:max_bytes(150000):strip_icc():format(jpeg)/Pros-and-cons-health-savings-account-hsa_final-32c82ecfb53340739b46e7bb0d13b18e.png)

A health savings account (HSA) is a tax-advantaged savings account for medical expenses like doctor visits, prescription drugs, and dental care. You can open an HSA if you enroll in a high-deductible health plan (HDHP).

High deductibles mean higher out-of-pocket costs, but your HSA contributions and withdrawals for eligible expenses are tax-free. This could save you money in the long term, especially if you have significant medical needs.

Key Takeaways

- HSAs allow you to pay for qualified medical expenses using pre-tax income, which could save you money on out-of-pocket health care costs.

- Unlike comparable savings plans, such as flexible spending accounts and health reimbursement arrangements, you can continue using your HSA to pay for medical expenses after you leave your job.

- You can only get an HSA if you have a high-deductible health insurance plan.

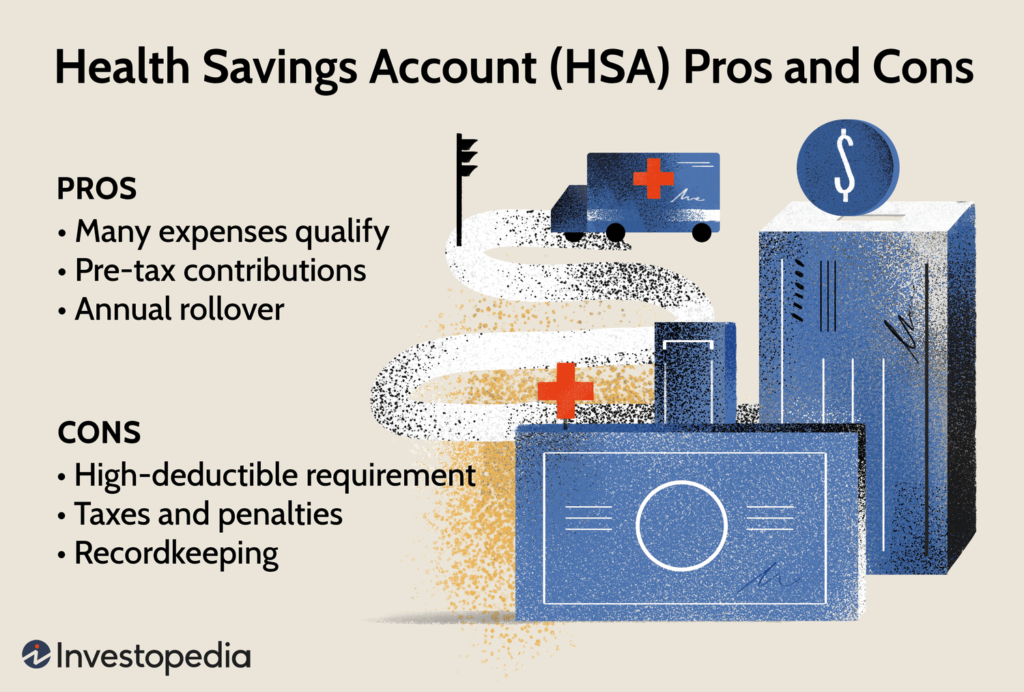

Advantages of an HSA

HSAs have substantial benefits compared to other types of health coverage.

HSAs Pay for Many Types of Medical Expenses

Your HSA can pay for copays, coinsurance, and other health care costs not covered by your health plan. Besides standard doctor visits, your HSA can also cover vision and dental care, prescription drugs, over-the-counter health products, family planning expenses such as contraception and fertility treatments, and even menstrual care products. You can find the full range of qualified medical expenses on the Internal Revenue Service (IRS) website.

In addition to these medical expenses, the HSA may also cover limited types of insurance premiums. For example, if you lose your job and buy COBRA coverage, those premiums are HSA-eligible expenses. So are the premiums you pay for health insurance coverage while you receive unemployment compensation. Medicare premiums, although not those for Medicare supplement insurance (i.e., Medigap), are also eligible if you’re 65 or older.

HSAs Have Tax Advantages

When you contribute to your HSA, the money comes from your paycheck before taxes are taken out. This lowers your taxable income. In other words, if you earned $70,000 and put $5,000 into your HSA, you’ll only owe income taxes on $65,000 for that year. This can save you money during tax time.

You can also make after-tax contributions to your HSA and claim these as deductions when you file your federal income tax return.

Distributions from your HSA are also not taxed as long as they’re what the IRS considers “qualified” distributions. A qualified distribution (or withdrawal) means the money was used for eligible medical expenses. A non-qualified withdrawal could result in a 20% tax penalty.

If you’re over 65, you can withdraw money from your HSA for any reason without paying a tax penalty, although you’ll still owe income tax on the withdrawal if the money is used for non-medical expenses.

You Can Take Your HSA With You When You Leave Your Job

Your HSA is yours to keep, even when you leave your job. You can usually continue contributing to it if you maintain HSA-eligible health insurance. This portability sets the HSA apart from the similarly structured flexible spending account (FSA) and other employer-sponsored savings accounts, such as the 401(k).

