temizyurek/iStock via Getty Images

Investment thesis

Diversified mining giant BHP Group (NYSE:BHP) (OTCPK:BHPLF) released its full year 30 June 2024 financial results as well as its updated economic and commodity outlook. Despite the widely talked about difficulties in China which have a big impact on demand for BHP’s commodities, the broader picture can be described as more neutral.

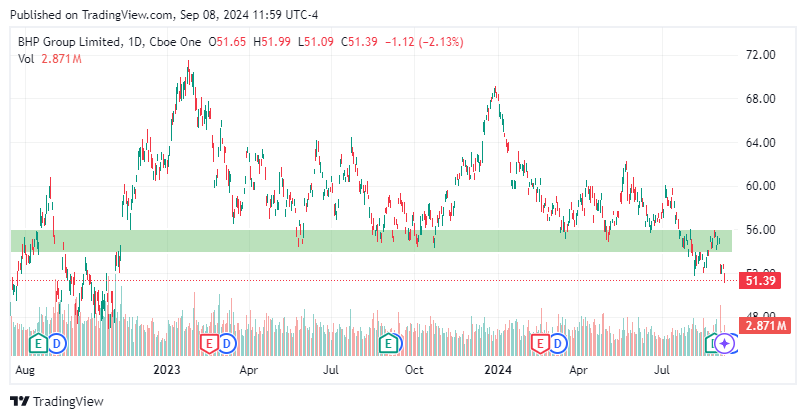

BHP’s top three commodities are iron ore, metallurgical coal, and copper. While copper has held up reasonably well, there are concerns about new low-cost iron supplies coming online in West Africa, something that could disrupt the $100 per ton cost floor. The fall in Chinese steel production hasn’t helped either, and BHP’s stock recently made new 52-week lows, breaking out below what has been a support region for the last two years:

Seeking Alpha

BHP is a low-cost producer across its commodity portfolio, so it should remain profitable even if pricing deteriorates further. The balance sheet is also solid and can likely weather a prolonged recessionary downturn. However, after the unsuccessful takeover of Anglo American (OTCQX:AAUKF) (OTCQX:NGLOY), BHP may be embarking on an organic growth strategy for copper (COPX) which implies more capex and less cash available for distributions to shareholders.

While long-term I remain bullish on the stock and still believe it will benefit from the huge call on mining and metals placed by the so-called energy transition, short-term my stance has shifted to more neutral.

