Arctic-Images

Enterprise Products Partners (NYSE:EPD) is a superbly run midstream firm with growing adjusted EBITDA, cash flow available for distribution and earnings. The midstream enterprise is also seeing significant momentum in its core gas business and easily supported its generous distribution with distributable cash flow. Enterprise Products Partners also just announced another acquisition in the Delaware basin, which is set to add EBITDA as well as cash flow going forward. Investors are set to see their distributions grow in the long term and the current valuation still makes EPD attractive as an income play.

Previous rating

In June, I pointed to Enterprise Products Partners’ strong value proposition for income investors, resulting in a strong buy rating, as the midstream firm outperformed other companies in terms of distribution growth. Enterprise Products Partners just announced the acquisition of yet another midstream firm, Piñon Midstream, which is set to complement the company’s NGL position in the Permian.

Massive midstream footprint, growing EBITDA

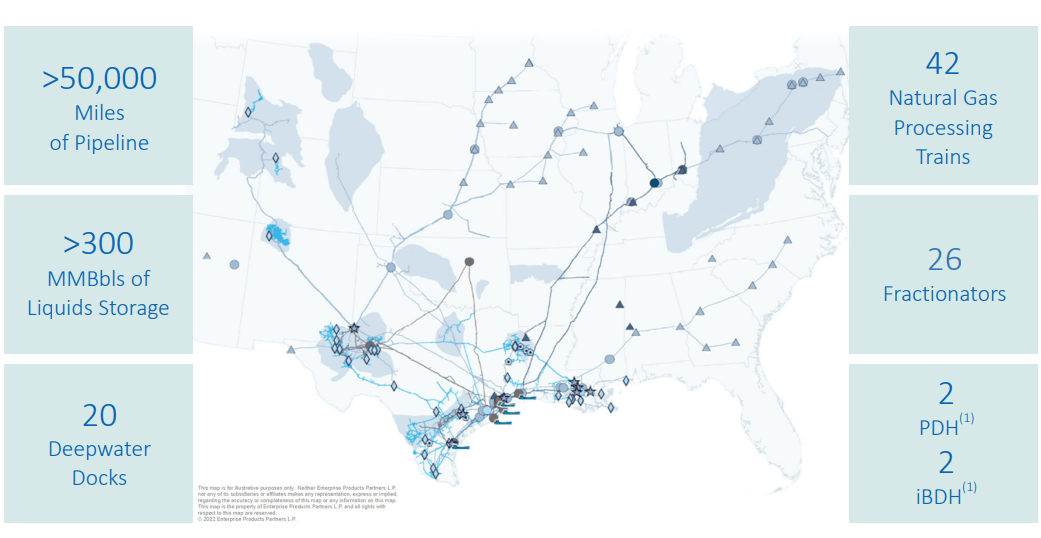

Enterprise Products Partners is one of the largest midstream enterprises in the U.S. The company owns more than 50,000 miles of pipelines, mostly focused on the transportation of natural gas liquids as well as crude oil, petrochemical and refined products. This pipeline network is complemented by a large mix of other energy infrastructure assets including storage facilities, deep water docks, fractionator facilities and other processing and transportation assets.

