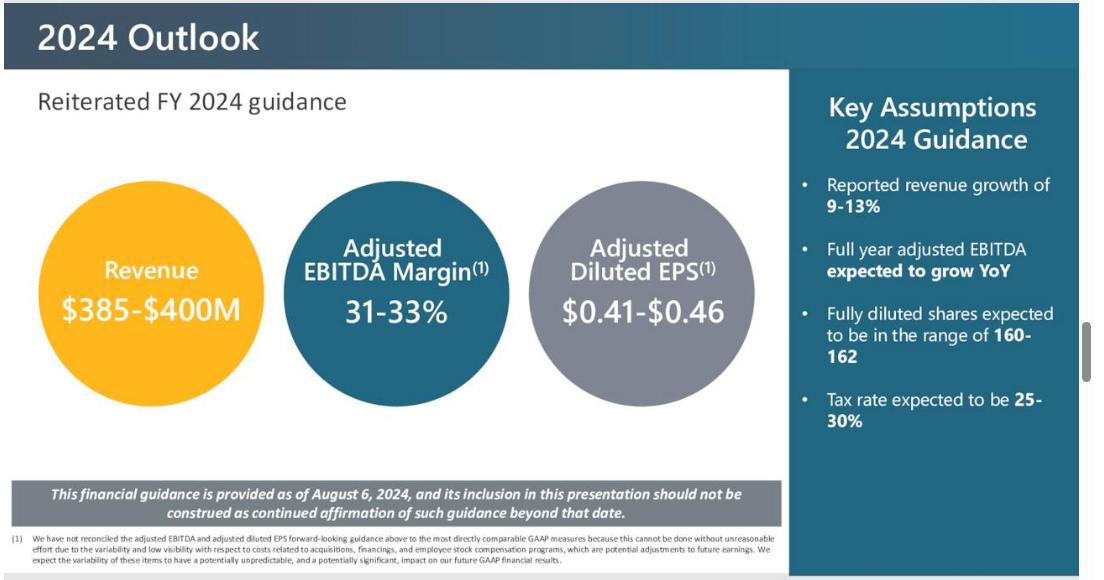

Revenues rose just over three percent on a year-over-year basis to $93.3 million, nearly $3 million south of the consensus. Management provided the following FY2024 guidance, which largely matched the guidance leadership provided after the first quarter results. Sales from Software did grow 13% from the same period a year ago to $38.2 million. However, Services revenues dropped three percent to $55.1 million. Management noted “cautious spending among large biopharma customers” for the decline in Services sales.

August 2024 Company Presentation

Analyst Commentary & Balance Sheet:

It is difficult to find a small-cap less loved on Wall Street right now. Since second quarter results hit the wires, six analyst firms including UBS and Barclays have reiterated Hold ratings on the stock. Two of these had minor downward price target revisions. New price targets range from $15 to $18 a share. Bank of America maintained its Buy rating on the stock and seems the lone optimist on Certara, but the bank declined to place a price target on the stock.

On the 10-Q Certara filed for the second quarter, it listed nearly $225 million of cash and marketable securities on its balance sheet. It also listed long-term debt of nearly $294 million. Management refinance their revolving credit facility and term loan during the second quarter. This pushed out debt maturities and should add a penny a share to earnings in FY2025 and two pennies a share in profit in FY2026. Net interest expense was just under $5.6 million for the second quarter. Just over three percent of the outstanding float in the shares is currently held short.

Conclusion:

Certara, Inc. made 43 cents a share of profit in FY2023 (Non-GAAP) on just over $354 million. The current analyst firm consensus sees earnings dropping slightly to 41 cents a share in FY2024, even as sales rise to $386 million. They project 51 cents a share of profit in FY2025 on just over 10% sales growth.

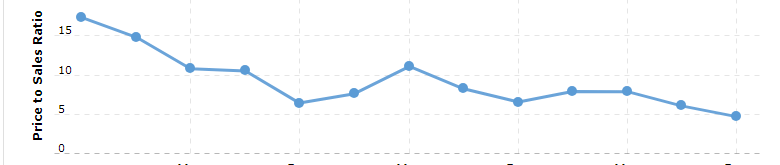

Macrotrends

For those investors that like to bottom fish, it should be noted that CERT has been trading at its lowest price-to-sales ratio over the past five years. In addition, since we last visited Certara, it has made two small acquisitions as it continues to build out its biosimulation capabilities.

I circle back to Certara on an annual basis, as it is a key player in a fascinating part of drug discovery and development. Unfortunately, like pretty much every analyst firm on the Street, it is difficult to currently like the stock. Profits will be flat to slightly down this year, and it is challenging to justify paying 27 forward earnings for CERT (The S&P 500 is trading at just over 22 times forward earnings in contrast and with expected profit growth in FY2024 in the low teens). And this is on a non-GAAP basis. On a GAAP basis, Certara had a $12.6 million net loss in Q2 as previously noted.

As software becomes a bigger contributor to overall sales, revenue growth (and hopefully profit growth) should pick up notably in the years ahead. However, until Certara, Inc. can produce consistent revenue and earnings growth, I will remain on the sidelines around the stock.