deepblue4you/E+ via Getty Images

Continental (OTCPK:CTTAF) (OTCPK:CTTAY) looks simply undervalued. They are going to spin off their automotive business. We don’t really have any detail regarding how much debt will be offloaded to the newCo or other important information to put targets for the respective entities, we recognise that Continental is undervalued using pretty straightforward peers which is possible to do as Continental’s businesses are quite representative of the overall industries they’re in, and a spin-off may actually work. The issue is that they are exposed to recessionary focuses in the meantime, as the spin-off is expected to occur in 2025.

Earnings and Spin-off brief

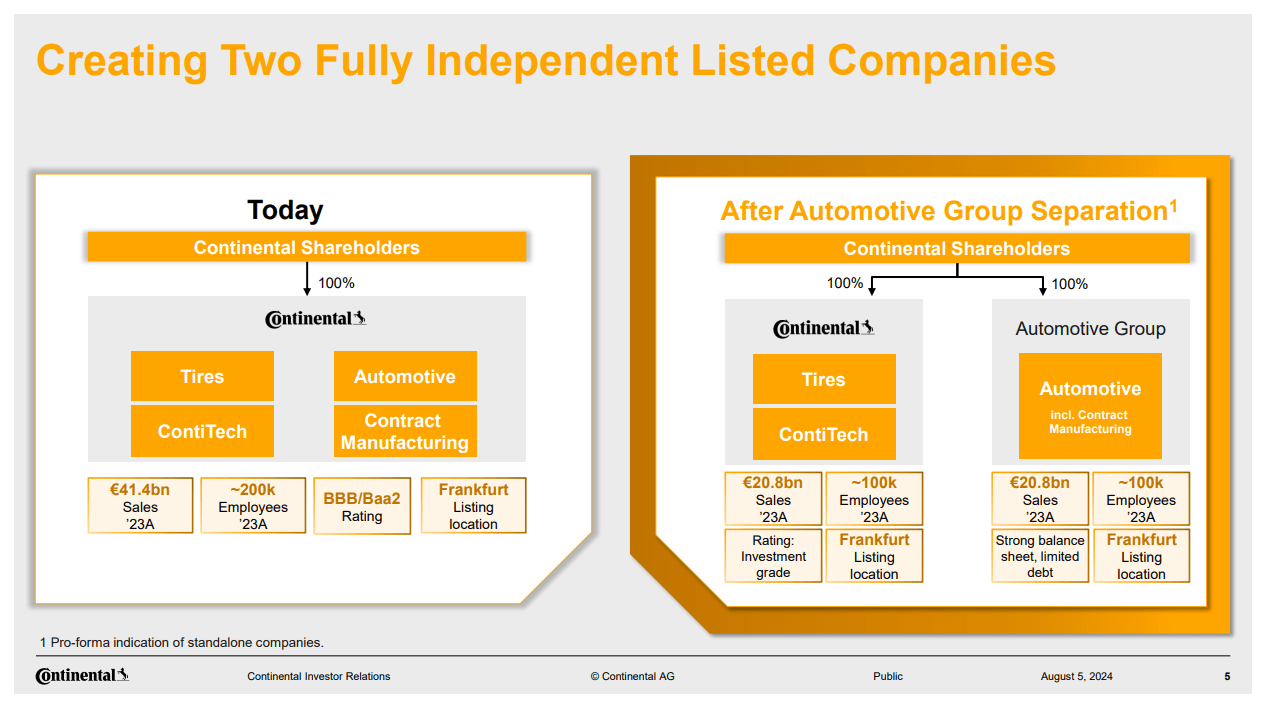

The spin-off was only recently announced. In a spin off the key data you want to be able to pin value to the individual parts is the debt figure because spin-offs should theoretically result in the same combined EV the day after the spin-off as the comprehensive entity the day before, and is a useful anchor to be able to make an assessment about whether newCo or the residual company’s stock are more interesting.

That data hasn’t been given yet and will depend on the business’ overall review, but other important data such as which parts of the businesses are getting split off are already detailed. In short, they are getting their automotive business away from their tyre business.

This makes some immediate strategic sense just because the tyre business has well-defined peers and industry valuation levels. Also, in terms of segment margins, at run-rates the Continental tyre business seems to be running at similar margins as peers in the industry, namely Bridgestone (OTCPK:BRDCY) and Michelin (OTCPK:MGDDF).

Spin off idea (Spin off presentation)

The ContiTech business will remain with the residual company. They make various products out of rubber and plastic used in industrial applications. It’s not particularly profitable and is also under strategic review, which again makes sense because it de-confounds the picture around the tyre business, which is most easily benchmarked and comped against peers.

