:max_bytes(150000):strip_icc():format(jpeg)/penaltyfree-way-get-529-money-back-v3-8144da01f0d84eb78b614c352d797e78.jpg)

A 529 plan can be a great way to save money for college, as earnings are generally exempt from federal and state income taxes if used for qualified education expenses. However, withdrawals from these accounts for non-qualified education expenses can be subject to taxes plus an additional 10% penalty. Fortunately, this penalty doesn’t apply under certain circumstances, such as when the beneficiary receives some form of tax-free educational assistance.

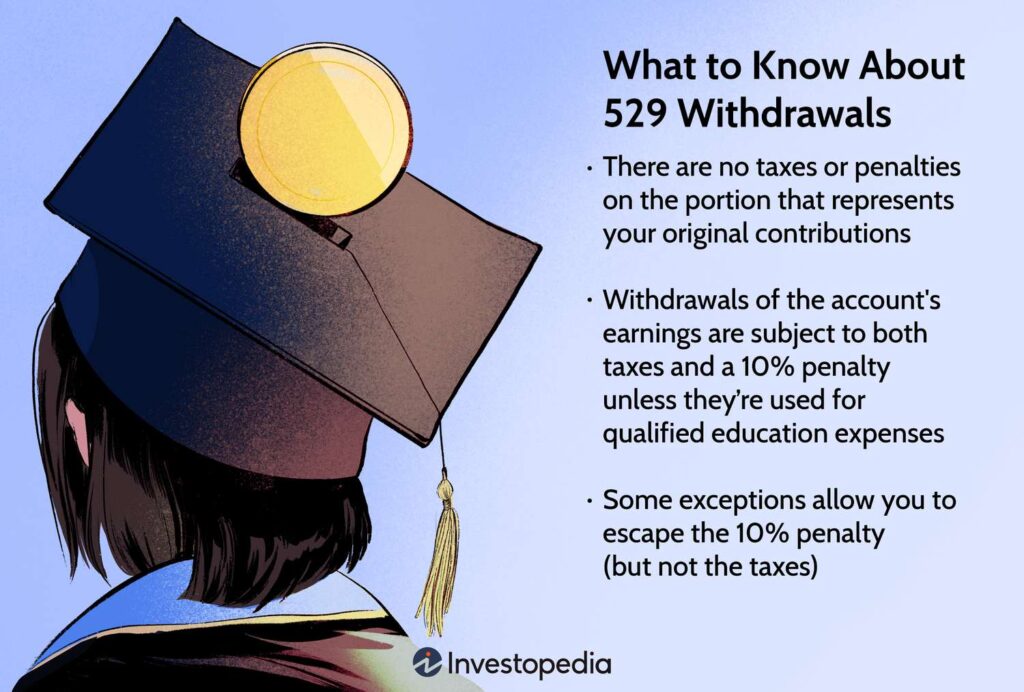

Key Takeaways

- A 529 plan is a tax-advantaged account used to save for qualified education expenses, lessening the need to rely on student loans.

- If the account’s beneficiary receives any form of tax-free educational assistance, then a distribution of up to the amount awarded won’t be subject to the 10% penalty on non-qualified expenses.

- As it isn’t entirely clear when this exception can be made, the safest bet is to make a withdrawal prior to the end of the calendar year that the educational assistance was granted.

529 Plans: The Basics

A 529 plan, formally known as a qualified tuition program (QTP), is a type of tax-advantaged account that offers a way to save for educational expenses. Although the basic framework for these plans was devised at the federal level, the states determine the specifics of their respective plans, such as what the investment options are and whether there are any tax benefits.

Because a 529 withdrawal usually isn’t subject to income taxes, parents often open these accounts on behalf of their children to grow their college funds tax free. One type of 529 plan, called a prepaid tuition plan, can even be used to essentially prepay for future attendance at select institutions based on today’s tuition rates.

Anybody can set up a 529 account, so you could open one and name yourself as the beneficiary if you so choose. This can be a good option if you want to save money to attend grad school.

