Tom Werner/DigitalVision via Getty Images

Dealing with Slow Traffic: An Inescapable Reality

I recently started my ‘Goulart’s Restaurant Stocks’ follow-up on the family restaurant company First Watch (NASDAQ:FWRG) with the article entitled “First Watch Restaurant: The Price For Maintaining Pricing”. I highly recommend reading it, where I dissected the financial, operational and strategy structure used for the current restaurant industry environment.

That said, I also recommend checking out my other articles where I talk about the industry in general. In “Inflation Forces Quick Service Restaurants To Innovate Amid Less Foot Traffic” I dissected some unorthodox quick service restaurant management strategies that are helping companies maintain a steady pipeline of openings and restaurant-level economics to deal with a slow traffic environment. In another article called “Taking Advantage Of The Selloff: 2 Full-Service Restaurants I’d Like To Buy On The Dip” I talk a bit more about how some FSRs are successfully maintaining positive comparable sales through a specific factor called “Perceived Value”.

With that in mind, we saw in my last article about First Watch that the company made it very clear that it is not a discount brand. CEO Chris Tomasso said in the latest earnings call that the family restaurant and daytime dining company will continue to adjust menu prices and will not enter the ‘Value War’. Rather than adopting value promotions like the rest of the industry, First Watch would implement strategic menu price increases, menu innovations to drive visits from occasional guests, and use its database and paid traffic to segment and reach both occasional and non-occasional guests through its advertising efforts.

If you follow the restaurant industry, and particularly the full-service restaurant segment, you know that the strategy of keeping pricing the same in low-traffic environments is already being used by some brands. Most of them are managing to offset the drop in traffic by increasing the check per guest. This is for two reasons.

A company can increase the average check in a number of ways, such as by introducing more expensive items (such as menu innovations or premium items through barbell pricing) or by increasing menu prices. These changes will increase the price of the product mix, but if done in the simplest way (by increasing menu prices) they can have spillovers in traffic. That’s why we’ve seen some companies that want to increase the average check through barbell pricing and that effort actually pay off in practice. Examples include:

- At Burger King (QSR) management implemented both value promotions to bring back non-occasional guests with the $5 ‘Your Way Meal‘ and the premium ‘Melts‘ menu and ‘Fiery Menu‘ in July;

- Denny’s (DENN) recently brought back its new value promotion called the ‘$2, $4, $6, $8, $10 Menu‘. Additionally, the company aims to reach the other end of the spectrum of guests through premium products like the new Berry Waffle Slam and the Sweet & Smoky BLT&E;

- IHOP (DIN) advertises value for non-occasional guests through the $6 ‘2x2x2 Combo‘ and offers ‘BreakFEASTS’ for guests who are willing to spend more;

- Despite the risk of downselling with its mismatched promotional mix and LTOs, Applebee’s has value promotions such as ‘Two for $20‘, ‘All You Can Eat Appetizers‘ and ‘Endless Fries’ and more premium options such as the ‘Whole Lotta Bacon Burger‘;

- Burger giant McDonald’s (MCD) is offering the ‘$5 Meal Deal‘ as its main value offering until December, but it plans to add a new burger called the ‘Big Arch‘ that is already being piloted in Canada and Portugal. This beef burger will be the largest and most expensive on the permanent menu (if successful);

- Jack In The Box (JACK) is offering both value meals like ‘Munchies Under $4‘ and the return of ‘Jack’s Big Deal Meal’ as part of its revamped promotional mix. I covered this change in detail in my article “Jack in the Box: Redirecting The Promotional Mix, Still Undervalued.” As premium items, Jack offers its new Smashed line and burgers like the Bacon Swiss Buttery Jack;

- While Wendy’s (WEN) has the ‘Biggie Bag‘ as a permanent value menu item and breakfast options starting at $2, it also focuses on the barbell by introducing menu innovations like the Triple Berry Frosty and Saucy Nuggs;