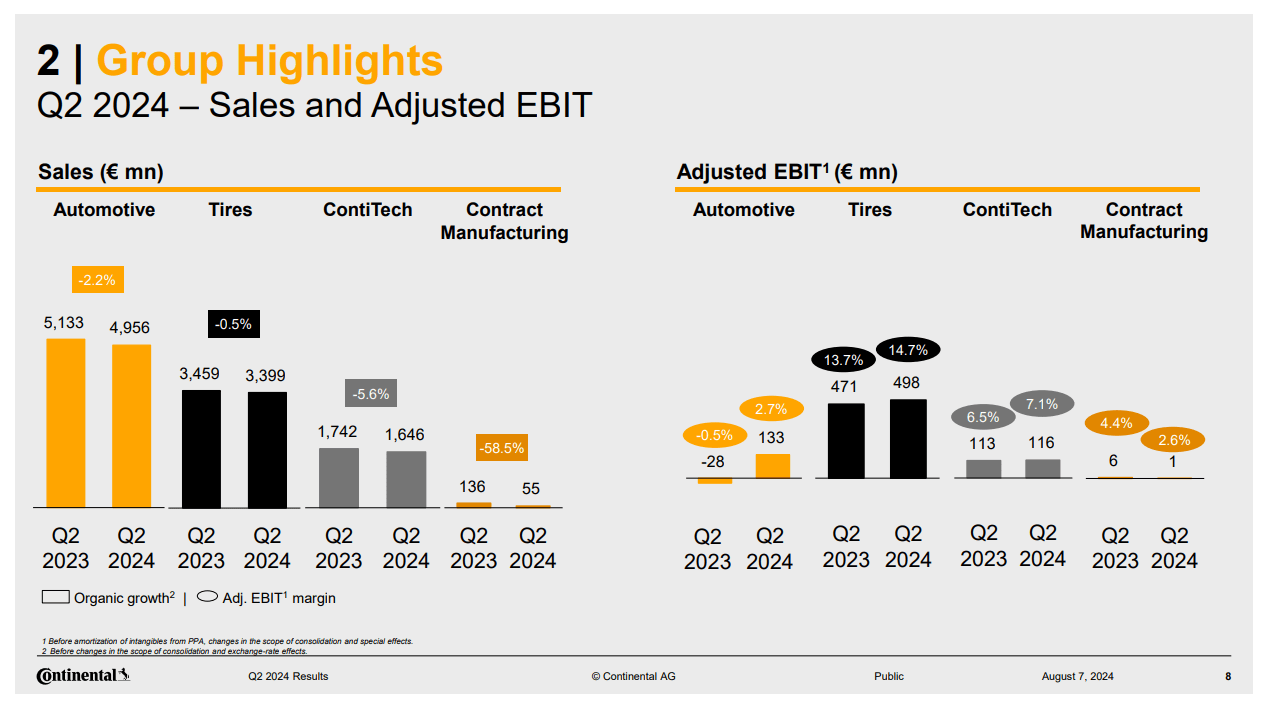

Highlights (Q2 Pres)

Automotive is under a fixed cost reduction programme which has allowed segment profits to grow. The growing areas have been architecture and networking, with a solid performance in safety and motion products and automotive mobility as well. These segments are involved in powertrain and chassis manufacturing, as well as brake systems. Product mix effects in architecture and networking also helped lift profits. These products are elements in the care designed for providing sensor data and connectivity.

As with Bridgestone, there was some trouble in the truck markets, but their lessened exposure to the US where the Thai imports wreaked the most havoc has helped them out in avoiding more serious performance hits. There was pricing pressure as input costs have also fallen, but general replacement demand has been decent, which is a key benefit to the tyre market. Longer term, if EVs indeed take hold, their greater weight will wear out tyres faster. Generally, volume was up. It was down for Bridgestone lately.

Automotive OE and general industrial OE in Europe is generally taking a hit, impacting tyres a bit as well but impacting ContiTech even more. Automotive OE levels in general are taking more of a hit in Europe than in the US, but the cheap imports are having a bigger impact on the US and the brands there. Continental is faring better with greater European focus.

Bottom Line

The earnings aren’t that remarkable, other than that they are not worse than peers. What we want to point out is that forward PEs for Continental are something like 8.56x based on analyst estimates. Bridgestone, which has been a bit of a laggard lately in performance, trades at a 10.4x forward PE. The implied valuation for the non-tyre businesses is extremely low for Continental, using Bridgestone as a comp. About 35% of income is from non-tyre businesses, whose implied valuation is around 5x forward PE assuming ContiTech should trade at tyre multiples (it’s quite small anyway). Taking Aisin (OTCPK:ASEKY) which does some of the same things that Continental does in the automotive business, they have a forward PE of around 8.89x, and they are a Japanese company which tend to be discounted compared to international peers who are listed on more efficient markets. There definitely seems to be a value case here, and the spin-off may address this discrepancy.

Given that multiples are actually quite low here in an absolute sense, and we are quite comfortable with the fact that tyres have replacement demand, we actually like Continental. It has also traded down to historically low levels. We think it’s a buy. As for which part we’d pick post spin-off, it’s too early to say obviously and will depend on investor behaviour after the spin-off (probably will dump newCo which is common).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.