While 529 plans are primarily used to pay for college, changes in legislation over the years have expanded how these funds can be used, such as the Tax Cuts and Jobs Act (TCJA) allowing withdrawals of up to $10,000 per year to pay for K–12 tuition. Another example is the Setting Every Community Up for Retirement Enhancement (SECURE) Act permitting distributions to repay qualified student loans, up to a lifetime maximum of $10,000.

Consequences of Non-Qualified Withdrawals

Since they’ve already been taxed, 529 plan contributions can always be taken out tax free. However, when 529 funds are used to pay for non-qualified education expenses, the earnings portion of that withdrawal may be subject to income taxes and an additional 10% federal tax penalty.

Unfortunately, because distributions are allocated pro rata between a plan’s contributions and its earnings, you cannot make a contribution-only withdrawal.

You may also have to pay income taxes and the 10% penalty if you exceed any distribution limits, even if the money was technically used for a qualified education expense. For example, if you withdraw a total of $12,000 in a single year to pay for your child’s high school tuition, that’s $2,000 over the $10,000. You would then owe taxes and a 10% penalty on the earnings portion of that excess amount.

Options for Penalty-Free Non-Qualified Withdrawals

If you make a 529 withdrawal for a non-qualified education expense, there are certain circumstances where the 10% penalty won’t apply (though taxes still will). These include:

- The beneficiary dies or becomes disabled

- The beneficiary attends a United States military academy (not exceeding the costs of advanced education)

- The qualified education expenses were only taxed because the student or parent(s) claimed the American Opportunity Tax Credit (AOTC) or Lifetime Learning Credit (LLC)

- The beneficiary received any kind of nontaxable educational assistance (other than gifts or inheritances), including scholarships, fellowship grants, veterans’ educational assistance, and employer-provided educational assistance

Beneficiaries can avoid paying income taxes as well as the 10% penalty by rolling over a lifetime maximum of $35,000 from a 529 plan into a Roth individual retirement account (IRA), subject to annual contribution limits, so long as the 529 plan has been open for over 15 years.

Another possibility would be transfering the funds to an Achieving a Better Life Experience (ABLE) account, also subject to annual contribution limits. This is only an option for those who’ve been diagnosed with significant disabilities prior to their 26th birthday.

The Educational Assistance Exception

If you open a 529 account for your child and they’re later granted some form of nontaxable educational assistance, that may mean having more funds saved than are needed to cover their qualified education expenses. Fortunately, you can withdraw an amount up to the awarded value from the 529 plan and use the money for any purpose, without paying the 10% penalty.

The major downside of this exception is that it would result in the student having a lower adjusted qualified education expenses (AQEE), or their total qualified education expenses during an academic period minus any tax-free educational assistance they received. Making a 529 withdrawal in excess of the AQEE results in the earnings portion of that distribution becoming taxable. You still wouldn’t owe the 10% penalty, just income taxes.

The Internal Revenue Service (IRS) also doesn’t clearly spell out when 529 funds have to be withdrawn in order to count toward this exception. However, to be on the safe side, consider making the 529 distribution before the end of the same calendar year that the scholarship funds were awarded, suggests Larry Sprung, CFP, founder of Mitlin Financial.

“Although there is some ambiguity regarding the timing, I think taking a more conservative approach is better,” says Sprung. “I would also recommend that you maintain clear records of what amount was distributed, when, and for what calendar and school year. It would also make sense to confirm your strategy with your tax professional, so you are both on the same page as well.”

The Bottom Line

A 529 plan can be a great way to save for college while minimizing taxes, and there are options for accessing these funds even if you end up needing less money for school than anticipated.

In particular, not only does securing tax-free educational assistance reduce your college costs, it also gives you an opportunity to withdraw an equivalent amount from your 529 plan—without paying the 10% penalty on non-qualified distributions. You may still end up owing income taxes in this situation, but you’ll still be able to retain more of your 529 earnings than you might’ve otherwise.