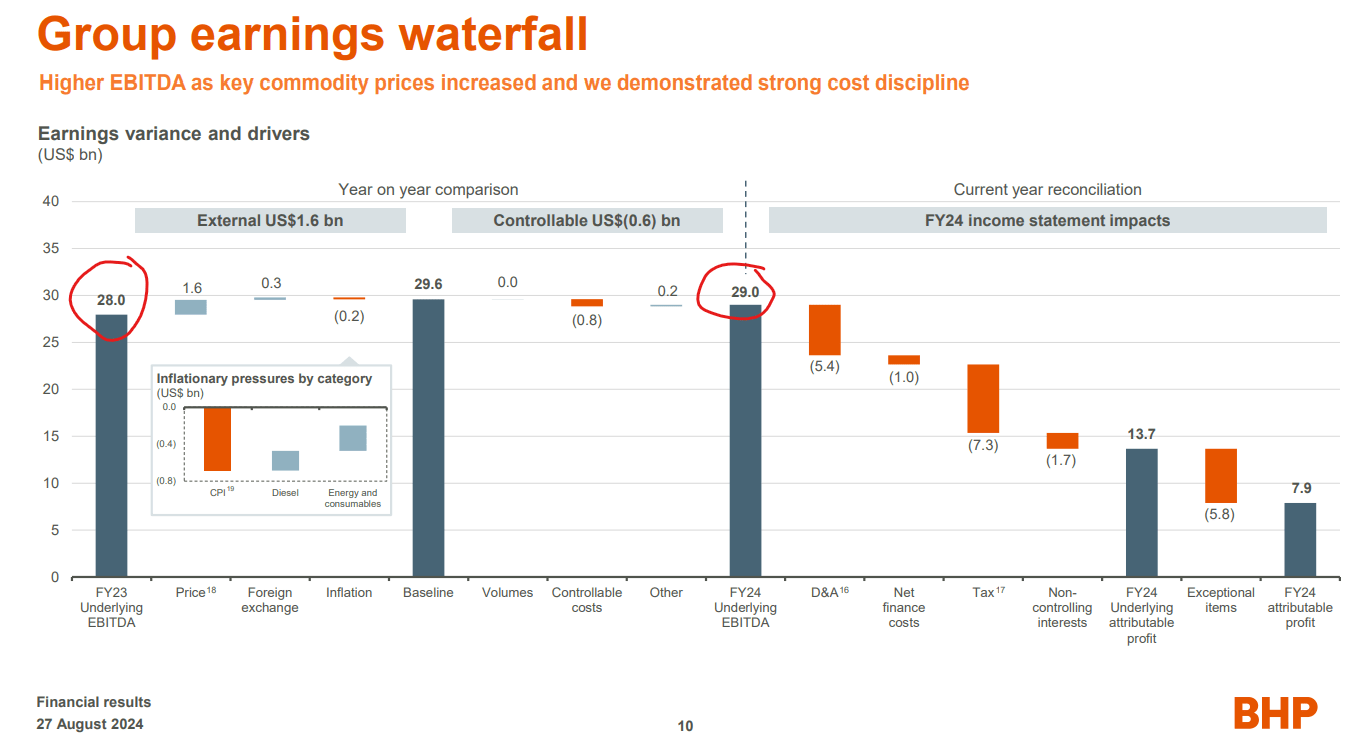

2024 was on par with the prior year

In terms of EBITDA, 2024 was on part with 2023:

BHP Presentation

BHP is now valued at about 5x trailing EBITDA. The total dividend declared for 2024 was $7.4 billion, slightly more than half of the “underlying attributable profit” and consistent the with the company’s policy of distributing out at least 50% of its earnings; this represents a yield of about 5.6%.

The key question is of course whether this performance can be sustained into 2025; management seems to think yes but acknowledges the China wildcard, particularly the property market:

China is experiencing an uneven recovery among its end-use sectors While we see steady growth in some parts of the economy important to commodity demand like conventional infrastructure, zero and low emissions technologies, machinery, automotive and shipbuilding, its property market remains under pressure.

The effectiveness of recently announced pro-growth policies will be key to China achieving its official target of around 5% growth in 2024. Overall, while these dynamics will support continued strong demand for our products, growth and supply over the next couple of years will likely result in a small-to-mild surplus for a number of those and continued price volatility.

These worries imply a mild near term surplus for BHP’s key commodity groups.

The near-term pricing outlook isn’t great

The short summary of BHP’s commodity outlook is that while copper has outperformed, the steelmaking commodities, iron ore and met coal, have been under more pressure; BHP now expects inventories to keep rising with iron being the weakest link:

We expect volatility in commodity markets to continue over the next 18 months, with a general trend of rising stocks across steel-making raw materials and the non-ferrous industries. Having updated our expectations for near–term supply–demand balances (where a surplus means rising inventories and a deficit means inventories are running down), we now forecast the following: refined copper is expected to move towards a marginal surplus, alongside a very tight situation in copper concentrate. We continue to see a sizable but narrowing surplus in nickel. We now anticipate a widening surplus in the iron ore market on average across CY24, with supply likely to continue to outpace demand into CY25. We see a mild surplus for all seaborne steelmaking coals across CY24, but the supply of higher quality coals remains moderately tighter than the market as a whole.