Your HSA will last even in retirement. You can reimburse yourself for eligible medical expenses incurred at any time if you maintain proof of the expense, such as a receipt. The money in the HSA never expires.

Your HSA Works Alongside Other Investment Accounts

When you turn 65, you can take money out of your HSA tax-free to use as retirement income. In this way, the HSA complements your other retirement accounts. It combines the tax-free savings of a 401(k) or traditional individual retirement account (IRA) while you’re working, and the tax-free withdrawals of a Roth IRA when you retire.

The investment opportunity is especially attractive if you’ve reached your annual contribution limits on other retirement accounts. Even though you can’t contribute as much to an HSA as you can to 401(k) or IRA, it can still boost your overall savings.

You can use your contributions to purchase the same types of financial assets as more traditional retirement accounts, including stocks, bonds, and exchange-traded funds (ETFs).

Disadvantages of an HSA

An HSA may help offset health care costs, but it may not be the best solution for everyone.

You Can’t Get an HSA Without a High-Deductible Health Plan

Your health insurance deductible is the amount you pay for covered medical expenses each year before your insurer starts to pay. The higher the deductible, the more you’ll spend out of pocket. In 2025, HDHPs are defined as having a deductible of at least $1,650 for individuals or $3,300 for families. However, many HDHPs have higher deductibles, often more than $3,000 for individual coverage.

The trade-off is that HDHPs generally have lower premiums. Thus, if you have expensive health care needs and expect to meet your annual deductible, you could save money you would’ve otherwise spent on higher premiums.

But if you only go to your general practitioner or the occasional specialist throughout the year, your out-of-pocket expenses will quickly add up. While your HSA contributions should cover these costs, you may prefer for your health insurance plan to cover major medical expenses directly, even if it means paying higher monthly premiums.

Most of the Value of an HSA Comes From Contributing a Lot of Cash

In 2025, you can put up to $4,300 in your HSA if you’re single or $8,550 if you have a family. These contributions never expire—you can use the money anytime, even years later. However, maximizing your contributions means you might have less money for other investments, including retirement accounts and cash savings.

Since you can only use these contributions for qualified medical expenses, you’ll only build up savings if your medical costs are lower than what you put in your HSA. If you have a severe illness or medical emergency, you could drain what you added to your HSA and still pay high excess out-of-pocket costs if you haven’t met your deductible.

There Are HSA Taxes and Tax Penalties

If you use HSA money for something other than qualified medical expenses, you may have to pay income tax and an additional 20% tax on the amount. The distribution will be reported on your tax return (Form 1040).

There are no exemptions for the income tax requirement for non-qualified distributions. However, you (or your estate) will be exempt from the 20% penalty if the distribution is made after you turn 65, become disabled, or die.

These rules are stricter than for other investment accounts, such as the 401(k) and 403(b), which allow for a taxable but penalty-free early withdrawal to pay for sudden financial hardship.

HSA Alternatives

Two alternatives to the HSA are flexible spending accounts (FSAs) and health reimbursement arrangements (HRAs). These plans generally cover the same expenses, though there are some exceptions, such as certain health insurance premiums covered by the HSA.

The FSA works like an HSA in that contributions are made with pre-tax income, and distributions are not taxed if used for qualified medical expenses. However, these differ from HSAs in two crucial ways:

- You can start an FSA regardless of the health plan you choose.

- Unused contributions don’t roll over to the next year unless your FSA expressly permits it (not all do). The IRS limits the amount that can be carried over. The carryover limit was $660 for contributions rolled over from 2024 into 2025.

Your employer funds an HRA, which can only be used for qualified medical expenses. Your employer’s contributions don’t count toward your income, so you’ll never have to pay taxes on them. But if you use the HRA to pay for a non-qualified expense, you must pay income tax.

You can roll over the balance of an HRA to the following year, but there’s a limit to how much you can be reimbursed during a given coverage period.

How to Make the Most of Your HSA

Try to contribute the maximum amount to your HSA each year. This helps ensure you’re covered for regular checkups, specialist visits you expect, and any emergencies requiring more painful expenditures. Any money you don’t use stays in your account and can become a nest egg for retirement.

Note

A 65-year-old retiring this year can expect to spend an average of $165,000 in health care and medical expenses throughout retirement.

Invest according to your risk tolerance: Because your HSA allows you to invest your funds, you can invest in slow-growing, less risky financial assets (such as ETFs) or faster-growing, potentially more volatile ones (such as stocks). Make sure you understand your own investing goals, including saving for retirement or preparing for significant health costs.

The Bottom Line

Open enrollment happens every year, which allows you to weigh the pros and cons of your health insurance options. While your HSA can help reduce the burden of high out-of-pocket costs from an HDHP, those costs might be lower with a different plan. A higher-premium plan might be worth lower out-of-pocket expenses.

On the other hand, an HSA could help you meet your long-term saving and investing goals while simultaneously covering you in the event of a large medical bill. Ultimately, its value depends on how much you can contribute.