beckariuz

Blackstone Secured Lending (NYSE:BXSL) is a top BDC choice for income investors that value a high-quality, well-performing investment portfolio and a highly secure 10% yield. Blackstone Secured Lending suffered only a minor decline in its balance sheet quality in the second-quarter and supported its dividend well with net investment income. Shares of Blackstone Secured Lending are trading, deservedly, at an 11% premium to net asset value and I see a risk profile that is heavily skewed to the upside. Investors that want to overweight quality BDCs that have a chance to sustain their dividends during a recession may want to take a look at Blackstone Secured Lending.

Previous rating

I rated shares of Blackstone Secured Lending a strong buy in June 2024 as the Federal Reserve proved to be reluctant to lower the federal fund rate: The Fed Just Made This 10% Yielding BDC A Strong Buy. Blackstone Secured Lending saw a slight increase in its non-accrual percentage in the last quarter, but at 0.3%, based off of fair value, it is very compared to most BDCs. The 10% yield is also well-supported by net investment income, and I consider Blackstone Secured Lending’s to be a high-conviction idea for income investors, especially those that want to prepare for a potential recession.

Why BXSL’s 10% is worth buying

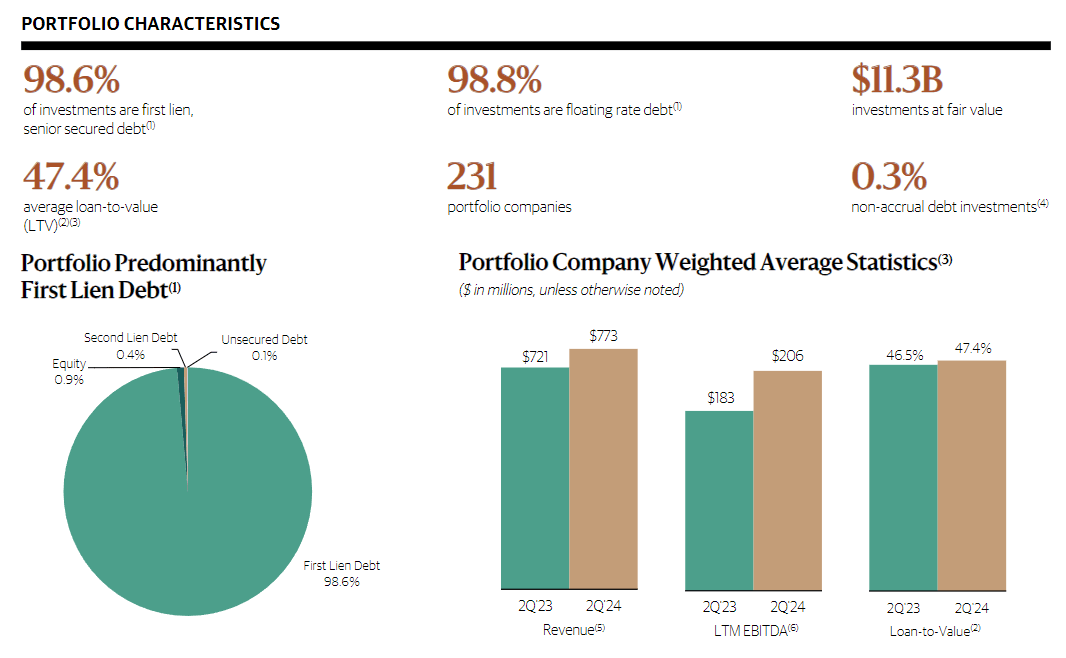

Blackstone Secured Lending is chiefly running a first lien-focused investment strategy, as the BDC’s portfolio structure includes almost exclusively variable rate first liens that generate interest income for Blackstone Secured Lending.

I mentioned in my last work on the BDC that I like Blackstone Secured Lending mainly because of its high degree of balance sheet quality. The investment company has very strict underwriting procedures and has therefore avoided the pitfalls that so many other BDCs have fallen into: originating more loans merely for the benefit of portfolio growth.

Blackstone Secured Lending’s non-accrual percentage, which measures the amount of non-performing loans that are at risk of write-off (or sale), was 0.3% as of the end of June. The non-accrual percentage did decline quarter-over-quarter, by 0.2% PP, but the first lien portfolio is mostly performing. BDCs, for the most part, have non-accrual percentages of 1.0% or higher. As the portfolio is overall performing very well, Blackstone Secured Lending also didn’t report any investment losses in the second-quarter.

