Pixelbizz/iStock Editorial via Getty Images

The European GRANOLAS stocks were strong performers in 2023 and through much of this year. The group, made up of GSK, Roche, ASML, Nestle, Novartis, Novo Nordisk, L’Oreal, LVMH, AstraZeneca, SAP and Sanofi, is akin to the USA’s Magnificent Seven. The parallel isn’t perfect, but they are primarily high-growth large-caps that have rewarded investors over the past few years.

I’m going to focus on ASML (NASDAQ:ASML) today. I reiterate a hold rating given its growth path and a mixed technical situation. Shares will be in play this week when fellow semiconductor industry company NVIDIA (NVDA) reports its second-quarter results.

ASML is about flat since my initial hold rating back in the first quarter. Despite a pair of bottom-line beats and generally bullish price action in Europe over the past six months, not to mention a weaker US Dollar Index, ASML has not been able to get much traction, though shares did notch an all-time high in July above $110.

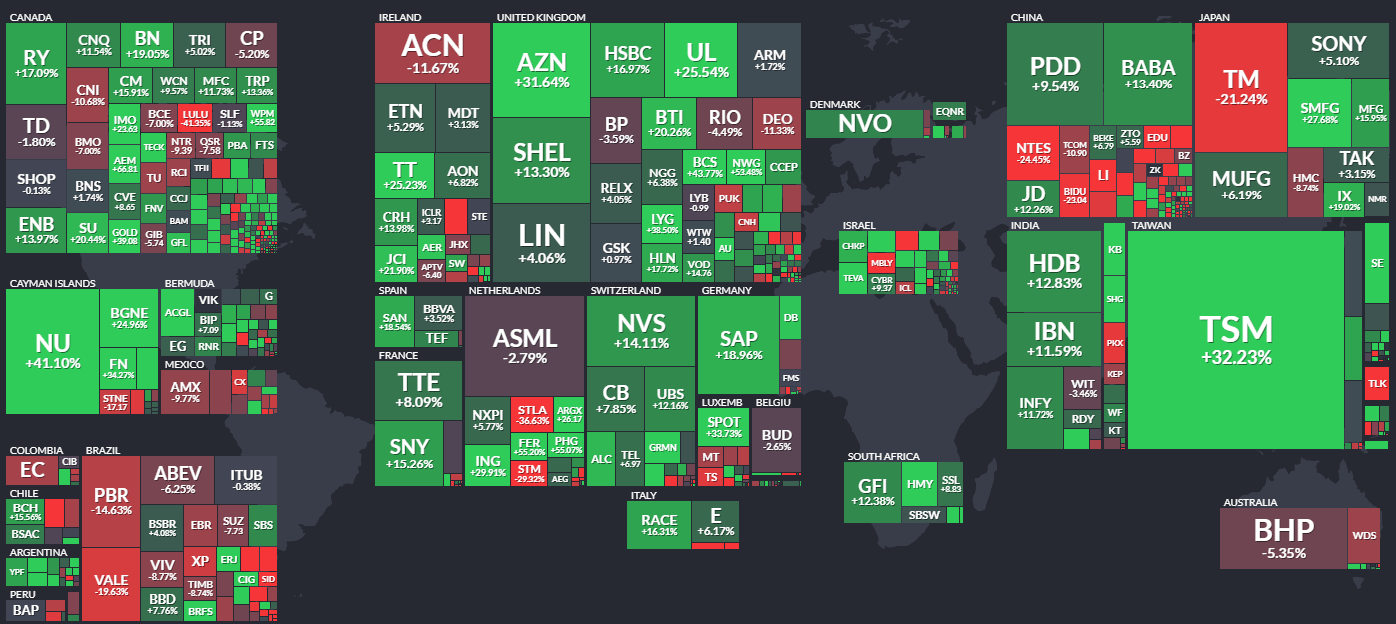

International Stock Performance Heat Map Last 6 Months

Finviz

According to Bank of America Global Research, ASML is the market leader in lithography tools, a critical part of the semiconductor manufacturing process enabling ‘Moore’s law’. The company benefits from technological transitions as well as new additions in leading-edge logic and memory chip capacity. ASML currently has a market share of close to 90%, which is a monopoly in next-generation EUV (extreme ultraviolet) lithography. The company holds critical relationships with clients like TSMC, Intel, and Samsung.

Back in July, ASML reported a solid set of quarterly results. Q2 operating EPS of $4.39 was a $0.36 beat while revenue of $6.8 billion also topped analysts’ estimates. The management team initiated Q3 guidance and reaffirmed its FY 2024 earnings outlook within the report. While revenue was down 10% from the same period a year earlier, net sales for Q2 came in ahead of the midpoint of the company’s forecast while its gross margin ticked to 51.5%, also modestly above what ASML anticipated.

