Kemter

Both optimists and pessimists contribute to society. The optimist invents the airplane, the pessimist the parachute.”- George Bernard Shaw.

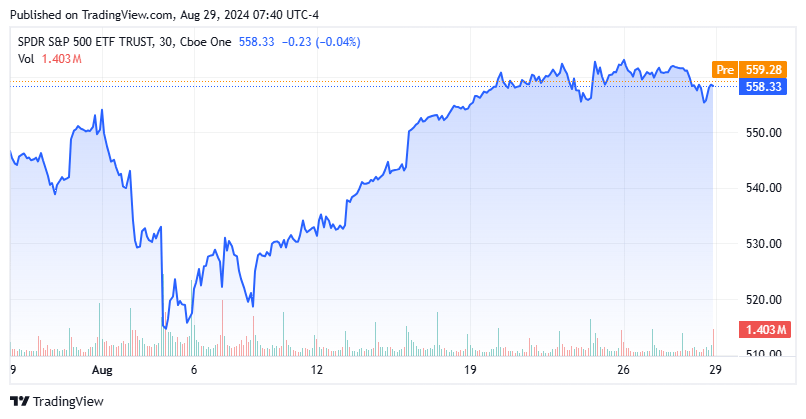

It is difficult to believe that we are already almost all the way through August and mostly through the Dog Days of summer. The start of the NFL season is also just one week away. After a very rough beginning to the month, it looks like the major indexes will end in the black for August. The S&P 500 (SP500) is hanging on to a slim gain for August with two trading sessions left in the month.

Seeking Alpha

What will September bring for investors? Here are five predictions for the ninth month of 2024 and what they could mean for the market.

The Yield Curve Normalizes:

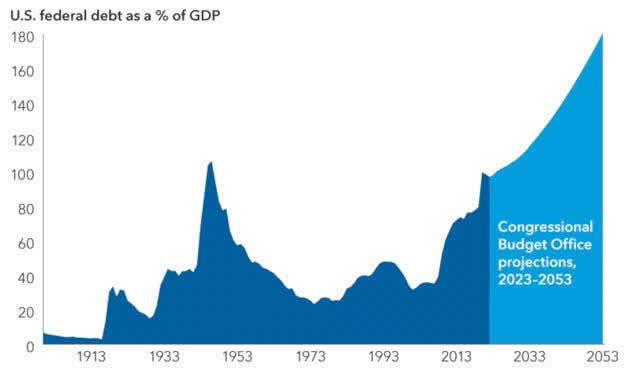

The yield curve, specifically the spread between the 2-Year Bond Yield (US2Y) and the 10-Year Treasury Yield (US10Y) has been continuously inverted now since July 2022. Inversions have been reliable predictors of upcoming recessions, like in 2000 and 2008. However, they tend to have long lag times, as can be seen here. The latest inversion has had a particularly long duration. This is most likely due at least somewhat to the trillions of dollars Congress has pushed into the economy over the past few years. This occurred via COVID-19 stimulus programs and other taxpayer largess, such as the misnamed Inflation Reduction Act or IRA and the CHIPS Act. The Federal Reserve also increased the money supply by 40% over two years during the pandemic.

CBO/Capital Economics

These programs were key drivers of the highest inflation levels since the early ’80s, with the CPI peaking at 9.1% in June 2022. They also have ballooned the national debt, and the U.S. now has the highest Debt to GDP ratio in its 248-year history. The fiscal deficit through the first ten months of the federal government’s FY2024 was $1.52 trillion as well.

CNBC – 08/28/2024

The yield spread has spent some time during this inversion above 100 bps between the two and ten-year treasuries. As of Wednesday, that spread had dropped to just under five basis points. My first prediction for September is that the month will end with this spread “normalized” or with the yield on the 10-Year Treasury above that of the two-year Treasury for the first time since the summer of 2022. Historically, this has happened just as recessions were taking hold. It also could signal a “soft landing” might be ahead. Only time will tell, and this will remain a $64,000 question for investors until resolved one way or another.

Continued Deterioration In The Jobs Market:

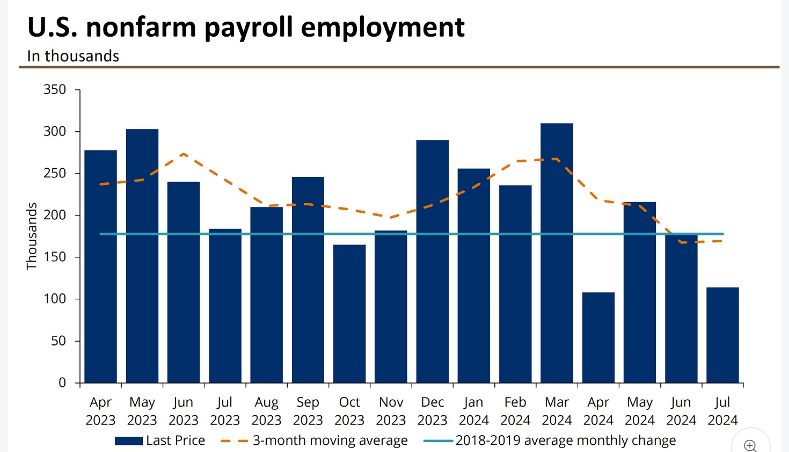

It has become clear recently that the jobs market is slowing, and that was before the massive 818,000 downward jobs revision by the Bureau of Labor Statistics, or BLS, last week. Job openings fell to a three-year low in June of this year. And that does not account for the significant rise in “ghost jobs” recently, where jobs are posted with little intention to fill them.

Then we got the dismal July BLS Jobs report on August 5th. It showed only 114,000 positions were created during the month of July. This was far below the consensus estimate of 174,000 jobs. In addition, the June jobs number was revised down by 27,000 positions to 179,000. This marked the 10th time in the past 14 months, that BLS jobs reports were subsequently revised down as well.

Bloomberg

The jobs trend does not seem to be our friend currently, so the easiest path of resistance is the prediction that the jobs market continues to be weak in September. The August BLS jobs report is due out just before the bell on Friday, September 6th. It will be one of the key economic readings for investors for the month. Based on recent data points, it most likely will be weak.

A 50bps Cut In The Fed Funds Rate:

Currently, futures are pricing in approximately a two-thirds possibility of a 25bps cut to the Fed Funds rate at the September FOMC meeting and a one-third probability of a 50bps cut. If the jobs number comes in weak for the second month in a row and CPI and PPI readings next month continue to show inflation isn’t moving up, I expect the Fed will cut rates by 50bps.

One Sharp Spike Again In Volatility:

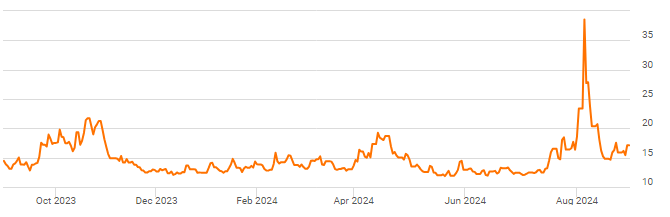

Unfortunately, a 50bps cut in interest rates is unlikely to be well-received by the markets. Especially if the main driver of the move is a weakening jobs market. Investors will rightly worry the Federal Reserve is “behind the curve” once again, much like the central bank was all through 2021 on the inflation front. I expect we will see another spike in volatility as well. I don’t think it will be the same magnitude as the massive spike investors saw early this month when the S&P VIX Index (VIX) briefly moved above the 60 level for the first time in more than four years. However, I think we will see a move in into the 30-40 range at some point in September. Most likely the result of worries around the Federal Reserve. I could also easily see another two percent down day on the S&P 500 during the coming month, if not multiple declines of this order.

Seeking Alpha

Other potential sources of tension in the markets could be of the geopolitical variety. The war in Ukraine could take a dangerous turn and escalate. Russia is likely to capture the key logistical hub of Pokrovsk, or at least have it surrounded, by the end of September. This would be a key victory on the way to consolidating all the Donbas front. Further escalation between Israel and Iran/Hezbollah also appears to have a significant possibility of occurring in September.