Blackstone Secured Lending

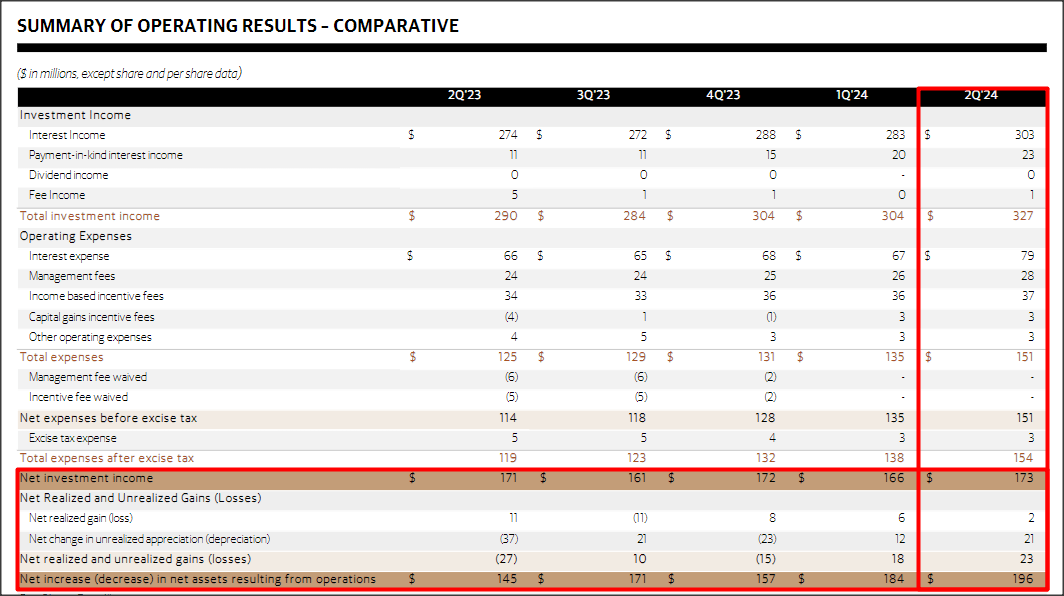

Blackstone Secured Lending generated $173M in net investment income in Q2’24, showing 4% quarter-over-quarter growth. The BDC’s net investment income mainly rose because of a $20M Q/Q increase in interest income. Blackstone Secured Lending, as I indicated in the previous paragraph also avoided investment losses in the second-quarter — the BDC actually saw realized and unrealized gains of $0.12 per-share, net in Q2’24 — which supports my statement that I see BXSL as a higher-quality investment choice in the industry.

Blackstone Secured Lending

Turning to Blackstone Secured Lending’s distribution coverage profile.