Strong systems sales helped the quarter even though this year is seen as a transition period for the $360 billion market cap Netherlands giant. Quarterly net books amounted to €5.6 billion, and the chips company expects third-quarter net sales to verify between €6.7 billion and €7.3 billion and a gross margin between 50% and 51%.

There continues to be strong demand for its Logic and Memory areas, leading to a growing total addressable market worldwide. What I like fundamentally is that ASML’s executives are focused on cost management to keep up its margins. So long as the global economy stays on a decent footing, then order intake should be healthy across the cyclical semiconductor industry. Also encouraging, ASML’s latest breakthrough in its chip-printing machine helped support shares earlier this month.

Key risks include growing competition from other international Semiconductor Materials & Equipment players as well as the chance of slower economic growth in 2025. EUV lithography delays could hamper profits if there are delays in that space. Finally, corporate capex tends to be quite cyclical which could result in volatile sales and earnings. ASML also has exposure to China, which was a bearish catalyst earlier this summer, but BofA sees potential upside given news of potential export rules benefiting the company.

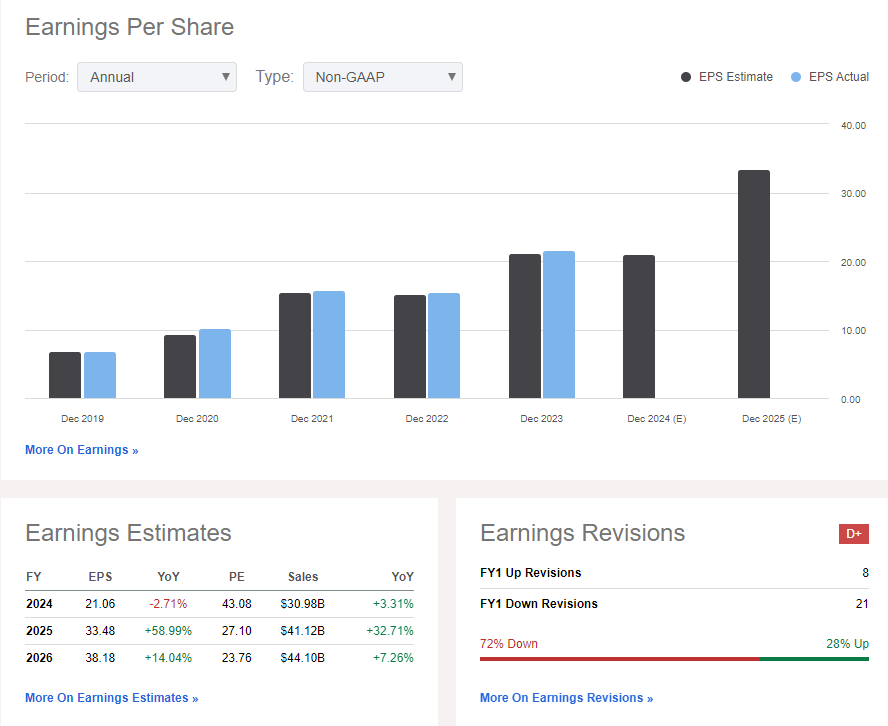

On the earnings outlook, ASML is expected to post a modest EPS decline this year but 2024 is forecast to see strong operating per-share profits. By 2026, the firm could reach $38 of EPS while sales growth jumps from $31 billion in 2024 to $41 billion in the out year. Mid-to-high single-digit top-line advances may persist thereafter. ASML’s free cash flow yield is low, below 1%, but analysts at Goldman Sachs expect the FCF yield to reach 4% by year-end 2025.

ASML: Big EPS Growth On Tap in 2025

Seeking Alpha

On valuation, if we assume $27 of 2025 operating EPS, which is about where the consensus stands today, and apply a 35 multiple, slightly below its very high 40x five-year average P/E, then shares should trade near $945.

That is a significant intrinsic value increase from my previous analysis due to its recent earnings beats and as high bottom-line growth in the coming two years coming closer to reality. A multiple more than two times the average of Europe is somewhat generous in my view, but growth figures remain sanguine.