Enterprise Products Partners

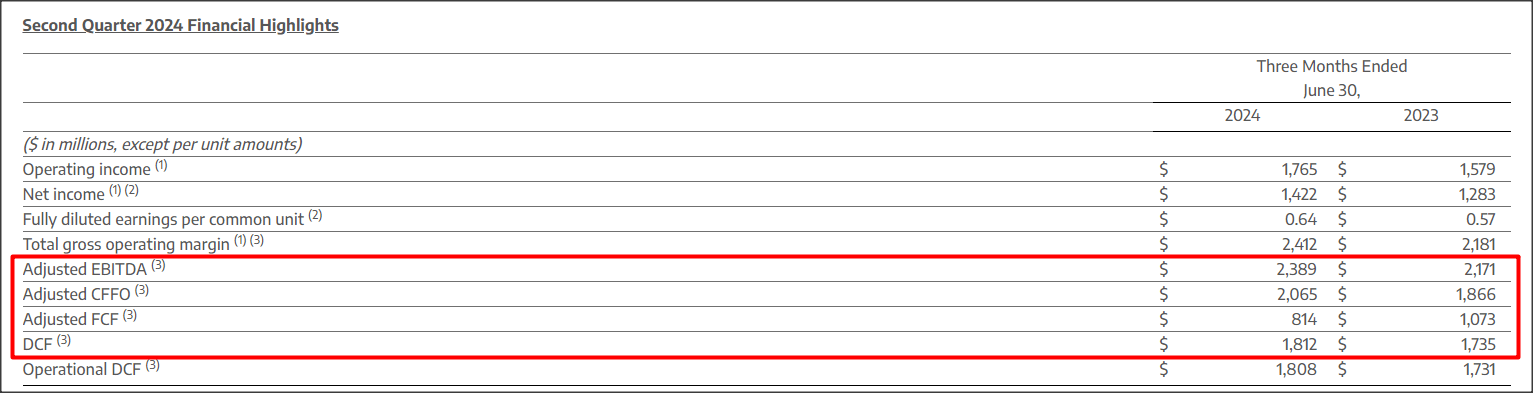

Enterprise Products Partners is growing both its adjusted EBITDA as well as distributable cash flow through organic growth as well as acquisitions. In the second-quarter, the midstream company generated adjusted EBITDA of $2.39B, showing 10% year-over-year growth. At the same time, Enterprise Products Partners’ distributable cash flow amounted to $1.81B, showing an increase of 4% year-over-year.

Enterprise Products Partners

Despite the lower DCF growth rate, the midstream company is easily covering its (growing distribution), with distributable cash flow. Enterprise Products Partners supported its distribution with DCF quite easily in the second-quarter: the distribution coverage ratio in Q2’24 was 1.6X, compared to 1.7X in the previous quarter. Besides a solid distribution coverage profile, Enterprise Products Partners is growing its distribution, which makes units especially attractive to income investors following a long-term investment strategy.

Further upside potential, in terms of EBITDA and distributable cash flow, could come from Enterprise Products Partners’ latest acquisition in the Delaware basin. EPD just reported (August 21, 2024) that it agreed to acquire Piñon Midstream for $950M in an all-cash transaction. The transaction will add 50 miles of natural gas gathering pipelines as well as other assets, including hydrogen sulfide and carbon dioxide treating facilities. Enterprise Products Partners projects that the acquisition will be accretive and add $0.03 per-unit to its distributable cash flow in FY 2025.

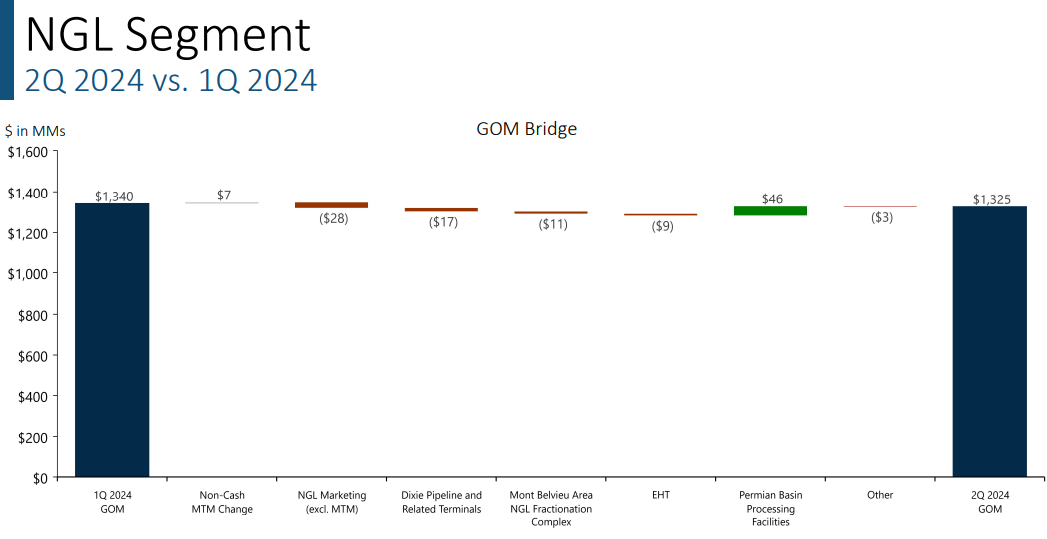

Importantly, the acquisition complements and strengthens the important NGL business, which is generating the majority of gross operating margins. In Q2’24, the NGL segment generated 55% of all gross margins in Enterprise Products Partners’ business, a total of $1.3B. This business had the second-highest growth rate (+19% Y/Y) in Q2’24, after natural gas pipelines (+23% Y/Y) and is obviously the segment with the biggest potential gross margin impact going forward.