- Chili’s (EAT) is enjoying a lot of success with its ‘3 For Me‘ value meal. Its design is designed to emphasize barbell pricing, as the promotion has three distinct price points ($10.99, $14.99 and $16.99). Management says only 18% of guests are in the $10.99 range. This ensures that incremental dollars aren’t lost and keeps the mix appealing to guests of all types;

- Dunkin’ Donuts, a brand owned by Inspire Brands, has a new value offering for the morning called the ‘$6 Meal Deal’ that consists of a bacon, egg and cheese sandwich, hash browns and a medium coffee. At the same time, Dunkin’ is betting on LTOs and seasonal fall menus to bring the park to life at other times (the Pumpkin Donut, Maple Sugar Bacon Breakfast Sandwich and other items are examples).

We could spend a lot of time listing examples of combining value promotions with premium items and menu innovations. This is the current industry paradigm and one of the most effective ways to present a product mix that appeals to both casual and non-casual guests.

The second way to increase the average check per guest is by leveraging the number of items per order. To achieve this goal, we need to understand how restaurants are approaching cross-selling strategies. A simple way to apply this concept in practice is through versioning, but there are other very effective ways. One of them is to find a specific price range that encourages guests to add unplanned items to their order. Below I have compiled some strategies of this type:

- While Jack In The Box’s ‘Munchies Under $4’ didn’t do much to bring back the occasional guest, it did serve as a great catalyst for increasing the average check. Management reported that guests were adding extra items in the $1 to $4 price range to their planned orders. This helped the company stem the decline in systemwide traffic and steady comparable sales at -2.2%;

- IHOP has an AI-based recommendation system in its app that offers lower-priced items as customers approach checkout. Management recently reported that implementing this system has boosted the number of items purchased per purchase;

- With the reintroduction of the ‘$2, $4, $6, $8, $10’ menu at Denny’s, the lower price points act to increase the volume of orders per guest. In this case, a guest could order a full meal in the $10 price range and top it off with specific items at $2 or $4;

- Wendy’s offers low-cost breakfast items, such as its recent $1 Honey Bud promotion. This also helps Wendy’s leverage digital sales and drive incremental dollars per breakfast transaction;

- Despite disappointing comparable sales, Del Taco (like Jack In The Box) implemented a value promotion called ‘Del’s Real Deal$’ at the end of the first quarter. The promotion, like ‘Munchies Unde $4’, did not drive traffic, but rather average check. With individual, value-priced options, items such as tacos, burritos, nachos and chips sell for $2 or less and served as a boost to existing orders;

- Sonic, another Inspire brand, also uses its value menu called the ‘Sonic $1.99 Menu’, starting at a very low price range to drive orders.

These are just a few strategies from an industry that is always on the move like the restaurant industry.

According to RMS, in limited-service restaurants the average check increase was 4.1% in August when compared to last year. This increase came from 3.8% due to the increase in the price of the mix (the first situation we described) and 0.5% in the quantity per transaction (second situation we described). I want you to notice that the majority of check growth needs to be achieved through an increase in product mix given how difficult it is to increase orders per transaction without running into a transaction that will eat into your restaurant’s margins.

As I have been warning here, the ability to increase menu prices is exhausted. That is, for every percentage increase in menu prices, there is some kind of spillover in traffic. However, there are some exceptions. Restaurants that have some kind of competitive advantage over their guests are able to achieve some degree of desensitization to this inverse relationship between traffic and price increases. This is where the ‘Perceived Value’ figure that I’ve been talking about so much here comes in. This is the holy grail of restaurants.

In my last article about Bloomin’ Brands (BLMN) I talked about this in more depth. Brands that have a positive perception of value in relation to their guests do not need to recover traffic and, consequently, do not need to go all out on value promotions. Sometimes the traffic is not even lost.