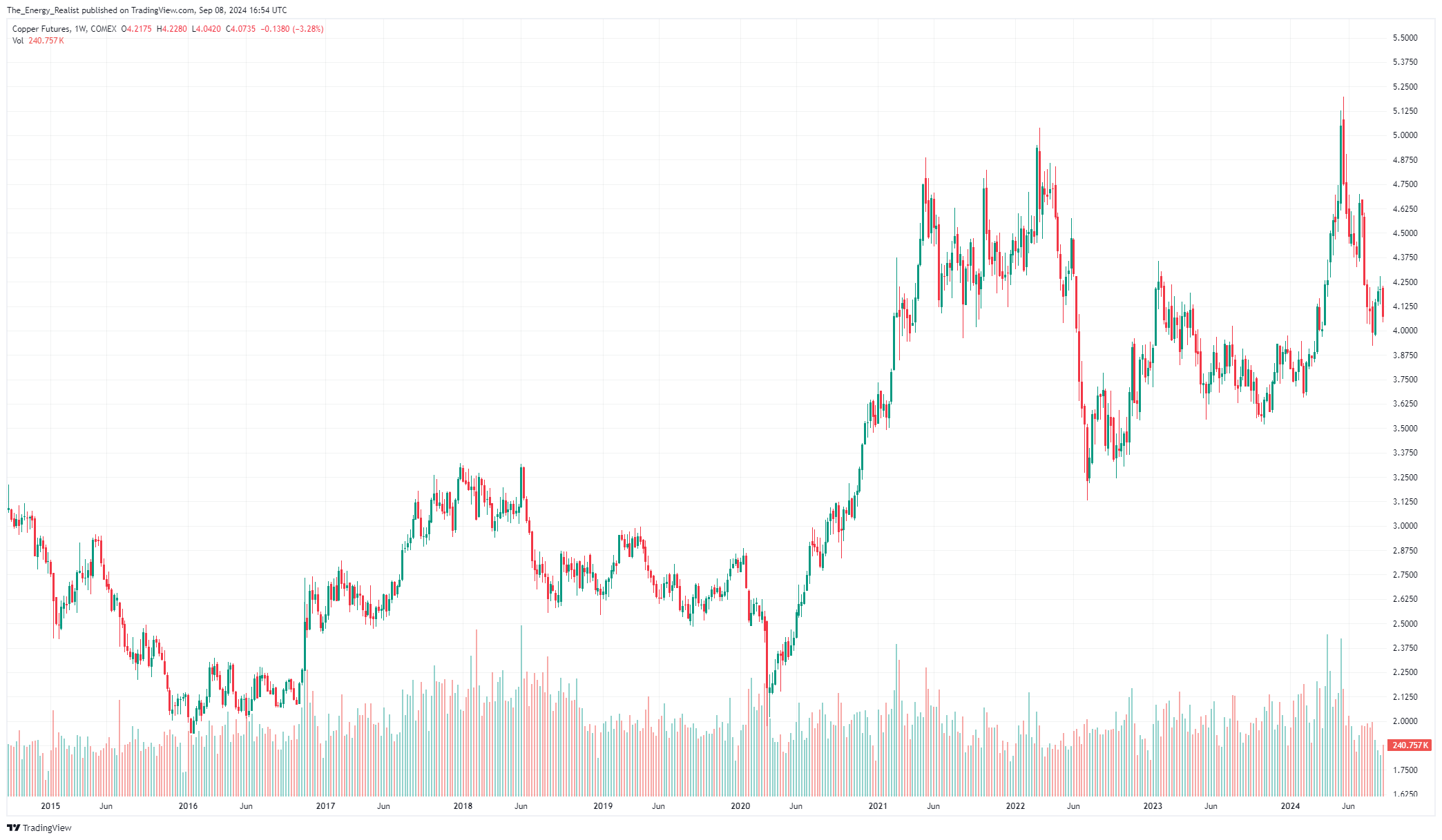

Copper prices have indeed treater after the run-up to $5/lb, but remain very high historically:

TradingView

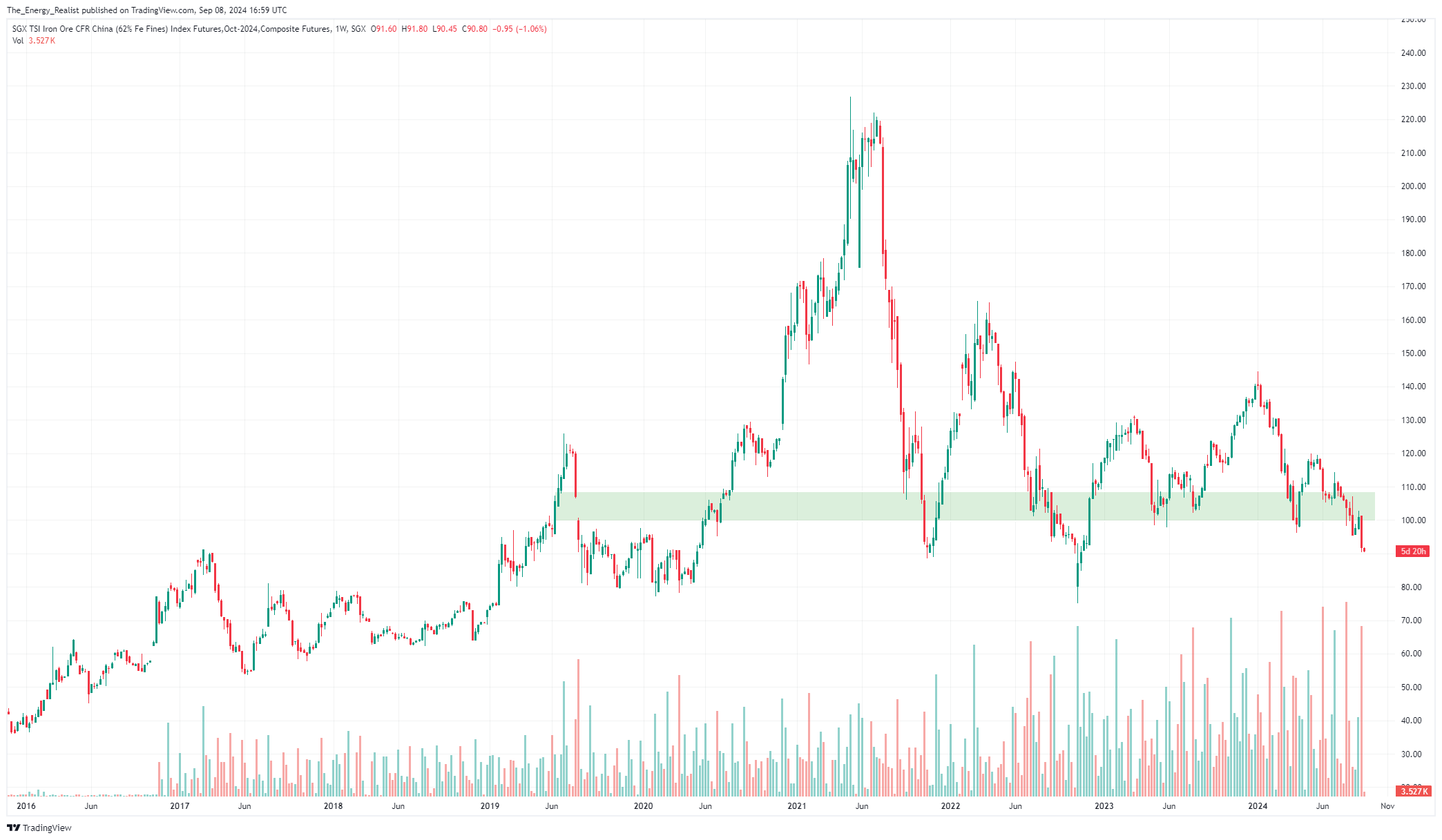

Unfortunately, BHP’s EBITDA is more sensitive to iron ore, which has broken below the $100/t support region:

TradingView

BHP considers $100/t to be “cost support territory” and expects marginal producers would have to shut down at this price:

Our estimate of cost support remains at $80–100/t CFR. In the first half of the year, the top of this range held firm, with marginal seaborne supply coming under pressure when prices approached the $100/t mark, and any dips below that threshold unable to persist for long.