Enterprise Products Partners

Enterprise Products Partners’ valuation

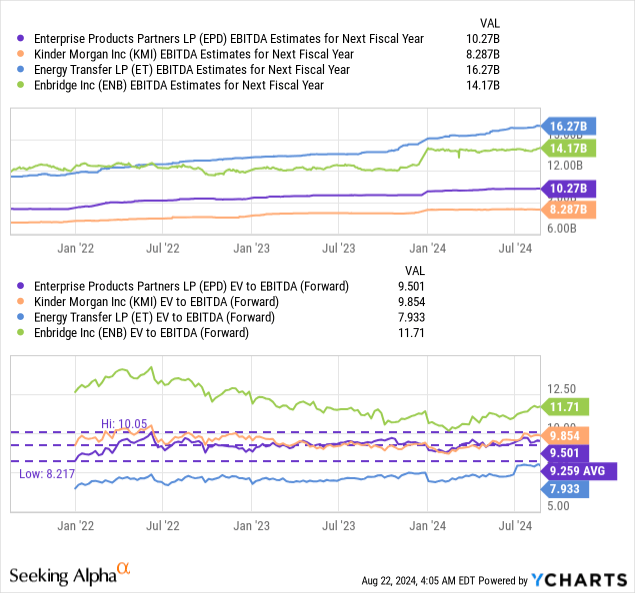

The midstream company’s units are trading at an enterprise-value-to-EBITDA ratio of 9.5X, which about equals the average EV-to-EBITDA ratio in the industry group. The average enterprise-value-to-EBITDA ratio is 9.7X, and I include Kinder Morgan (KMI), Energy Transfer (ET) and Enbridge (ENB) in the industry group represented below. All companies are focused on midstream operations and own large pipeline networks that connect producer areas with consumer end-markets.

As I indicated in my last work, I see a higher valuation multiplier for Enterprise Products Partners chiefly because the midstream firm has a superior distribution growth record and the company has also considerable experience acquiring new energy assets and integrating them into its existing operations. Acquisitions are therefore playing an important role in EPD’s overall growth strategy, and it has been a lever for distributable cash flow growth in the past.

In my opinion, Enterprise Products Partners’ units could revalue to a 10-11X enterprise-value-to-EBITDA ratio, which implies a fair value in the range of $30.66 and $33.77 per-unit. Should the unit price approach my upper-range fair value target, I would consider reducing my position and changing my rating as well. With a fair value of up to $33.77 per-unit, EPD has 16% upside revaluation potential.

Risks with EPD

Enterprise Products Partners is focused on the fossil fuel industry and, as such, subject to limitations placed on its business by environmental regulations. As such, federal agencies can place limits on the company’s expansion projects, which may negatively affect Enterprise Product Partners’ EBITDA and distributable cash flow prospects going forward. There is also no guarantee that Enterprise Products Partners will be able to realize its estimated synergy benefits with regard to the Piñon Midstream acquisition. What would change my mind about EPD is if the midstream firm were to see a drop in its distribution coverage ratio, or if it failed to grow its distributable cash flow at all.

Closing thoughts

Enterprise Products Partners is a well-run midstream enterprise with growing NGL operating gross margins, an increasing footprint in the growing Delaware basin as well as a considerable excess distribution coverage. Enterprise Products Partners is also seeing significant growth in its core business, especially in NGLs and natural gas pipelines… resulting in double-digit EBITDA growth in Q2’24. The latest acquisition of Piñon Midstream is expected to be accretive to distributable cash flow as well, which may further improve the midstream firm’s distribution coverage ratio. Since EPD is growing its distribution consistently, EPD is chiefly an investment for income investors. Currently, units of Enterprise Products Partners pay investors a 7% distribution yield and units are still quite moderately valued based off of the enterprise-value-to-EBITDA ratio.