Take a look at some examples like Texas Roadhouse (TXRH) which in the last quarter showed a solid consecutive growth of 4% in traffic. According to Black Box Intelligence, the top quartile of brands with the highest traffic showed a growth of at least 1%. Meanwhile, the average full-service restaurant showed a decline of approximately 2.4%.

Other brands that have managed to show positive comparable sales despite slow traffic fall into exactly the same scenario we discussed earlier about traffic sensitivity to price increases. One interesting example is Chilli’s, which showed a 7.4% comparable sales growth last quarter. This was driven by an impressive 8% increase in average check per guest and a 0.6% decrease in traffic. Another example is The Cheesecake Factory (CAKE) with its strategy of rotating menus, innovations, and seasonality. Cheesecake saw 1.4% comparable sales growth last quarter, with traffic declining 0.2% and average check growing 1.6%.

Thus, by forgoing promotions, First Watch almost completely forgoes the chance to recover traffic from an incremental gain of non-occasional guests, even temporarily. In this case, a hook and build strategy could retain some of them, as clever companies have done before. Therefore, it is not true to say that promotions generate only incremental traffic, since loyalty is possible.

This indicates that management possibly sought to increase the average check per guest through direct and indirect strategies of increasing the quantity per order and the product mix, as discussed previously. Now that we have the problem, let’s examine the results.

Was the Price of Maintaining Pricing Expensive?

It’s always interesting to note that First Watch is a family restaurant brand that focuses on daytime dining. We know how traditional family restaurants are doing, and they’re not doing very well. I recently wrote an extensive article about this situation called “Denny’s: Value Strategy Tackles The Decline Of Family Dining.”

The first thing we notice is how different First Watch is from concepts like Denny’s, Cracker Barrel (CBRL), and even IHOP. All of these have shown declines or stable performances in recent years, while First Watch, which is at the beginning of its life cycle, is showing accelerated growth in the number of units, revenue, and operating cash flow.

The second point I would like to make is how First Watch is different from the rest of the industry in terms of the ‘Value War’. While Cracker Barrel is revamping its menu and restaurants in its ‘5 Pillars’ turnaround strategy, Denny’s is going deeper into value with its ‘$2, $4, $6, $8, $10 Menu’, and IHOP is doing the same with options like the ‘$7 Rooty Tooty Fresh ‘N Fruity’, all-you-can-eat pancakes, and the ‘2x2x2 Combo’.

That said, I’ll say up front that comparing First Watch to other family restaurants is not an easy task given the differences in life cycle and approaches to value. With some caveats and other bases for comparison, let’s look at how First Watch performed in its comparable sales during Q2 2024:

Author

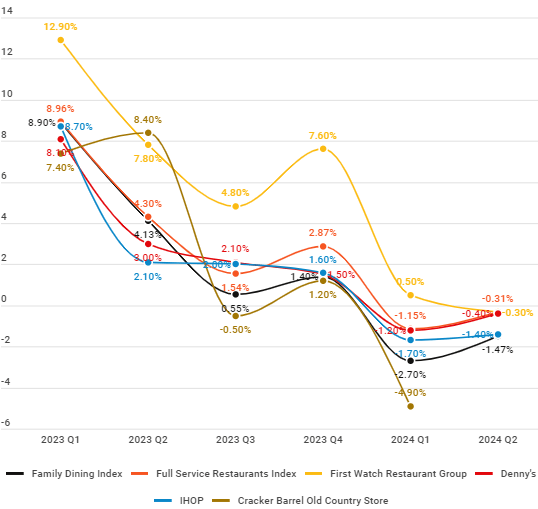

Note that during 2023, First Watch was growing its comparable sales at an impressive rate, even when compared to industry second- or first-quartile FSRs. This momentum appears to have slowed down during Q1 2024. Prior to this, guests were already decreasing their restaurant visits, but there was still some maneuverability regarding average check growth.

