magnez2

American Express Company (NYSE:AXP) is a classic American company that was founded in 1850 through a business consolidation. Approximately 174 years later, AXP sits at a market cap of $183 billion, with more than $15 billion in revenue achieved in Q2, and a net income of approximately $3 billion suggesting an appealing margin.

Although this is a company that has been active for many decades, its top-line growth post-pandemic has been in double digits (after rounding), suggesting that they are not yet in the maturing business stage.

In this analysis, I will look at the company’s growth, valuation, and risks, to decide whether the stock of AXP is a buy, sell, or hold.

American Express: A Multifaceted Global Payments Company

American Express is a globally integrated payments company that offers a wide range of products to its clients. Including credit cards, banking, merchant acquisition and processing, fraud prevention, network services, travel services, and more. Currently, the company is split between four core operating segments with the first one being U.S. Consumer Service (USCS) which is in charge of issuing proprietary consumer cards in the United States and offering banking services.

Followed by Commercial Services (CS), which also issues proprietary cards but in this case, to small businesses and large enterprises. In addition to providing banking services and expense management tools.

Next, is International Card Services (ICS) which is in charge of providing services to both consumers and businesses outside the United States. Finally, Global Merchant and Network Services (GMNS) is the direct competitor of Visa (V) and Mastercard (MA) by operating a global payment network in charge of the processing and settlement of card transactions.