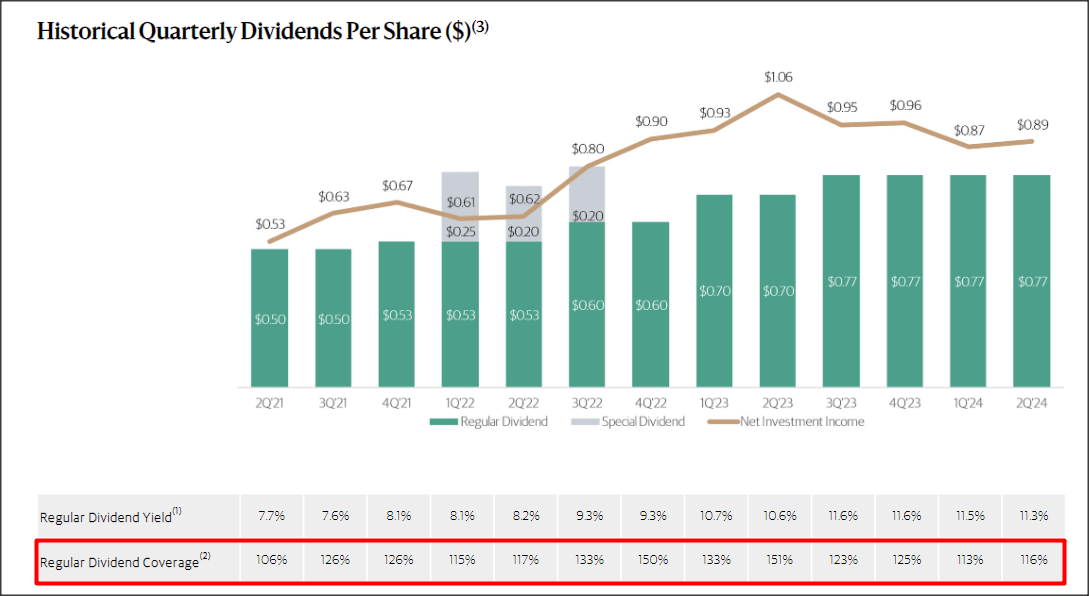

Blackstone Secured Lending’s net investment income of $0.89/share in Q2’24 calculated to a dividend coverage ratio of 1.16X compared to 1.13X in Q1’24. The BDC currently distributes a quarterly dividend of $0.77/share, which I expect to get raised going forward. Blackstone Secured Lending has consistently supported its dividend with net investment income over the years, which makes BXSL an especially reliable dividend payer. Currently, shares of Blackstone Secured Lending yield 10.3%.

Blackstone Secured Lending

BXSL’s valuation

If there is a BDC that is deserving to trade at a premium valuation, it would be Blackstone Secured Lending, in my opinion. The BDC is managing its portfolio well, has excellent credit underwriting (a low non-accrual percentage) and is supporting its dividend well with net investment income.

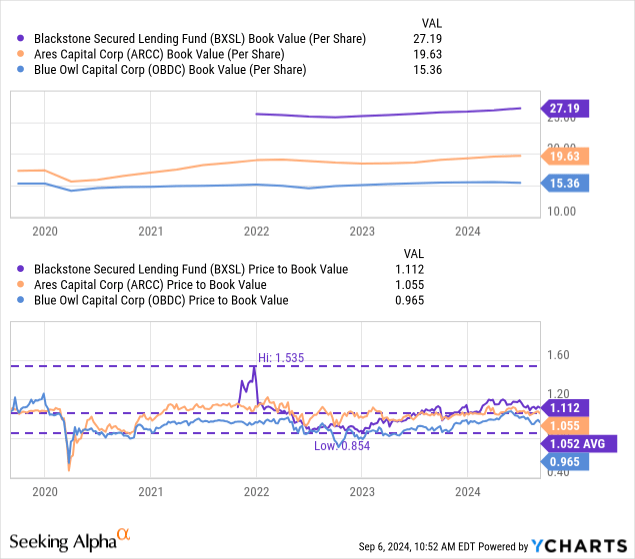

Blackstone Secured Lending is currently priced at a P/NAV ratio of 1.11X while rival BDCs, for the most part, trade considerably closer to their respective net asset values. Blue Owl Capital (OBDC), which has a merger and revaluation catalyst, even trades at a 3% discount to its last reported net asset value. Ares Capital (ARCC), long regarded as the gold standard in the BDC industry, is priced at a P/NAV ratio of 6%. I recommend Ares Capital chiefly because of the BDC’s long history of delivering consistent financial results (with regard to portfolio performance and dividend coverage): A Top BDC For Turbulent Times.

Blackstone Secured Lending’s shares are trading slightly above their longer term (5-year) average P/NAV ratio of 1.05X, indicating that income investors are willing to reward the BDC for its predictable and high-quality growth. In my last work I argued that I saw a fair value P/NAV ratio for Blackstone Secured Lending of 1.25X given the BDC’s superior quality of the portfolio/balance sheet and the well-supported dividend. I confirm my strong buy rating for BXSL and increase my fair value of $33.99 per-share (up from $33.60 due to a Q/Q increase in net asset value).

Risks with Blackstone Secured Lending

The BDC is heavily invested in loans that pay variable rates, thereby posing a risk to Blackstone Secured Lending’s net investment income in a lower-rate world. However, the main reason for me to rate BXSL a strong buy is the investment company’s top-of-class asset quality and the BDC has sufficient excess dividend coverage to suggest that the dividend is not in imminent danger. Therefore, the only factor that would get me to change my mind about Blackstone Secured Lending is if the BDC were to see an unexpected, drastic increase in its non-accrual percentage and a deterioration of its dividend coverage profile.

Final thoughts

In my opinion, buying shares of Blackstone Secured Lending is a solid decision for investors that look to recapture high-quality dividend income. Blackstone Secured Lending is trading above its longer term P/NAV ratio, but the premium is deserved as the portfolio is performing well and the non-accrual percentage is super low, indicating superior asset quality. The dividend looks to be well-supported by net investment income (both in the short and long term) and Blackstone Secured Lending, given its first lien strategy, is a 10% yielding BDC cash cow with the potential to raise the dividend in the future.