The traffic trajectory since Q1 2023 was as follows: 5.10%; -1.20%; -1.90%; 0.20%; -4.50%; -4.00%. Meanwhile, First Watch has reached the threshold for sustainable price increases. Now take a look at the average check per guest growth trajectory: 7.80%; 6.60%; 2.90%; 7.40%; 5.00%; 3.70%.

While it appears that comparable sales are stagnating due to this traffic sensitivity and inability to grow average check per guest without major issues, First Watch’s traffic situation doesn’t compare to the 8.3% drop at Cracker Barrel or other players that don’t disclose traffic data. What we do know is that Black Box estimates that family restaurants saw a drop of about 5.1% in traffic (1.1% less than the drop reported by First Watch).

In my opinion, aside from the demographic factors I explored in my previous analysis of family restaurants, the main reason traffic declined more slowly at First Watch was simply their segmentation.

In cases like Denny’s or IHOP, casual diners ended up switching from FSRs to QSRs during breakfast. QSRs like Wendy’s, Tim Hortons, Burger King, McDonald’s, Del Taco, Taco Bell (YUM), Panera Bread, Dunkin’ Donuts, Jack In The Box, and many others have all expanded their breakfast offerings in the wake of the pandemic. The need to move the park in the morning became a necessity as traffic declined, especially for concepts that weren’t set up for that task.

Because First Watch’s segmentation has always avoided discounts and focused on innovation and maintaining its premium pricing, casual guests have remained resilient to both inflationary pressure, substitute products and segments such as QSR trying to grab a share of this market.

This has proven to be a safeguard, but it hasn’t made comparable sales bulletproof. Traffic has been declining faster since Q1 2024, and based on industry and segment trends, comparable sales are expected to remain low. Reflecting this, in the latest earnings call the CFO adjusted the company’s guidance for comparable sales to a negative 2% to flat, with a mid-single-digit decline in same-restaurant traffic.

This means that First Watch, while resilient thus far, does not have a significant competitive advantage that would place it alongside the champions in perceived value of stable traffic, nor in the group of restaurants that can increase average checks to overcome declining traffic. This is my main concern about the strategic position of ignoring value promotions. That is, with current conditions deteriorating in the industry during August, would it be foolhardy to not adopt some tools to boost traffic?

In my opinion, the answer is yes. Guest weakness is likely to continue for some time to come, and maintaining a strategy that doesn’t include value promotions if you’re not a restaurant with check/traffic resilience is risky. I say this based on the most recent industry data.

- August CPI shows that eating out prices have outpaced eating at home prices by 3.1% year-to-date. That’s about 2.5% above the historical average of 0.6%. That gap is second only to what we saw in 2016, which was 3.9%, and that was a terrible period for the industry as a whole;

- RNA’s Restaurant Performance Index (RPI) indicated a decline in both the current situation and expectations for the industry in July. During the month, the Current Situation Index fell from 98.9 in June to 97.7 in July (numbers below 100 indicate pessimism). The Expectations Index fell from 99.8 to 98.4, marking the tenth consecutive decline;

- Also according to RNA research, only 20% of operators reported higher comparable sales during the month of July compared to last year. This result was the second worst of the year, behind only January. This research also reported that in no month this year did the majority of operators record better comps this year than last year, with May being the closest month; About 37% of operators expect lower sales in the next six months and 46% of them predict worse economic conditions in the next six months. This is the worst forecast in the last 12 months;

- We saw deterioration across nearly every component of the CSI. Comparable sales are at 95.7, down 2.3 from June. Traffic is at 94.2, down 1.5 from June. Labor is at 97.5, just 0.7 behind June. Capex is at 100.2, down 0.5 from June but still above 100; According to RMS data, QSR traffic is about 2.1% higher in August than it was a year ago. In addition, prices in this segment increased 3.8%, a substantially slower increase than the double-digit growth we saw last year, supporting my thesis of stagnant and declining comparable sales.