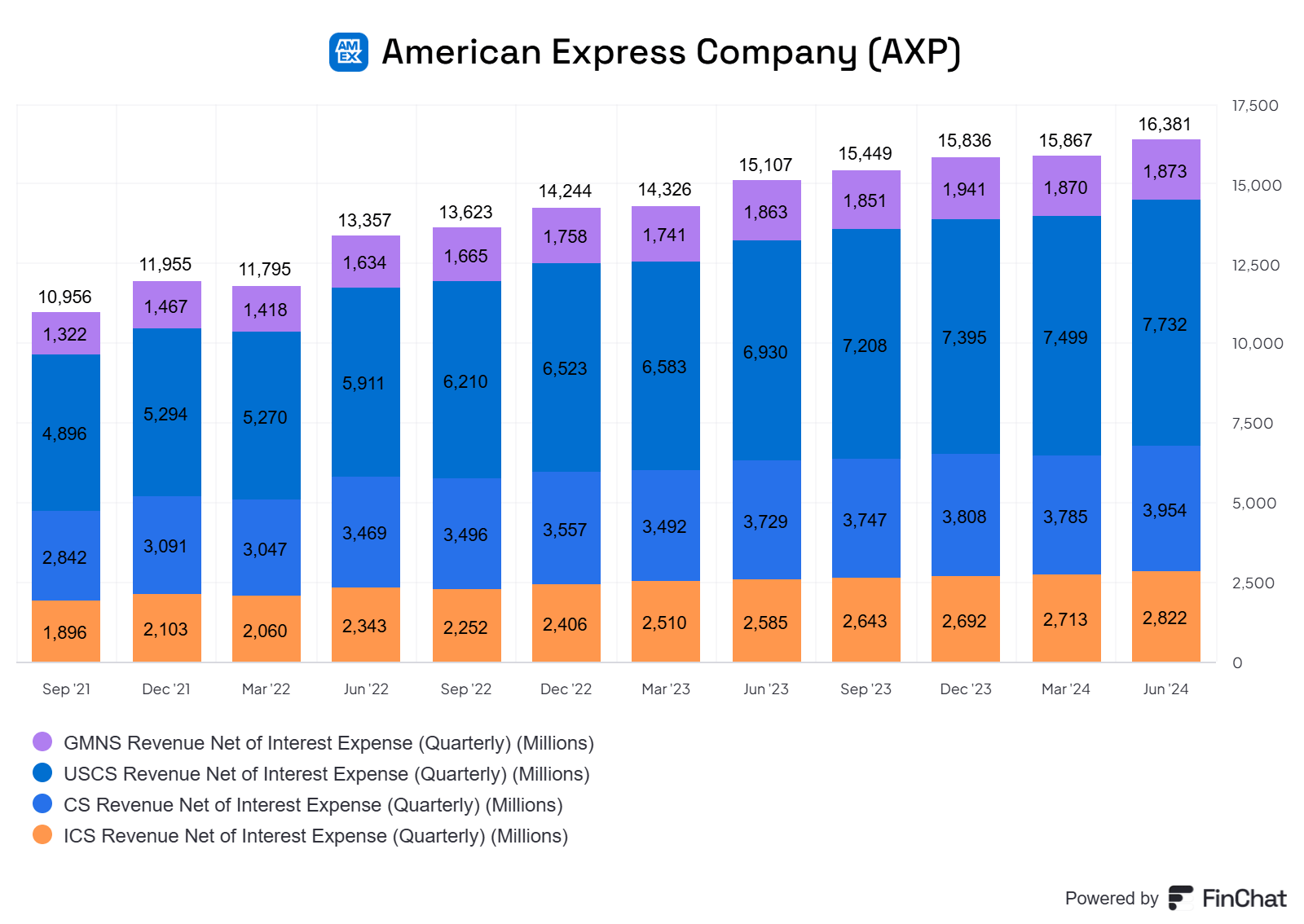

AXP Revenue Growth and Segment Performance

FinChat

Looking at its top line, American Express has exhibited some great momentum with consistent QoQ revenue growth over the past quarters in all of its operating segments. Post 2020, the company had a great growth recovery and in their past two fiscal years they increased revenues by 15.7% and 9.7%.

Currently, their fastest-growing segment is their core segment, U.S. Consumer Services (USC), which in Q2 alone brought $7.732 billion in revenue, representing 11.6% growth from a year ago. Nonetheless, this growth has normalized, as in Q2 ’23, the YoY growth level was some percentage points higher at 16.1%.

The International Card Services (ICS) and the Commercial Services (CS) segments also exhibited similar trends of normalizing growth rates from a year ago and currently their YoY revenue growth rate in Q2 sits at 9.2% and 6.0%, respectively.

Contrarily, the Global Merchant and Network Services (GMNS) segment was the only one that saw minimal growth over the last year as their revenues only increased by a modest 0.5%.