However, this assumption could be tested by new resources in West Africa expected to come online in 2025. According to Mining.com:

The world’s largest untapped ore reserve in Guinea’s Simandou is intensifying preparations for production. The project could deliver 5 million tons starting in 2025 before ramping up steadily to 90 million tons a year in 2028, according to Macquarie Group Ltd.

[Costs] at Simandou, which is divided into northern and southern blocks, would be comparable to the cheapest supply currently available. By the end of the decade, the southern part of the project is likely to be producing at $20 a ton, and the north at $35 a ton, according to Commonwealth Bank of Australia analyst Vivek Dhar, who pegs the long-term iron ore price at just $68 a ton.

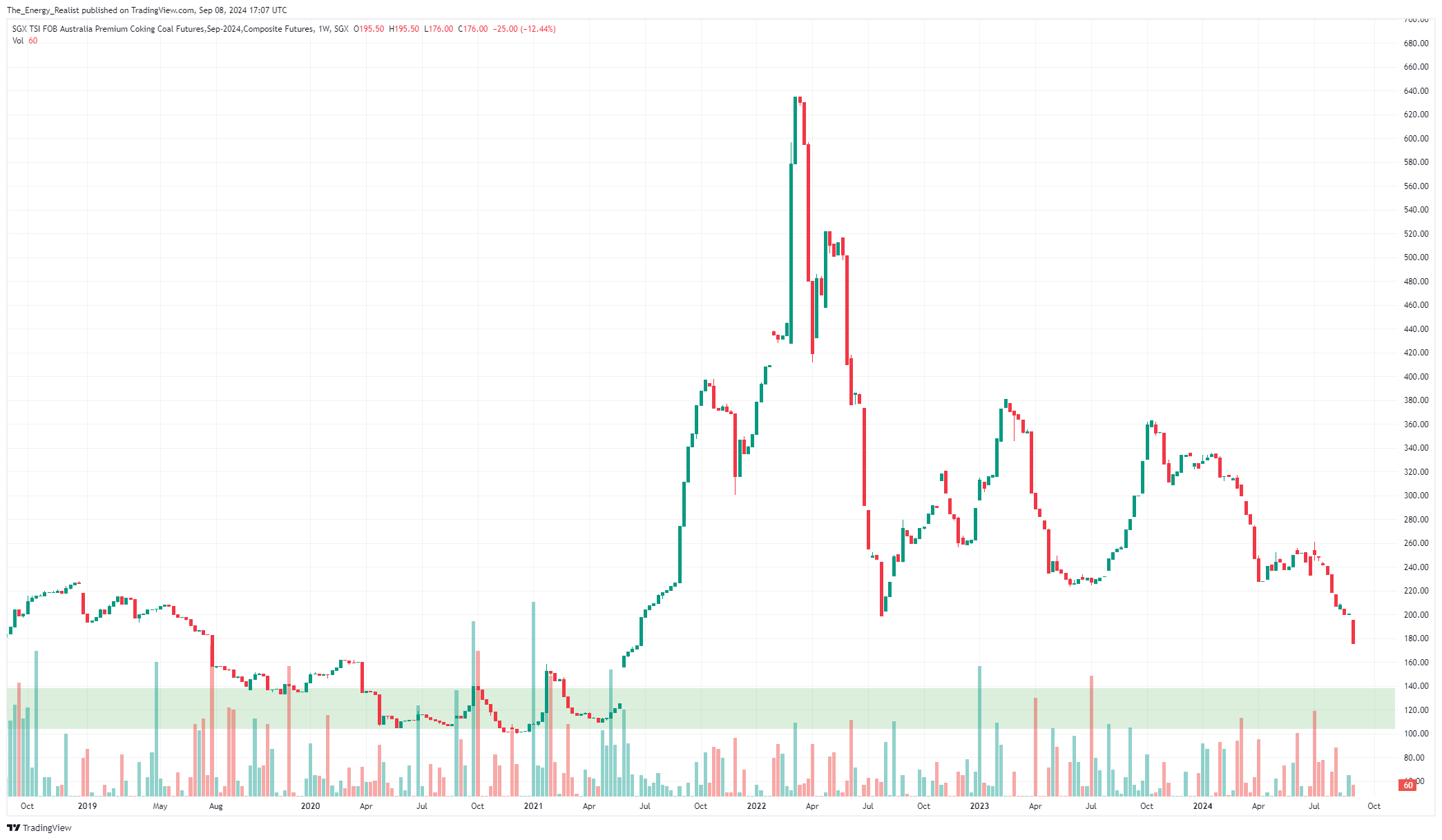

Steelmaking coal also seems to be still in search of a floor:

TradingView

Longer term, BHP believes that high quality coking coal will be sought after because it contributes to lower carbon emissions and the supply in the higher grade spectrum isn’t as large. However, in the shorter term, the price looks like it could indeed fall more.

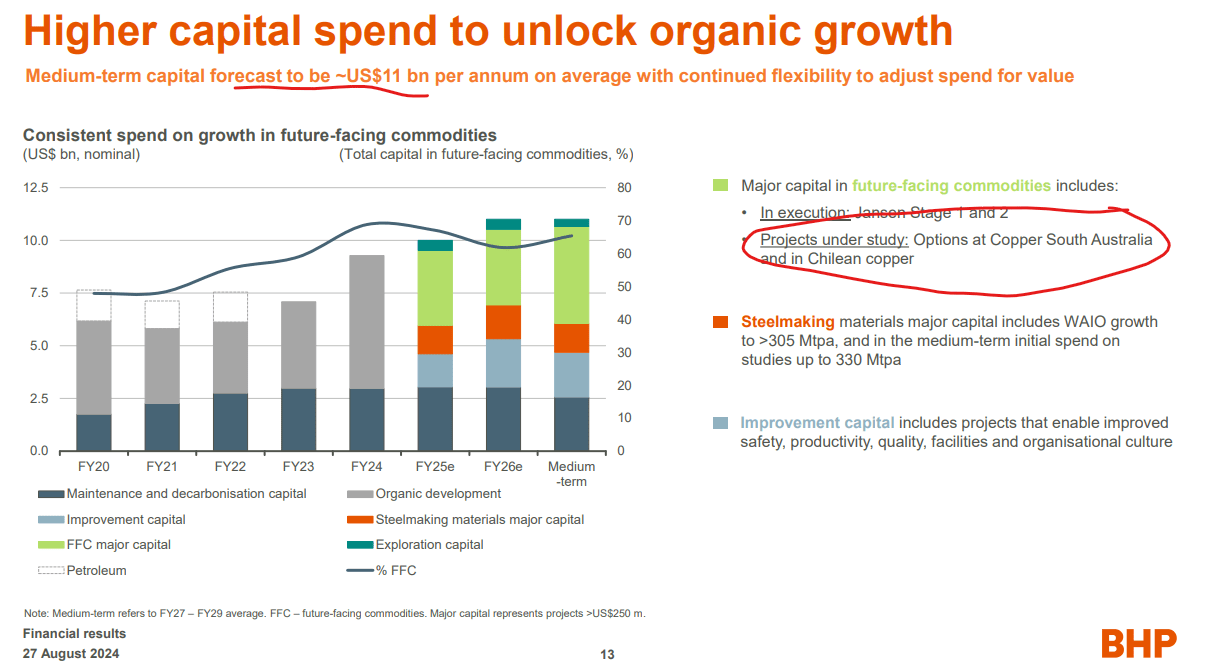

Get ready for the capex cycle

Without further capex, BHP’s copper production from Chile’s Escondida is expected to decline starting in 2027. Given the Anglo-American merger failed, BHP appears ready to substitute acquisition-led with organic growth:

BHP Presentation

This is almost 50% capex increase from 2023; while much needed to deliver higher production in the 2030s, in the meanwhile it has implications for shareholder returns.

In response to an analyst question, BHP’s management even hinted at potentially increasing leverage to meet both the capex and shareholder return goals:

But right now, given the range of CapEx that we’ve talked about, $11 billion, it excludes a few of the things that you mentioned, given the flexibility available in our net debt range and where balance sheet is, we feel they’re comfortable in terms of allocation of really maximizing value for growth projects, but also looking at cash returns.