Now that I have shown the danger of maintaining a rigid strategy in a volatile environment and why I do not endorse it, let’s take a look at Q2 developments.

Q2 Developments: Acquisitions, Debt and Strategic Positioning

In Q2 2024, First Watch reported top line sales of $258.6 million, up approximately 19.5% from the same period last year and approximately 6.7% from the previous quarter. Approximately $21 million of this revenue came from 21 restaurants acquired from franchisees in the Raleigh-Durham area, or approximately 8.1% of total revenue. As of the acquisition, these 21 restaurants will be company-operated, meaning that all revenue and operating costs will be borne by First Watch. The Company’s EBITDA was $32.1 million, up approximately 38% from the same period last year and 24.4% from the previous quarter. The impact of the acquisitions on EBITDA was $5 million, or 15% of total EBITDA. On average, Raleigh-Durham restaurants contributed $1 million each to revenue and $238,095 each to EBITDA.

In addition to the acquisition, First Watch also purchased the development rights in the area previously agreed upon with franchisees through unit development commitments. The total amount paid was $73.7 million. Because this acquisition supported the company’s operating cash flow for the quarter by 2.3 times and the company also incurred nearly $30 million in capital expenditures, First Watch had to issue $97.5 million in debt. This helped the company maintain $45.1 million in cash on hand, similar to its historical levels.

Based on the assumptions that the acquired restaurants are all mature (>3 years of operation), generate approximately $2.6 million of AUV and have a margin of 20% each, acquiring the restaurants for $73.7 million, paid entirely from third-party capital at a cost of 7.9% and modeled by perpetuity at 2% growth, we find the following information:

- The present value of the cash flows from the 21 units added together is $163.346 million. The NPV is $89.646. This indicates that the project increases the value of the firm and not the other way around. Even when we exclude perpetual growth, we find an NPV of approximately $57 million;

- If revenues remain stationary at unit level, the project’s payback is approximately 7 years, however, if we consider growth based on historical data, the payback would be only 4-5 years;

- The Benefit-Cost Ratio is 1.78-2.38 (depending on realistic assumptions of perpetual growth);

- The IRR for this project ranges from 14% to 16% based on the above assumptions. This is about 4% to 3% lower than greenfield units. However, for comparison purposes, the IRR for both the greenfield units and the units acquired in April are higher than for projects in the pipeline of companies such as Applebee’s (IRR of 14.5%), legacy BJ’s Restaurants (BJRI) units (IRR of 15.8%), and other full-service restaurants.

It is interesting to note that in the financial modeling I did not consider development rights as part of the deal, as they are essential to maintaining First Watch’s presence in the Raleigh-Durham area, but unfortunately cannot be quantified without access to the undisclosed agreements.

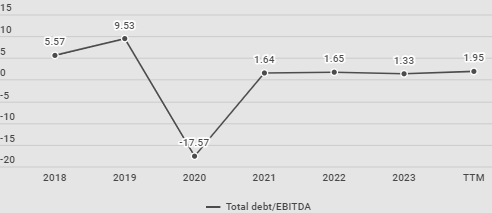

With the debt, First Watch now has approximately $188.6 million in long-term debt on its balance sheet. This represents a 105.8% increase over the same period last year and a 58.2% increase over the last quarter.

Author

However, even with the increase in debt, when we measure its impacts based on the increase in EBITDA, the Debt/EBITDA Ratio only rose from 1.33 to 1.95. This is because third-party capital has already been allocated and is now generating a larger EBITDA, mitigating the effects of debt and financial and economic risk. These effects should be even more diluted by the end of 2024, since to measure the last variable I used the EBITDA of the last 12 months. I estimate that with a projected EBITDA of $117.736 million for the full fiscal year 2024, and assuming that debt remains the same, the ratio would be 1.60, in line with what we saw in 2021.