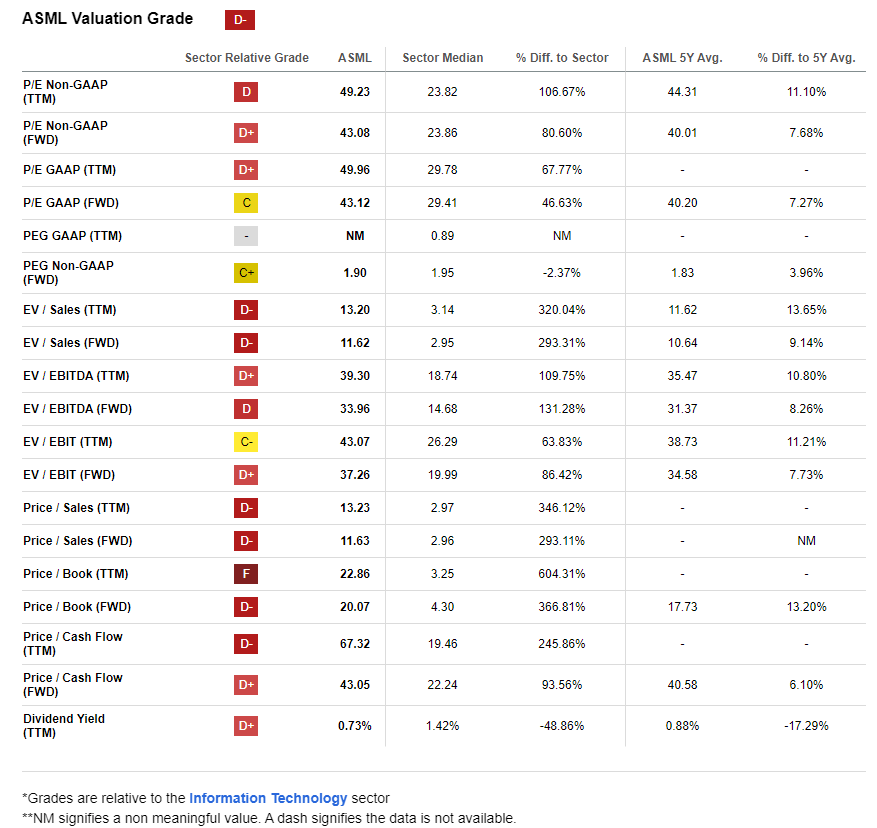

ASML: Premium Valuation, Low FCF

Seeking Alpha

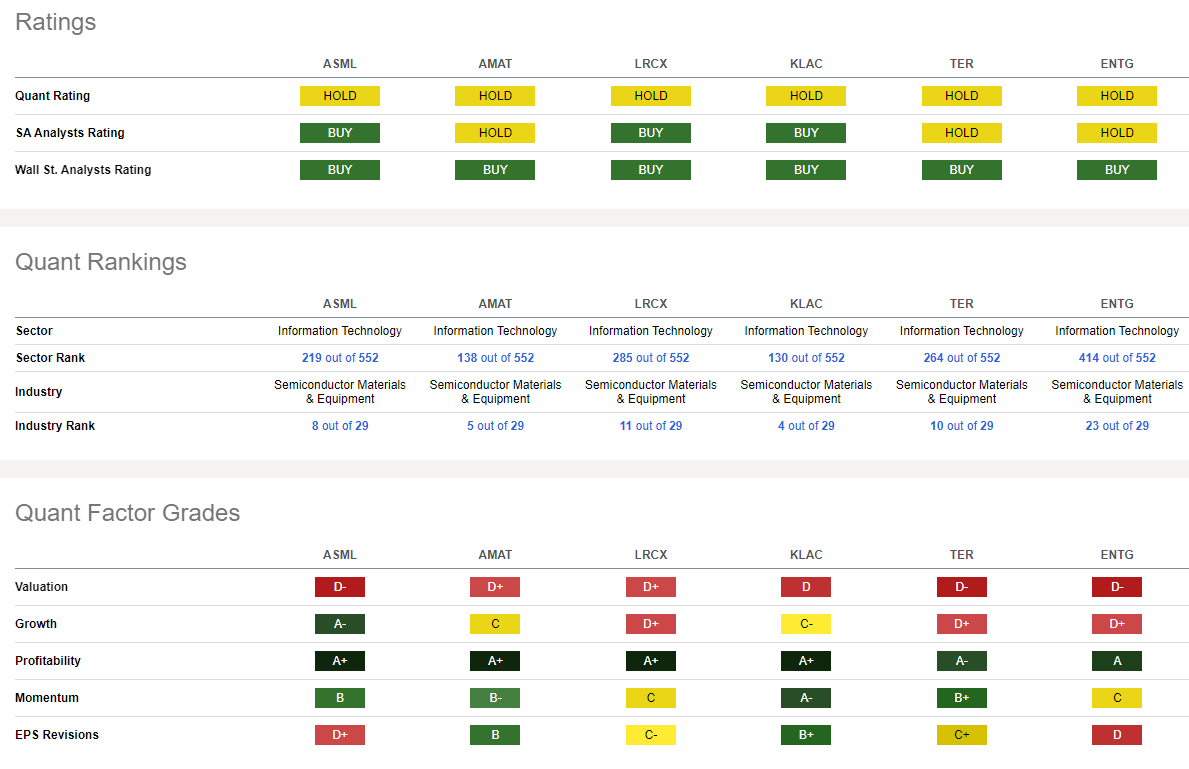

Compared to its peers, ASML sports a premium valuation, on par with the major industry members. Its growth trajectory is quite healthy – the best in its group – while profitability trends are sublime.

While I’d like to see better free cash flow, share-price momentum is decent, though I will