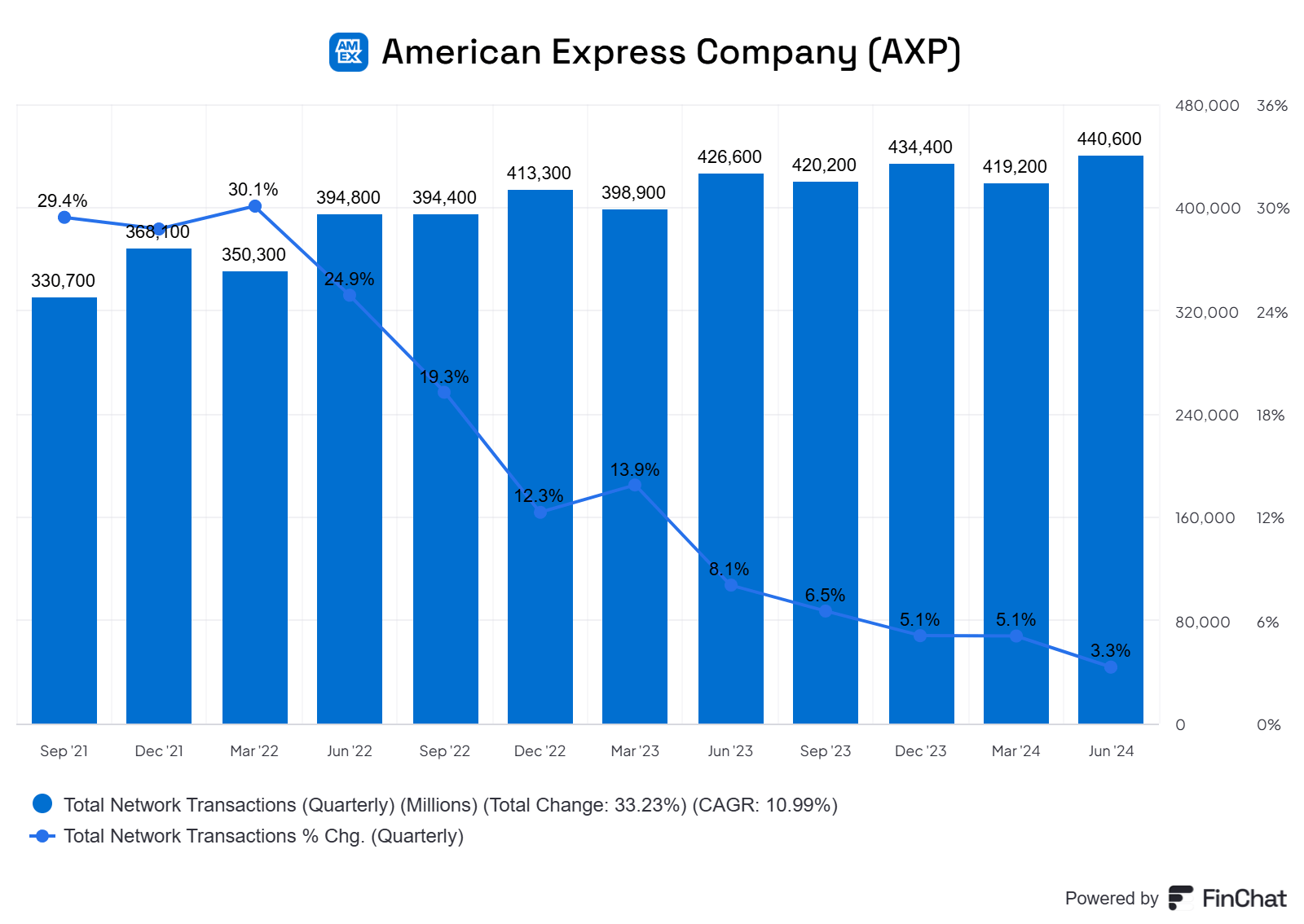

FinChat

The core KPI that describes GMNS’ modest growth, total network transactions (TNT), was $400.6 billion in the previous quarter. As seen in the graph above, this metric has tended to rise consistently, but growth rates have declined, partially due to previous elevated levels from the pandemic recovery in consumer spending, especially within travel, which is an industry where American Express has strong penetration.

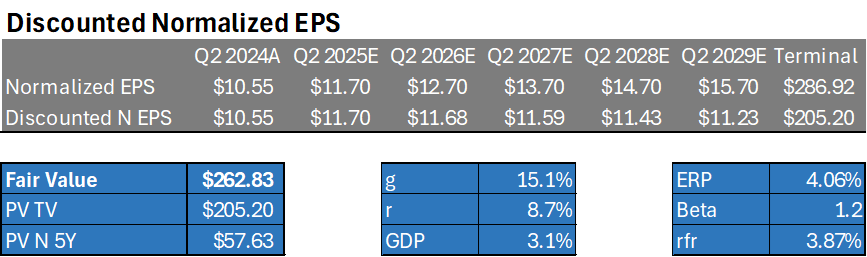

Valuation Analysis of AXP: Fairly Valued Stock

Source: Author’s Compilation | Data: Seeking Alpha, Damodaran, YCharts, TradingEconomics

Running a valuation based on the expected normalized earnings of American Express yields a result that makes the stock fairly valued. This is based on a discount rate of 8.7% using the CAPM model, a perpetual growth rate of 3.1% based on average US GDP, and the average expected normalized EPS growth over the next three years of 15.1% based on analyst estimates. All of that together results in a fair value of $262.63 compared to the current stock price of $258.65.

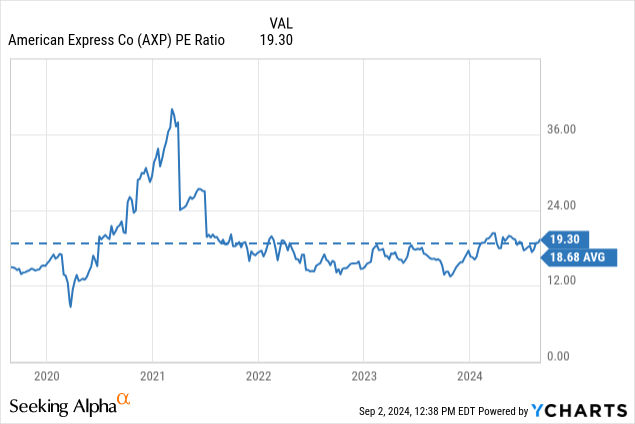

Simultaneously, their current PE ratio sits close to its five-year historical average, implying that the stock is also fairly valued based on a multiple PE comparison. However, due to its price increase, the PE multiple has expanded significantly since October, when the stock traded at a minimum of 13.26x and now sits at 19.30x.

| AXP | V | MA | |

| Return on Equity | 34.98% | 48.55% | 187.70% |

| Price to Book (TTM) | 6.20x | 13.42x | 58.85x |

Source: Seeking Alpha

Finally, at first glance, the price to book multiple of 6.20x might immediately seem overvalued. Nonetheless, this high multiple is helped by its elevated return on equity of 34.98%, which is considerably inferior to other competitors. Unfortunately, the justified price-to-book formula returns meaningless results as in the denominator the cost of equity is inferior to its sustainable growth rate due to high retention ratio and elevated ROE.

Interest Drops Impact on American Express

AXP 10-Q

Based on the sensitivity analysis of the company’s latest 10-Q, interest rate drops would most likely benefit their net interest income. Although American Express is a company that makes most of its revenues from non-interest income, the truth is that interest income still represented 22.8% of revenue in Q2. A drop in rates (with constant spreads) incentivizes consumers to spend at higher levels, which would potentially benefit AXP in revenue streams such as discount revenue.