I don’t see any problems with the current debt levels. But there is a risk associated with the individual performance of these restaurants and how they will perform in a value-driven environment, as I explained in the first part of this analysis. However, if First Watch maintains comparable sales within the range they established in the guidance (-2% to flat SSS) I don’t see any structural risks, just a lackluster performance.

Now, turning to openings in the quarter, First Watch opened seven new restaurants in six states. Six of those restaurants are company-owned and only one is a franchise. That brings the total systemwide total to 538 restaurants at the end of Q2. As I said in my last analysis, management estimates that there is an addressable market of 2,200 units for First Watch over the long term. That would represent a 308% growth in total units. We know that First Watch develops the majority of its units, which means that to achieve that goal, the company will need to continue to have a high capital expenditure burden.

Currently, the company said that about 130 units are in some stage of development. That represents about 25% of First Watch’s total system, meaning the company will continue to grow its number of units at a rapid pace in the coming quarters, regardless of the macro scenario.

Even though I am not yet concerned when I look at the ratio between total debt and EBITDA, as well as the Debt Efficiency and Financial Leverage indicators, there are still reasons to believe that the debt will continue, increasing both Economic Risk (taking into account RNA’s forecasts for the industry environment and First Watch’s positioning in relation to the promotional environment) and Financial Risk. The company continues to generate insufficient operating cash flow to cover its investment activities. Since the company prioritizes the development of its units from scratch and should continue on this path, I see the debt increasing in the medium term.

Another development we had during Q2 2024 was the improvement in labor costs. In my last analysis of First Watch, I pointed out this as one of my biggest concerns. Since the restaurant only operates during the day, I had already pointed out some bottlenecks in its management of staff during peak hours and queues.

During Q2 2024, First Watch, in addition to improving its working time bank system, also developed a table reservation system. This platform has already been tested and will be implemented during Q3, which will also alleviate some labor costs and reduce the chances of ‘clopenings’. Even though I think these developments could be implemented sooner due to the “No Night Shifts Ever” philosophy, better late than never. I’m looking forward to seeing how this system works during weekend brunches, as that’s when traffic hasn’t backed up to First Watch.

For now, First Watch relies on its real-time timekeeping system and workforce management tools to predict peak times in advance, much like BJ’s Restaurant has implemented. This has helped First Watch reduce labor costs from 33% of revenue during the past quarter to 32.8%. That’s above the ‘30/30/30 Rule benchmark’, but in line with other restaurants.

First Watch will be working tirelessly throughout the rest of the year to get its everyday value message in front of the right guests. Since the company is unlikely to join the giant group of restaurants that are launching their value meals, management plans to make its communications more effective for its target audience. That’s the ‘First Watch Way,’ according to management.

To target more precisely, First Watch has amassed an opt-in database of approximately 7 million guests (both occasional and non-occasional). This database will be amplified using the reservation and queue management system I mentioned earlier. Once a specific pattern of potential guests has been identified, First Watch intends to “target demand generation across our own communications channels as well as paid digital media.”

My Recommendation

I really don’t believe that segmentation efforts will help First Watch gain share in a highly price-sensitive and extremely value-sensitive market. This is reflected in the pessimistic guidance for the rest of the fiscal year.

The truth is that First Watch, when compared to other family restaurants, seems to me to be a rising concept in a declining segment. However, in my opinion, this does not justify the current pricing levels.

Let’s take a look at the multiples, so I can better explain my view of the company. I’ll use about eight metrics for comparison purposes: P/E, EV/EBITDA, P/S, P/CF, P/B, EV/EBIT, PEG Ratio, EV/S. For comparable companies, I’ll use other family restaurants, such as Cracker Barrel, Dine Brands, Denny’s, and casual restaurants like BJ’s Restaurants and Texas Roadhouse.

Averaging the above models and using these comparable companies, we get a target price of approximately $14.30. However, when we look at more appropriate metrics for valuing growth companies such as P/S and EV/EBITDA, we find a target price of $12.50 to $13.50. This is below the current value of the stock.