Other developments

The BHP news cycle has been quite full over the last few weeks. One development has been the reporting that BHP and its JV partner Vale are close to resolving the dispute over the Samarco environmental damages claim with Brazil. The final settlement may be a bit higher than what was reported earlier and could push the stock price down by 3%, assuming this information wasn’t already priced in. Compared to the exposure to iron ore and met coal prices, I don’t see this one-off event as such a big deal.

BHP also averted a prolonged labor strike at Escondida in mid-August. The resolution will increase labor costs for BHP – the linked article talks about a 1% dividend from the mine going towards worker bonuses – but there is also a silver (or copper) lining. Rising regulatory and labor constraints apply to the entire industry, not just to BHP, and push the cost curve up. As a low-cost producer, BHP may ultimately benefit from these trends because additional supply may not be able to step in.

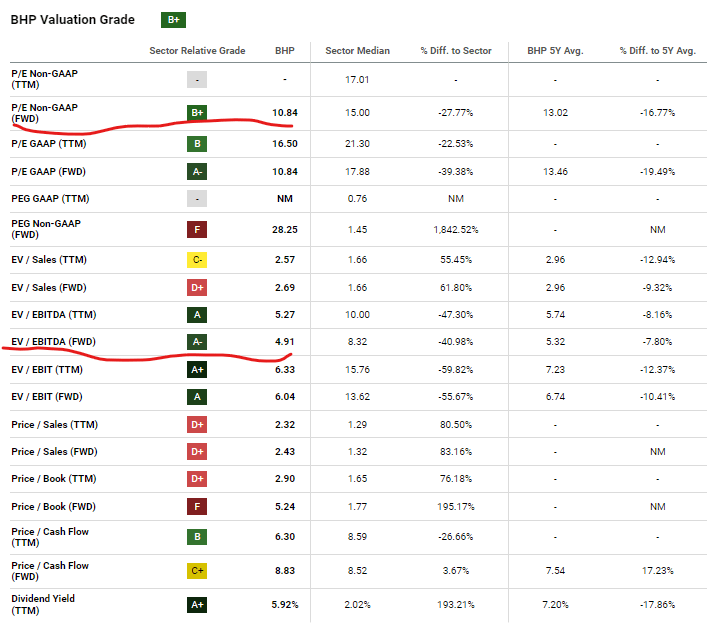

Valuation and targets

BHP’s valuation looks good relative to the sector at 4.9x forward EBITDA:

Seeking Alpha

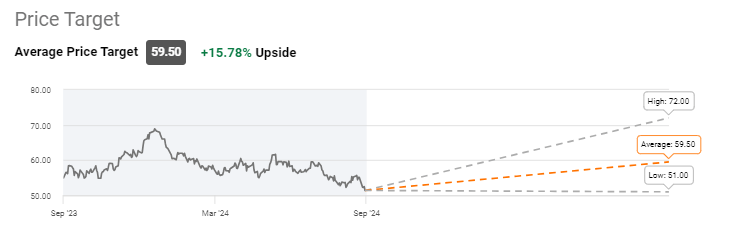

However, that might reflect concerns over deteriorating commodity pricing. The average Wall Street analyst target is now about $60:

Seeking Alpha

This can be achieved with a modest repricing of the EBITDA multiple from 4.9x to about 5.5x; I consider that consistent with a “hold” recommendation.

Takeaway

BHP is the world’s largest mining company by market cap and is also a low-cost producer in its key commodity groups. Long-term, the company is well positioned to benefit from the energy transition call on the metals complex and could perhaps even act as a “hedge” during what increasingly looks like an inflationary decade.

However, short-term the stock may be pressured by iron ore and met coal oversupply, so new entrants may get opportunities to pick a better pricing point. Copper will likely do better than the steelmaking commodities, but getting exposure through “pure play” producers would make more sense.

As for bets on a China recovery, I now prefer a basket dominated by large-cap technology and finance names (FXI), as China’s economy may also be gradually shifting away from infrastructure-led growth to “new economy” and higher value-added sectors.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.