note risks on the chart later in the article. Finally, the sellside has been bearish on the company, evidenced by a high 21 EPS downgrades in the last 90 days compared with just eight upgrades.

Competitor Analysis

Seeking Alpha

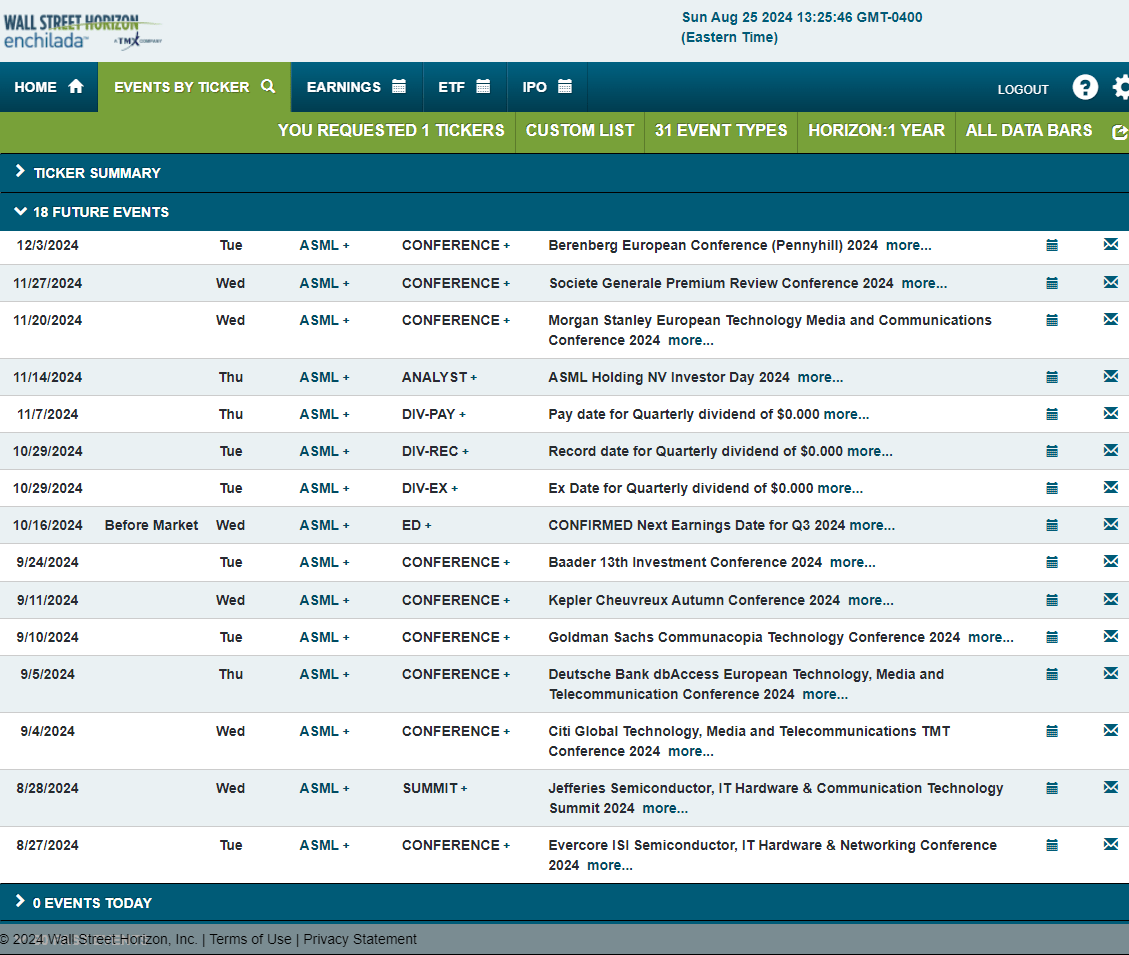

Looking ahead, I can say with more than two years of analyzing stocks on Seeking Alpha that this is the busiest corporate event calendar I have come across.