Looking at the DDMs, we also observe an overvaluation of the stock. To do this, we will consider the Modigliani-Miller Hypothesis about the irrelevance of the dividend policy since the company does not pay dividends.

Using the SPDDM model and considering the discount rate of 6.79%, we need to make some assumptions about the two cash flows to shareholders that we will discount to present value. The first one is D1, which in normal situations would be the dividend of year 1. Here, we use the estimated EPS for the fiscal year, which is $0.36. For the second cash flow, we will use the estimated sale price of the stock in year 2. Assuming that the P/E for FWRG is 41.69, we obtain the exit price of $15.01. Discounting these cash flows to present value, we have a target price of $14.39. We can use both ends of the EPS estimate to obtain a range in the SPDDM. This gives us a price target of $12.05 (using EPS=$0.30) to $17.12 (using EPS=$0.43).

Let’s look at DPDDM and make the same assumptions about the discount rate and cash flows to the shareholder in year 1. For year 2, I will assume an EPS of $0.42 and an exit price of $15.09 (assuming a P/E of 35.94 in 2025). This gives us a total of 3 cash flows: year 1 dividend, year 2 dividend and exit price. Discounting these three cash flows to present value gives us a target price of $14.03. Considering the sensitivity of EPS in year 2 in the same way that I analyzed the sensitivity of this factor in SPDDM, we obtain a range of $12.09 (using EPS2=$0.36) and $15.33 (using EPS2=$0.46).

Note that in both metrics, the upside potential is not that appetizing, which signals a possible overvaluation by more than three valuation metrics. It is really difficult to value a growth company, and far from being an intrinsic problem of First Watch, this problem affects players such as Dutch Bros (BROS), Kura Sushi (KRUS), CAVA (CAVA), and many other restaurants that have gone public in the last ten years.

As in my last analysis of the company, I prefer to stick to simpler valuation methods and make fewer assumptions than to build a DCF for First Watch. There is the whole problem of estimating when the company will generate free cash flow, and to do so we would need to estimate margins and investments in operating assets that are always volatile in growth companies since they always need to maintain working capital.

That said, I maintain my ‘Hold‘ recommendation for First Watch and set a target price between $13.50 to $14.50 based on the models presented above.

The concept has proven to be relevant, but I don’t believe they will be able to continue performing as well as they did in 2022 and 2023 with the strategic approach of completely ignoring promotional environments. In my opinion, First Watch will show negative comparable sales in the low single digits in both Q3 and Q4.

We have seen that few restaurants that have a certain competitive advantage can succeed with this strategy. These are the kings of ‘Perceived Value’. This is not the case for First Watch. I say this based on traffic and average check per guest data, since both have been contracting in the same direction since Q1 2024.

Why not further deepen the barbell strategy? That way, if well implemented, the company would be able to boost traffic without compromising its margins. Well, First Watch could even use its new database firepower and boost segmentation to avoid the risk of selling down. This risk would be eliminated, since the guests who would order the promotional items would be non-occasional. We learned from Chili’s that you can pull two levers at once and still grow your check by double digits. Even as it targeted value with its ‘3 For Me’, for example, the company focused on menu innovations like the new Big Smasher Burger and improved operational efficiency with AI-based labor control and Ziosk tabletop order processing tablets.

We have seen that some companies that did not have affordable full meals in their promotional mix are adopting this recently. BJ’s Restaurant, which like First Watch was considering keeping its promotional mix without many value offers, recently changed its mind and launched its ‘Pizookie Meal Deal’ for $13. Even Applebee’s, which was selling at a low price with its large LTOs, had to launch the ‘Two for $20′ to balance its promotional mix. We know that guest inertia punishes timing errors in launching promotions, and those who are confident in providing value to the guest end up gaining market share from those who are slow to do so.