This scenario is consistent with the previous risk assessment of Q4, with the difference that an instantaneous parallel rate shock of -100bps would result in an extra NII of $152 million vs. $74 million some quarters ago. All of this implies that the company’s hedge instruments have been positioned to benefit more from a rate-cut scenario.

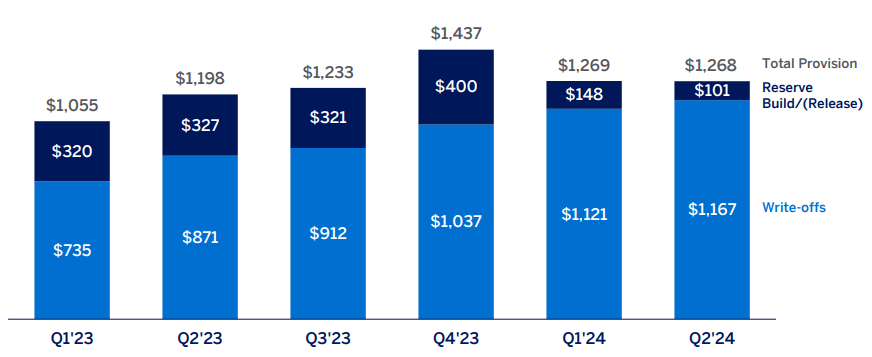

Risks for American Express

AXP 2Q Presentation

The most notable risk for American Express is rising write-offs over the past quarter. As seen in the graph above, these have been growing consistently to the point of reaching $1.167 billion in Q2 ’24. Nonetheless, during the Q2 earnings call, the company expects its write-offs to remain stable for the remainder of the year.

Unlike competitors such as Visa and Mastercard, American Express has revenue streams that predominantly come from the United States. This could be a positive aspect due to the large purchasing power of the US consumer, and a potentially more efficient cost structure. Nonetheless, it provides a significant concentration to a single economy that the consumer spending composition of its GDP is approximately 70%. Even more risky when American Express and other card payment companies are highly dependent on the economic cycle.

In June, eBay announced that it would stop accepting American Express cards as one of its payment options due to its high fees. For no one is a secret that American Express fees are among the highest as it is common to enter some stores where there is a sign that American Express cards are not accepted. Although eBay news is probably not material to the top line, it is a risk that larger merchants stop seeing American Express as a payment option due to its high fees.

Nonetheless, the value proposition of American Express to merchants is similar to the one of Affirm (AFRM), but with different types of clients. Both priced high fees to merchants, all with the intention that providing benefits to customers would increase the average purchasing price compared to other payment methods. Of course, American Express targets affluent customers, while Affirm for the most part serves the other range of the spectrum with customers with lower-than-average FICO scores. Therefore, accepting American Express Cards could be perhaps a net gain for merchants. Especially the ones with higher gross margins.

Takeaway and Stock Rating

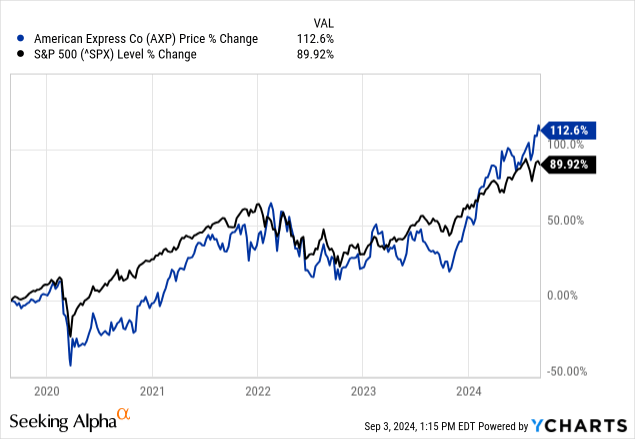

The stock of American Express has been able to obtain similar total returns to one of the S&P 500 over a five-year look back period. In addition, the stocks sit fairly valued based on several valuation methods, and the revenue growth rate of double digits reiterates the existent potential. Nonetheless, I can’t find a clear catalyst for the stock to outperform the market going forward, and therefore I rate the stock as a hold.

Seeking Alpha

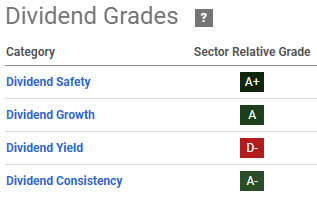

Yet, I find this stock an attractive income play for patient investors due to its track record of incrementing its dividend (ex-covid) at appealing levels. For example, 10 years ago, they paid a dividend per share of $0.98 and now sits at $2.60. In addition, Seeking Alpha gives them solid quant ratings, except for the dividend yield at 1.01%.