ASML’s team presents at seven conferences over the next month with a confirmed Q3 2024 earnings date of Wednesday, October 16 BMO. The firm’s annual Investor Day will be held on Wednesday, November 14.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

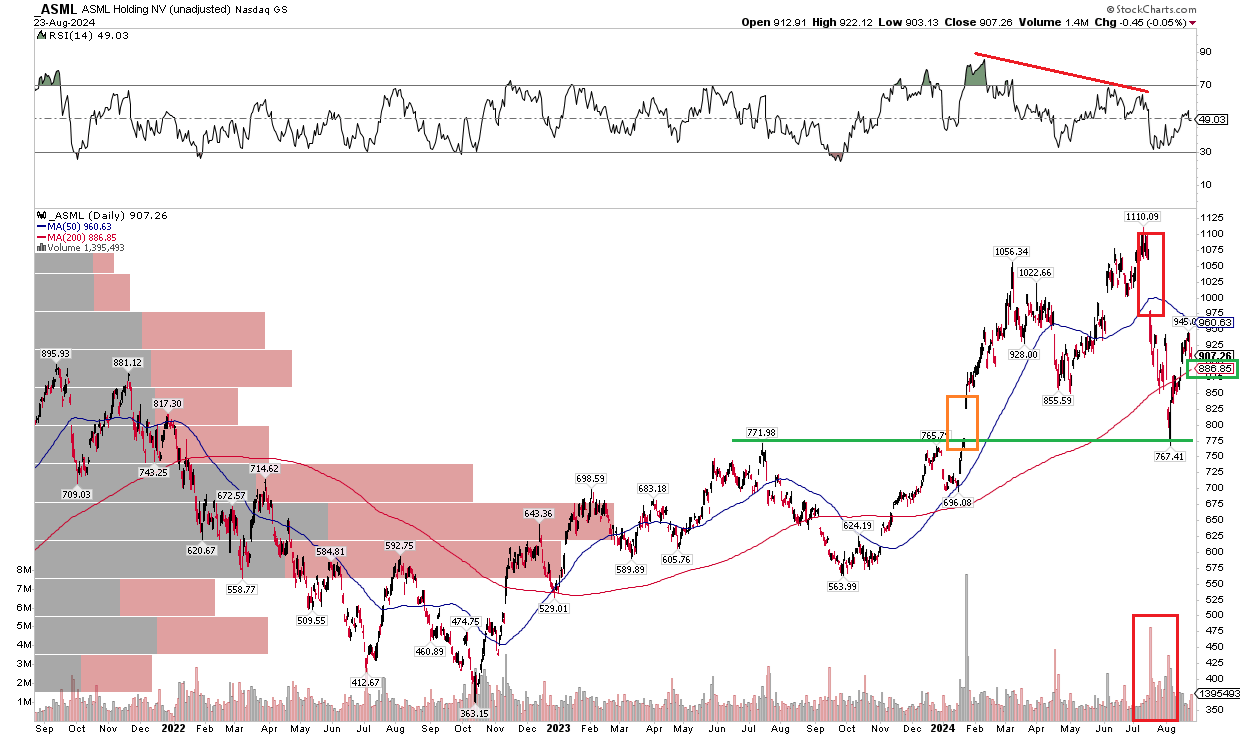

While I see shares undervalued modestly, the technical situation is less than impressive. Notice in the chart below that ASML is about flat going back to the middle of the first quarter. Shares rallied to new all-time highs in the summer before a wave of selling pressure struck chips-industry companies. Support has emerged, however, in the $765 to $772 range – so long as the stock is above that point, the bulls have some control.

Also take a look at the rising long-term 200-day moving average. It remains positively sloped despite the stock being down about 10% from its latest peak. On the bearish side of the ledger, ASML put in a bearish momentum divergence when analyzing the RSI momentum oscillator at the top of the graph. What’s encouraging is that ASML filled its February gap and then met big buying demand in early August.

Overall, support is near $770 while resistance is near the all-time high of $1110 with an upside gap that could be in play if we see strong Q3 price action.

ASML: Shares Hold Critical Support, Bearish RSI Divergence, Rising 200dma

Stockcharts.com

The Bottom Line

I am more upbeat on ASML’s valuation today, but the technical situation is mixed, leading me to reiterate a hold rating ahead of a busy conference season and Q3 earnings in mid-October. Stronger price action and optimism over this fall’s conference engagements could warrant an upgrade to a buy later this year.