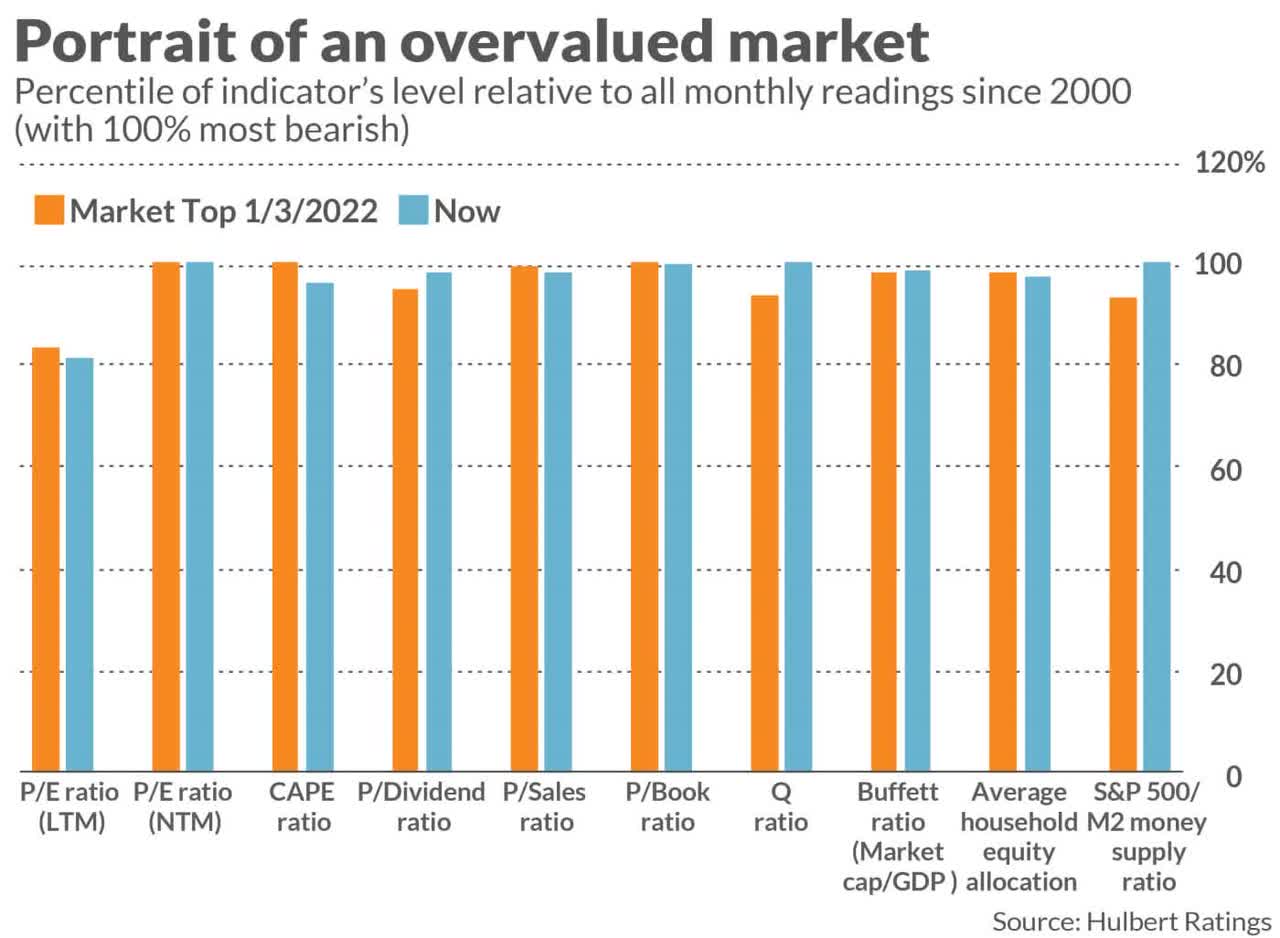

A Down Month For The Markets:

Hulbert Ratings/MarketWatch

As I noted in a recent article, the current stock market is extremely overbought, viewed through numerous valuation metrics. As much or more so than at the beginning of 2022, which was just before the last bear market, equities went through. As investors may recall, the S&P 500 fell 19.64% for that year (18.32% accounting for dividends). The index’s worst annual performance since 2008. The Nasdaq (COMP:IND) performed even worse, losing a third of its value in 2022.

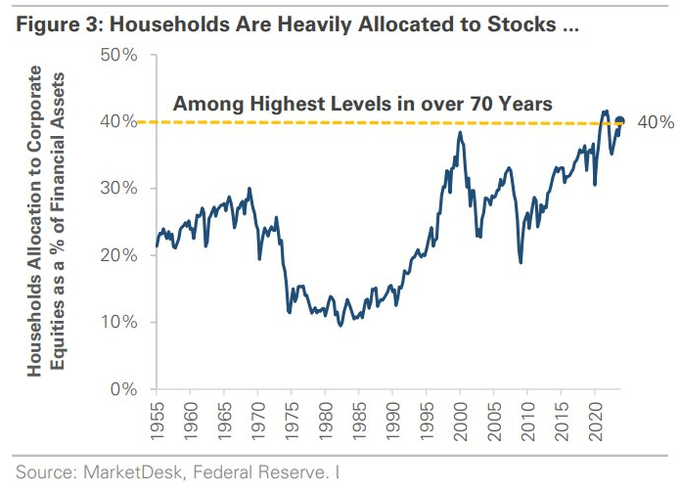

Market Desk, Federal Reserve

As a testament to the current level of investor complacency and greed, the household allocation to equities is at/near its highest level in 70 years. And this is with the markets trading at extreme valuation metrics and with the short term “risk-free” treasuries still yielding slightly more than five percent.

As Warren Buffett has long liked to quip, an investor “should be fearful, when others are greedy and greedy when others are fearful.” And with September historically the worst performing month for investors, my final prediction for the coming month is this: Equities will end the month down, and perhaps significantly so. Prudent investors should position their portfolios accordingly.